Volatility: Exponentially weighted moving average, EWMA (FRM T2-22)

Вставка

- Опубліковано 7 лют 2025

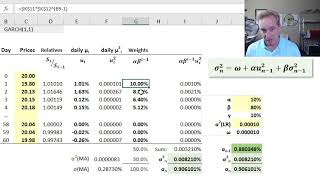

- [here is my XLS trtl.bz/2t1pb9S] The exponentially weighted moving average (EWMA) cures the key weakness of the common historical standard deviation by assigning greater weight to more recent returns and lessor weights to more distant (in the past) returns. Its key parameter is lambda, λ, which specifies the ratio of consecutive weights. The EWMA elegantly simplifies to its recursive form: σ^2(n) = λ*σ^2(n-1) + (1-λ)*u^2(n-1). Discuss this video here in our forum: trtl.bz/2Hztp12

Subscribe here www.youtube.co...

to be notified of future tutorials on expert finance and data science, including the Financial Risk Manager (FRM), the Chartered Financial Analyst (CFA), and R Programming!

If you have questions or want to discuss this video further, please visit our support forum (which has over 50,000 members) located at bionicturtle.co...

You can also register as a member of our site (for free!) at www.bionicturt...

Our email contact is support@bionicturtle.com (I can also be personally reached at davidh@bionicturtle.com)

For other videos in our Financial Risk Manager (FRM) series, visit these playlists:

Texas Instruments BA II+ Calculator

• Texas Instruments BA I...

Risk Foundations (FRM Topic 1)

• Risk Foundations (FRM ...

Quantitative Analysis (FRM Topic 2)

• Quantitative Analysis ...

Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

• Financial Markets and ...

Financial Markets and Products: Option Trading Strategies (FRM Topic 3, Hull Ch 10-12)

• Financial Markets and ...

FM&P: Intro to Derivatives: Exotic options (FRM Topic 3)

• FM&P: Intro to Derivat...

Valuation and Risk Models (FRM Topic 4)

• Valuation and RIsk Mod...

Coming Soon ....

Market Risk (FRM Topic 5)

Credit Risk (FRM Topic 6)

Operational Risk (FRM Topic 7)

Investment Risk (FRM Topic 8)

Current Issues (FRM Topic 9)

For videos in our Chartered Financial Analyst (CFA) series, visit these playlists:

Chartered Financial Analyst (CFA) Level 1 Volume 1

• Level 1 Chartered Fina...

#bionicturtle #risk #financialriskmanager #FRM #finance #expertfinance

Our videos carefully comply with U.S. copyright law which we take seriously. Any third-party images used in this video honor their specific license agreements. We occasionally purchase images with our account under a royalty-free license at 123rf.com (see www.123rf.com/... we also use free and purchased images from our account at canva.com (see about.canva.co.... In particular, the new thumbnails are generated in canva.com. Please contact support@bionicturtle.com or davidh@bionicturtle.com if you have any questions, issues or concerns.

Thanks David. I'm back for another lesson. What was different about this video is that you made clear what weakness does this approach overcome. I like that you showed it to be a step up from historical standard deviation. I wish there was a video where the focus was only on the weaknesses of methods and how other measures of volatility were introduced to overcome those issues. For example, standard deviation, EMWA, GARCH (1,1), and so on.

No... understand the term persistent first. Your will make mistake in exam without thoroughly understanding persistent

can someone give me Bionic Turtle's xls file, i click the link but its has been delete

You are saying that Day 0 is today and Day 1 is yesterday. But Your return calculation has swapped the numerators and denominators. Otherwise concept is clear

You sir, saved my day!

Glad to hear it, thank you!

How do we calculate the volatility n-1

I don't understand: is the EWMA for the estimation or for historical data only?

It may be important to show the correct formula of the first weight, instead of (1-lambda) it should be (1-lambda)/(1- lambda^N) cause if lambda is .99 or .98, using (1-lambda) in the first weight wont get a sum that gets close enough to 1 if you have 262 observations or so.

Thank you

Why is the day 1 price relative amount of 0.90909 calculated as Si-1/Si rather than inversely as the other days all are?

what is the so-call "half-life" in EWMA? tia

Great video

Thank you for explaining. Just a thought, what do you think of this method to other parametric methods?

can you explain why the number in 2 first row appeared in the video is not the same as those in the excel file?

Thanks a lot sir

If day 60 is the most recent day, shouldn't the strongest weight start from bottom? Meaning cell G68 = 20.0 %, G67 = 16.0%, etc. Thank you!

This simulation assumes that day zero is today's closing price and day 1 is yesterday's price such that the most recent log return = LN(20/19.80) = +1.01% and this most recent return is assigned the highest weight of 20.0%. However, I admit the presentation of the time dimension here is sub-optimal, or maybe even confusing: I can see why you'd assume 60 is the most recent day for a couple reasons. I could have shifted the yellow column of prices down one row (to better align the most recent return with the most recent price; maybe helps a little) and I SHOULD have labelled the days with (eg) "t -1, t-2" to convey they are going back in time. Thanks because next time i'll make that more clear!

@@bionicturtle Thank you so much for responding, I understand it better now. However, then if I'm not mistaken there is a typo in the "price relative" column. The first calculation in cell D8 is congruent with your explanation and the price relative formula but in cells D9:D68 you swich the numerator with the denominator making the price relative "inversely". This was the main reason I thought day 60 was the most recent day.

@@mariana__7814 Oh, yes, sorry, you are totally correct! That's just a flat out MISTAKE in the XLS (I must have switched my intention with respect to the direction of time). No wonder you thought D60 was most recent. So this is just an error with the XLS, unfortunately: column D should be consistent. Fortunately, because column C is a random price vector anyway, we can just view column D as the historical series INPUT (of price relatives). Thank you for your observations, sorry for the confusion!

@@bionicturtle no worries, thank you very much for clarifying!

@@bionicturtle just putting dates on the left would do :)

Thank you very much! One question, how do I start with regards with my volatility calculation? What is my variance at time t=0?

It's empty. You can see that in Bionic Turtle's xls. There is only the closing price and nothing to compare it to until t=1

can you give me Bionic Turtle's xls file, i click the link but its has been delete

@@DamiensRegicide

In Excel Data Analysis tool pack we have installed EXponentially smoothing Average Function. can we use that?

I have not used it, sorry, don't know

How does 0.000003 * 20% give 0.0001? That would give you 0.0000006?

Yes correct, but it's just that 0.0000006

rounds to 0.0001%; my Excel is displaying 0.0001% but the underlying value at cell H8 is 0.0000006