You have created the most comprehensive and well made content library on financial/statistical topics on UA-cam. With it, you have helped countless students. People in my postgraduate finance class were joking they got their degrees at BionicTurtle university, since the quality of your explanations is so high and you cover just about everything. It's just amazing work. Thank you!

I am looking everywhere for a clear explanation for where you find the parameter values alpha beta etc, but there is no clear answer anywhere. Why did you not explain why and how these are obtained?

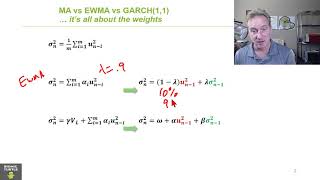

right at the beginning I explain that σ(n) is today's estimate as given by a GARCH(1,1) volatility estimate model where σ(n) = ω + α*µ(n-1)^2 + β*σ(n-1)^2. The forecast is derived from this same GARCH(1,1), so it's all GARCH. The previous video is this same place list goes deeper on GARCH(1.1): ua-cam.com/video/7PEaWHIGTFs/v-deo.html

Hi Professor, where does the forecasted volatility/variance equation come from? It seems not to require the previous returns (u_(n+j)) at all, which is neat. I also was under the assumption that the expectation of the conditional variance is the long-range variance V_L, so why does it represent a forecasted variance here?

You have created the most comprehensive and well made content library on financial/statistical topics on UA-cam. With it, you have helped countless students. People in my postgraduate finance class were joking they got their degrees at BionicTurtle university, since the quality of your explanations is so high and you cover just about everything.

It's just amazing work. Thank you!

how do we decide the right value for Beta?

Very- very good explination. Great work!

Thank you!

God bless you sir!

Thank you! Your explanations are the best!

Where is the lagged component?

I am looking everywhere for a clear explanation for where you find the parameter values alpha beta etc, but there is no clear answer anywhere. Why did you not explain why and how these are obtained?

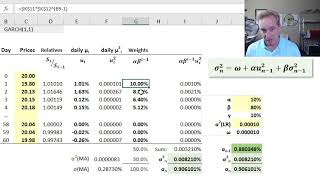

Apparently the most common approach to obtain those values is to use the "Maximum Likelihood Estimate"

ua-cam.com/video/Xef4LL2KUy0/v-deo.html

so how do we get the estimated vol sigma-t that is used in forecasting sigma-t+1?

right at the beginning I explain that σ(n) is today's estimate as given by a GARCH(1,1) volatility estimate model where σ(n) = ω + α*µ(n-1)^2 + β*σ(n-1)^2. The forecast is derived from this same GARCH(1,1), so it's all GARCH. The previous video is this same place list goes deeper on GARCH(1.1): ua-cam.com/video/7PEaWHIGTFs/v-deo.html

Hi Professor, where does the forecasted volatility/variance equation come from? It seems not to require the previous returns (u_(n+j)) at all, which is neat. I also was under the assumption that the expectation of the conditional variance is the long-range variance V_L, so why does it represent a forecasted variance here?

That intro to stats class doesnt even get you close to where you need to be

It's not useful at all.

Why ?