@sammyjny Future coupon pays LIBOR that prevailed at PRIOR 6 month settle (if LIBOR curve static, prior 6 mo L = 5.5%). But that's annual bond equivalent, so future coupon = 5.5%/2. Discounting this $ to PV is next step, here disc. @ 3 mo. continuous. Your 100 par would be valid if 3 mo LIBOR = 6 mo LIBOR *and* coupon freq (semi-annual) = discount (continuous) Re the 0.75 and 1.25 floaters: actually, this is where your idea applies: at settle, bond = par, so 100 effectively impounds them

It's a john hull example so .025, .50 is arbitrary: it's just to show pricing in-between coupons (T - 3 months to next coupon). Could be anything depending on T - ? to next coupon. Cash flows are independent of discounting. First, get the cash flows. Second, discount them. And the cash flows are based on, fixed at 8% semi and floating, based on 6 month libor i.e. 1/2 of 5.5%

@sammyjny We you say is valid (of course) except it would give the same result. So it is merely a simplification that is possible only on the exact moment of settlement. When you asked why the bond isn't valued at par (100), that is the correct idea, at settle: our basis for determining future floating coupons is the forward rates and these necessarily reconcile with the discount rate. Similar to 100 * (1+r) / (1+r) = 100 but works for series of forwards. ...i'm not clear on your second part

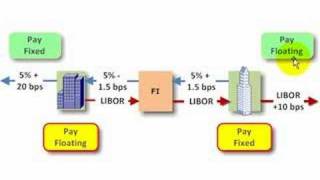

I remember starting on the swaps desk at First Chicago (now J.P. Morgan) in 1991 and a letter was sent to me, Simon Rogers, on the S.W.A.P.S desk. Someone thought it stood for something, like Special Weapons And Products (!). It only means you are "swapping" cash flows. Always draw them out to make sure you are using the correct side of the bid/offer spread.

Hi soncheeba, it could use discrete (annual) compounding instead. For my given continuous rate, there exists a higher annual rate that is equivalent. But continuous is more convenient/common in academic finance, is all. David

Hi, thank you for the video. Quick question on the idea of pricing the legs. When you price the fixed leg, you take into account all the future coupon payments and notional and then discount them. However, when you price the floating leg, you consider just one coupon and the notional. I may be understanding something incorrectly and I would appreciate if you could help me understand the concept behind the pricing of floating leg.

@sammyjny ...(append) You've identified the two difficult ideas here: 1. Determination of (future) coupon cash flow is a function of the floating swap &, any time valuation is between coupon settlements, will differ from discount because the time horizon won't match (i.e., coupon is 6 month rate but discount is < 6 mo rate. Also, here the compound freq complicate) 2. At the future settlement exactly (here, +0.25 months), we do have a match. Then indeed discounted PV = par

the timing of the valuation is important, we valuate the swap at 9th month, 3 months after the first coupon payment, thus, we receive next floating coupon in 3 months time base on the 6 months floating rate (5.5%). however, we discount the fv base on 3 months floating rate (5%) because the discount period is only 3 months

@@irislynn4970 Yes, even i was struggling that why we took 6 months for calculating future cash flow, and for PV we took 3 months rate. Thanks, David :)

i still don't understand - we are going to pay coupon in 3 Mo but why take 6 Mo rate? 1. the rate that we are going to pay is already agreed 3 Mo back right? that rate is not given anywhere? 2. there are 3 floating coupon left but why only one pay coupon is taken in right side please explain

@sammyjny.... the point is that the ISP is being valued in mid of the first leg of 6 months and hence if at that point of time want to know what am i getting i would need to take into account the fixed income part in toto while the payment in first leg that is floating leg is yet 3 months away and at 3 months form deal is what the example points to and hence the 3 month value of floating cupon is subtracted.... when we calculate at 0.5 yrs the value of ISP will be diff. hope some bit is clear...

Hello David. I think the uncertainty on the floating rate side of this is here you use the 6m rate to calculate the floating coupon. It comes across on the video that you are using the 6m at the 3m point in time rater than the 6m rate at inception. However as you said the libor curve is not changing then this does in fact make sense.

everything makes sense to me except for the following: when the bond expires at t = 1.25, why do we use the libor rate only at t = .5 and not at .5, 1, and 1.25?

