Introduction to the Black-Scholes formula | Finance & Capital Markets | Khan Academy

Вставка

- Опубліковано 28 лип 2013

- Created by Sal Khan.

Watch the next lesson:

www.khanacademy.org/economics...

Missed the previous lesson? Watch here:

www.khanacademy.org/economics...

Finance and capital markets on Khan Academy: Interest is the basis of modern capital markets. Depending on whether you are lending or borrowing, it can be viewed as a return on an asset (lending) or the cost of capital (borrowing). This tutorial gives an introduction to this fundamental concept, including what it means to compound. It also gives a rule of thumb that might make it easy to do some rough interest calculations in your head.

About Khan Academy: Khan Academy offers practice exercises, instructional videos, and a personalized learning dashboard that empower learners to study at their own pace in and outside of the classroom. We tackle math, science, computer programming, history, art history, economics, and more. Our math missions guide learners from kindergarten to calculus using state-of-the-art, adaptive technology that identifies strengths and learning gaps. We've also partnered with institutions like NASA, The Museum of Modern Art, The California Academy of Sciences, and MIT to offer specialized content.

For free. For everyone. Forever. #YouCanLearnAnything

Subscribe to Khan Academy’s Finance and Capital Markets channel: / channel

Subscribe to Khan Academy: ua-cam.com/users/subscription_...

I thought the third guy was going to be called Formula

haha!!

good one xD

lol

fantastic

Or model

I have been watching these kind of videos for 3 years now for my uni and i have to say, i found no one close to your broad range of videos and high quality standards.

You made me pass a lot of courses.

I sincerely hope you earn a lot of youtube money.

Lmao facts. This guy is amazing. I know when I get a stable (hopefully high paying) job Im gonna donate to Khan Academy, cuz it is a non-profit

can't agree more!

@@ItsBigChuck and how is it going so far? (just curious, it's been 2 years)

@@user-lc3xp5eo8l😂😂😂

I like the "rough speaking", it made things more clear to me.

Talk rough to me

@@thamadflava daddy

Thank you for Posting. You have done what many teachers do not do today. That of breaking the down the equation. Describing the outcome of the variable in a clear way. Your speaking voice is excellent and engages the listener. Do you know how hard it is to find teachers that want to teach because they are passionate teaching. You have unraveled our FATHER OF PRICING Option"s Formula and have done him a great service.

Even I have the feeling I understood something. Hahaha !

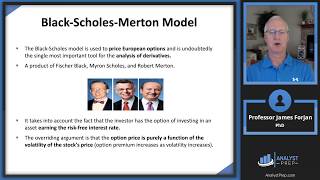

Honorable mention to Louis Bachelier who did the preliminary research that led to the Black Scholes Formula.

In creating the formula, we can it either an initiator, innovator, or executer

Thank you so much! I'm preparing for my CFA level 2 and was stuck on the black-sholes model. You saved me so much time of head-scratching!

Great video! I'm studying for an exam and your videos really are a lot clearer and easier to remember than the rambling of my professor or the 800 pages of examples in our books. Life saver!

This is by far the easiest way to explain the B&S formula ! Thank you so much for this instructive video !

Thank you so much for this. I have immense respect for Khan Academy and the work you guys do. It's quality and life-changing.

A phenomenal lesson I’ve been watching this lesson overtime in my studies, and as I revisited, Always understand a little more. I have immense respect for Khan Academy and the work you guys do, really help me a lot. My humble contribution to this, 's in time 9:09, when you said that an increase in sigma (historical volatility), makes D1 go up and D2 down in value, which it's not quite accurate, I'm certain it's because you speaking in rough terms to be easier to understand.

As my understanding goes, an increase in volatility (sigma) makes BOTH D1 and D2 increase in value, but the ratio of this increase in D1 is greater. Which makes the difference, between them, and their fore between N(D1) and N(D2) greater. And that's why an increase in volatility alone makes the premium of a call option, as the example, have an increase in value. More specifically Extrinsic value. The outcome in the premium it's the same, but I humbly believe that's this's more the case in that situation.

Sorry for the bad English, I'm a foreigner and I love the videos. You guys should do a deep math course on Black and Scholes, I'm certain it's gonna be great! Best Wishes!

my prof. never tried to break down this BS model in class. this is simply the best explanation of one of the most complicated formulas in finance world. Thank you so much Professor Khan. You are the best!

My god, thank you for existing. I love you. Thank you thank you for making finance fun!

Really appreciate with your effort in making this video. I could really get the meaning and applied to tests or exams. THX!

Honestly, I was about to click away, but then I stuck it out. Sal's just a genius at teaching.

