Thank you very much for the video. I am a lawyer and though as lawyers we don't need to go so deep when we deal with swaps, understanding the underlying functioning is quite useful!

Thank you. I have spent hours trying to figure out how to price it and I couldn't figure out how the floating rate bond is worth only one cash flow. duh!

Because those LIBOR rates represent the market rates that the fixed income bond (fixed payment side of the swap) must be based upon for valuation purposes

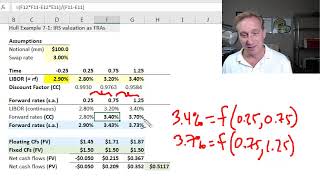

Hi David! I am confused with your discount factors. Can you explain please why do you use continuous compounding? It's unrealistic, isn't it? In your example there is a semiannual compounding, should not your discount factor be like 1/(1+libor/2)^(n*2)?

Hi kiril, if we read an assumption given like "15-month LIBOR is 3.4%", it is insufficient because we aren't given the compound frequency (this is Hull's question, btw). We could be told (eg) that the rate is "15-month LIBOR is 3.4% with semi-annual compound frequency" in which case your formula would apply! But if we are told that "15-month LIBOR is 3.4% with continuous compound frequency" then we retrieve the discount factors with continuous discounting, because it's a FEATURE of the given rate. The advantage of discount factors is that "they do not lie" because they don't need compound frequency assumption (they've already embedded it). In this way, the reason (to answer your question) is that compound frequency is part of the definition of a nominal (aka, stated) rate. A nominal/stated rate is imprecise without it, b.c 3.4% s.a. and 3.4% cc are (slightly) different rates. I hope that's helpful!

Thank you David for your answer. But usually what compound frequency for Libor is implied? I mean if I open swap manager in Bloomberg I will enter parameters of the swap and I can see the Libor curve, but how to understand what frequency is used for pricing? I tried to replicate swap from Bloomberg in excel many times, and I failed so far. Still cannot grasp it. Academic way of explaining is way easier than the way it really works. Any advice is appreciated!

Thanks for the video! When looking on Bloomberg on a swap calculator, there is a DV01 per leg, but only one PV01. Can you discuss the differences here?

Thank you for the uploaded video. My question is: why did you state that the floating rate bond in 3 months (that is the PV of all future cashflows by then) will be equal to the par value?

Hi David! Thanks heaps for the video. It was really concise and to the point. Can you please put the excel file here as well? Cause in the other videos, sharing the excel file helped a lot. Cheers

Thank you David, Can you give brief clarification on how to calculate daily floating and fixed legs values? i use to evaluate daily PnLs so i would like to know how to calculate them on a daily basis with using of LIBOR. take any of example and give me.

I spent hours looking at the note, couldn’t figure out. But this video cleared the concept

Thank you for watching! We are very happy to hear that our video was so helpful!

Thank you so much!! Very well-organized and clear. You just save my midterm-exam from getting zero!!

Thank you very much for the video. I am a lawyer and though as lawyers we don't need to go so deep when we deal with swaps, understanding the underlying functioning is quite useful!

Rodrigo Cordova You're welcome! We are happy to hear that you found this video useful!

Thank you. I have spent hours trying to figure out how to price it and I couldn't figure out how the floating rate bond is worth only one cash flow. duh!

Hi David, understood everything but the part with determining the floating rate coupons... can you elaborate on that?

Thanks for the video!

Thanks a lot David. It was really helpful! an old fan.

For the floating rate bond what discount rate did you use ?

why did we use the discount factors of the FLOATING rates to calculate the present value of the FIXED cash flows??

Because those LIBOR rates represent the market rates that the fixed income bond (fixed payment side of the swap) must be based upon for valuation purposes

in other words they are the benchmark (min rate to earn or simply called as YTM)

Hi David! I am confused with your discount factors. Can you explain please why do you use continuous compounding? It's unrealistic, isn't it? In your example there is a semiannual compounding, should not your discount factor be like 1/(1+libor/2)^(n*2)?

Hi kiril, if we read an assumption given like "15-month LIBOR is 3.4%", it is insufficient because we aren't given the compound frequency (this is Hull's question, btw). We could be told (eg) that the rate is "15-month LIBOR is 3.4% with semi-annual compound frequency" in which case your formula would apply! But if we are told that "15-month LIBOR is 3.4% with continuous compound frequency" then we retrieve the discount factors with continuous discounting, because it's a FEATURE of the given rate. The advantage of discount factors is that "they do not lie" because they don't need compound frequency assumption (they've already embedded it). In this way, the reason (to answer your question) is that compound frequency is part of the definition of a nominal (aka, stated) rate. A nominal/stated rate is imprecise without it, b.c 3.4% s.a. and 3.4% cc are (slightly) different rates. I hope that's helpful!

Thank you David for your answer. But usually what compound frequency for Libor is implied? I mean if I open swap manager in Bloomberg I will enter parameters of the swap and I can see the Libor curve, but how to understand what frequency is used for pricing? I tried to replicate swap from Bloomberg in excel many times, and I failed so far. Still cannot grasp it. Academic way of explaining is way easier than the way it really works. Any advice is appreciated!

Thanks for the video!

When looking on Bloomberg on a swap calculator, there is a DV01 per leg, but only one PV01. Can you discuss the differences here?

could someone give me more explanation on why the floating leg becomes par after the payment (reset date)??

Excellent illustration .. do u have the valuation spreadsheet for this IRS, please?

Thank you for the uploaded video.

My question is: why did you state that the floating rate bond in 3 months (that is the PV of all future cashflows by then) will be equal to the par value?

Hi David! Thanks heaps for the video. It was really concise and to the point. Can you please put the excel file here as well? Cause in the other videos, sharing the excel file helped a lot. Cheers

Hi David, thanks for this video!

Is there a similar one for currency swaps?

Thank you David, Can you give brief clarification on how to calculate daily floating and fixed legs values?

i use to evaluate daily PnLs so i would like to know how to calculate them on a daily basis with using of LIBOR. take any of example and give me.

2:10 you said it had "remaining life of 18 months" you mean 15 months

Can some one answer please ?

Why did we use the discount factors of the FLOATING rates to calculate the present value of the FIXED cash flows??

Not sure, but I think to keep it zero on each payment

thanks for the video. and would you mind explain why fair price of float bond in 3 month is at par? thanks a lot again!

thanks

+Seunghyun Kim You're welcome! Thanks for watching!