Thank you soooo much!! you explain it very clear and very easy to understand. Even if I do not have a strong math background, I can still understand it. which is very helpful for my CMA study. I was trying a long time to find a good explanation online until I found you !!

Thank you for saving me heaps time in studying!!!!

Fantastic!!! with some real world introduction of the people how introduced this calculation, then some basic intuition and then a perfect break down to how it works (although the explanation is not very in depth, which is, at this point, absolutely ok!)

Thank you very much!

Very well explained. I finally understood the logic with the help of your video. Thank you for making it so simple.

Excellent!! Nothing will be able to substitute your way of explaining.... Keep it up, Thanks!!

great video for economics and finance students like me!!! thanks, Sal!!!

Thank you ! This helps me a lot. Keep up the good work :)

Thanks! Very helpful! Looking forward to the derivation!

This video makes me take my subject Financial Engineering seriously. I mean, I just find it interesting on how this mumbo-jumbo of variables makes so much sense in going to more advanced financial modelling techniques.

"Financial engineering"

They're just slapping engineering on everything now aren't they

Thank you. It's interesting and much more easier to understand/remember than textbook :))

Sal Khan is a national treasure.

this saved me in my financial theory and practice exam

Do you have any pdfs used to help

Me study for financial theory as a whole? Please

So simple and clear. Thanks Sal

Fantastic video!

Best video on BSM.

I really enjoyed this video. Thanks.

Thanks for the video! As an Actuarial Student, this video is a pretty accurate and informative explaination video about the B-S Formula. 1 thing I would like to ask though, why didn't you include the divident factor into the equation?

I did this in college, 43 years ago with select stocks in S&P 500. The problem with it is that the distribution of risk is not representative to reality, it’s only an attempt or approximation. For example a standard dev. gives equal weights to up and downside.

has anybody had success with applying this formula @federick ?

That is true for all models. For a model to be useful, it need not always accurately represent reality. However the user has to be aware of the limitations of the model he uses.

Great video Sal! thank you

Wow, this explanation was amazing!

I've never done any finance or economics, nor seen any previous videos on the subject, I just watched it because it sounded interesting :p

Great explanation!!!

Great explanation thank you so much

It's clearly explained! Thanks :).

Wow thank you I intuitively understand the formula now

Sal, you ROCK!!! So thankful for this explanation and overview. Really appreciate bringing Black-Scholes back to practical use. Probably the best explanation on the web. No, make that in the entire world!

Great video as usual sal! Can you by any chance make videos in preparation for the CFA?

Thank you so much

Khan academy 👍

What actions we can take based on greeks values ? Are there any channels that share that ?

Excellent explanation

Thank you so much. you are a awesome teacher.

Amazing video! T does represent time to expiration but not 'how long the holder of the option has to exercise it'. The model was created to value the price of European Options only (not American), Options whereby the contract is only executed at the Expiration date and not before, so we are interested in T in the model as it tells us when the Option gets executed, the holder of the Option cannot execute it early :)

Thank you so much for the video. I have a question, can you tell where can we get the FX option prices history. I doing my thesis and Black Scholes is in my theoretical background, except I will actually use Garman Kohlhagen model, which is basically Black Scholes but is used for FX options.

Thank you!

I want to Algebraic Isolate the Stock Price from the Black Scholes formula.

I have not been successful yet. Is there a way?

Great Video!!!!!

Can you derive mathematically d1? Thank you! Or do you know where to find a derivation of d1? I mean why is it equal d2 Plus stand. Deviation and squared time until expiration

Amazing explanation

great explanation

Thanks.

Options are my bread and butter, calls/puts/credit spreads, always wondered about this formula but never dared to try to understand it! Very interesting video, not for everyone (your younger audience) I suspect, thank you !

Great, thank you ! ! ! :) :) :)

from where would i derive the risk free interest rate or the SD?

great post

you sir are sofa king amazing

is there also a formula like this for american options?

謝謝謝謝謝謝

fantastic

so can i use this formula for American options or no?

Anyone know how to get volatility for non-public start-ups or is there a different valuation method to calculate stock-option expense for start-up?

but if the put option, we just change formula to pay-get, right? or we change the minus result to plus in the end?

tasukete please, help me

Please do the whole series😭

My professor don't teach me anything

I am all dependent on you😭

According to doctor I used to live with that means they spent all their time, "every waking hour and to the exclusion of everything else," trying to win the Nobel prize.

I told him he should do it. All his parents ever did was boast about how wonderful he was, how genius he was, how he was a genius when he was 6 years old. Going on and on about it every time we ever saw them, I didn't see why he shouldn't also get a Nobel prize to go with it. That's when he said you have to spend more time trying to win the prize than you do with anything else in your life.

That was the best nights sleep I've had in a long time! Thank you!!!

Can the N(d1) and the N(d2) be replaced with just the formulas for d1 and d2?

I also think we need a number theory and proofing playlist.

Lovely

Hands off my uni lecturer is the worst, this simple 10 minutes saved my life

"most famous equation in finance", lol. a certain CAPM may be a good rival.

@eloteh CAPM is more likely relevant for other assets and it has already a serious competitor : APT model.

kindly be advised date pf expiration T is expressed in days or weeks or what? if I'm calculating C0, thank u

i would imaging you convert r to daily rate, and then t would be the number of days.

for d1 ...Would we not need to discount the X (exercise price) by e^-rT ?

Sebastian Roest it's market stock price, the strike price is in future

I think we need a quantum mechanics playlist

How is this equation applied for Put options, rather than Call options?

Shall it be possible for you to recommend a book on the topic.

+wronski11 Options, futures, and other derivatives :)

+Alexandru Dumitras writer is Hull

Normally the exercise price aka strike price is denoted by K

I guess it should also be mentioned that Merton and Scholes went on to create a hedge fund (LTCM) which almost melted down the economy and was bailed out by tax payer money to avoid a contagion to the overall economy that would have been in the order of trillions of USDs. The math might have been elegant, but risk pricing (the actual reason why they have received the nobel prize) was not really the thing these gentlemen were good at ironically.

Intuitively why is it hat the higher the stock price the higher the call option is? I thought it'd be the opposite intuitively. Because at a lower stock price the room for increasing stock price is higher thus when you buy a call option, the lower the strike price is the more the potential earnings will be. Can someone explain to me please!!!

What about american options?

One of BSM's many assumptions is that it does not apply to American options

It applies to american options too, you just need to adjust the time variable.

If d_1 and d_2 get larger, doesn't SN(d_1) and Xe^{-rT}(d_2) annulate themselves ? And what is the point therefore ?

Not sure if you care after six months, but it's because of the square

As the standard deviation gets larger, the difference in the two parts of the equation also gets larger.

WHy it has no sound?

S1 displays serial correlation

I remember Sal saying that he wants too but he has to get an intuition on the subject before he can teach it.

Great. Another one? So there are Futures Traders and now Options Traders?

I have a semi-friend who was a Futures Trader but he also calls himself a broker. No idea if that's the same as a Futures Trader. He worked at a place with Futures in its name. He has a fit if I tell online in a social media the exact place of where he worked. No idea why that is either but I don't think I'll ever understand what he does. I've been trying to for over 5 years now. He's done work in all parts of finance though. He was also a hedge funds manager for awhile. He started as a floor trader in the 80's.

I call it a semi-friend bc someone like him never would have been friends with me (never would have met me) if I didn't know someone who died in the World Trade Center. He had a fund for victims' families. That's how I met him but I never used the fund. Eric wasn't a stockbroker. He was a recruiter for professional businesses. I have no idea what that means. Unfortunately I didn't ask and he didn't offer to explain what he does. He was too busy being excited about the Sphere that was in the World Trade Center (donated by someone in 1970) than he was about his actual work.

是為協助

4:55

Black Scholes is extremely inferior 1)The process is actually multifractional (MPRE-multi-fractional with random exponent) multi-tempered stable motion 2).Even if the stochastic process is just a geometric Brownian motion, the nonzero quadratic variation of the aforementioned process coupled w/ non-zero proportional trading costs implies perfect dynamic hedging is infinitely costly. 3)There is endogenous price impact non-neutrality (endogenous reflexivity) 4). There is endogenous incompleteness.

U been reading George Soros' stuff m8?

@axe Feel better now?

Holy crap. I never understood a word said here^

Any chance you could put this in lay man's terms without the scribbles so it might make some sense?

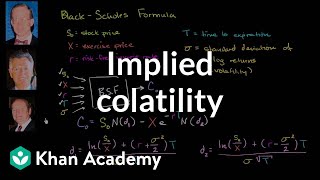

X = exercise price

What's excercise price?? Is it premiums or the options we choose to sell/buy or the amount a option seller is paying to get the premium??

exercise price is the price agreed upon in the beginning for which it will be bought/sold

@@lalaoepsi7572 let say index Dow is trading at 33200 and i write 33000 PE for 10$ then what is the exercise price??

This is an ok formula except that it assumes a normal distribution which is scary for option writers in the event of a black swan

2:09

Where is the Volatility?

👍

Does this equation have any provable value? Or is it just another way for us to spin our wheels? Only useful in the short term. And not even all that useful. Sadly.

I'm such an idiot. I thought it said the Back to School formula XD 🤦♀️ (low key clicked because of that) 🙃

You can never predict anything in a system based on irrational production.

Didn't Edward Thorp really develop this?