Shouldn't the FV of floating-rate cash flows be the LIBOR rate on the previous payment date divided by 2 (semi-annually)plus notional? Why have we taken the value to be the 6m future LIBOR rate divided by 2 plus notional?

I am getting the value of swap as $3.6 when I took the 6 month LIBOR at 5.5%. The continuous compounding rate is 5.4257%. So the value of swap should be (4-2.75)e^(-0.0542*(3/12))+(4-2.75)e^(-0.0542*(9/12))+(4-2.75)e^(-0.0542*(15/12)) = 3.6. Please tell where I am going wrong?

Something is off, or perhaps it's escaping me: the basic assumption of an IRS swap is the PV for both legs at time of inception must be equal. If fixed payment is 8%/year the Libor should be equal to 8%, unless the agreement is for Libor +1, 2% or so. I think the LIBOR curve is unrealistic but also incorrect...what am I missing?

no, only if the spot/zero rate curve is flat (which would actually be unrealistic, to have no term premium). Otherwise, we expect the swap rate to be different than the current (libor) spot rate. I don't know what you mean by unrealistic LIBOR. A fair swap rate at inception reflects the term structure which tends to be non-flat. This is all really basic, established theory (true the video is over 10 years old, as you can see by the date). Please note that I have a more current playlist including more current IRS valuation here ua-cam.com/video/tFWoVTHc3AM/v-deo.html

Perhaps a stupid question. But why do you use the LIBOR rates as the yield for the fixed rate bond when calculating the present value? why is not r fixed in the formula?

Hey David, in an interest swap deal hull claims a fixed rate receiver is long the fixed rate bond and short the floating rate bond -- and the reverse is for the fixed rate payer. I am little confused by this construct because if the FR receiver is long the FR bond he/she is expecting interest rates to go down hence the increase in value of the FR bond (right?). But won't this be the same change in direction/value (i.e. an increase) for the FL rate bond since LIBOR would have gone down too.

Thanks David for this explanation but can you/someone please explain for the Floating Leg Calculation as to why you use 5.5% for calculating the FV but use 5% for calculating the PV

Hi Bionictutle. Firstly thank you for such a simple to understand tutorial on IRS. the only thing I don't understand is, by definition the variable leg of the swap is unknown, so how do you know what the swap rates should be? in your tutorial you made up those numbers, which means if i choose my own interest rate i can make the value of the swap to positive or negative.

Hi David! Where can we get this valuing sheet? thanks. I am currently struggling to find out how discount factors are calculated and how that formula is formed/proof. Can you give some insights please?

JareBMF I sort of figure it out. But I have faced more rock-walls while building zero curve... Someone told me if we use new proxies like OIS and Fed Fund Rates that there's no need for building discount factor curve, infact we could simply bootsratp OIS curve to derive zero curve. From there calculate Fwd rates to define the floating leg's cashflows... Does it make sense to you?

I am not sure the logic presented here is very accurate for the floating leg, the floating rate should be unknown other than the first floating-rate cash flow payment. the actual valuation for the floating leg should be the first floating discounted plus 1 discounted to the present day for those unknown LIBOR rate cash flows.

The rates for the floating leg are forward rates. In this case they are made up, but in reality they would be know ie: 3 month Forward LIBOR in 6 months from now.

@sammyjny Future coupon pays LIBOR that prevailed at PRIOR 6 month settle (if LIBOR curve static, prior 6 mo L = 5.5%). But that's annual bond equivalent, so future coupon = 5.5%/2.

Discounting this $ to PV is next step, here disc. @ 3 mo. continuous. Your 100 par would be valid if 3 mo LIBOR = 6 mo LIBOR *and* coupon freq (semi-annual) = discount (continuous)

Re the 0.75 and 1.25 floaters: actually, this is where your idea applies: at settle, bond = par, so 100 effectively impounds them

It's a john hull example so .025, .50 is arbitrary: it's just to show pricing in-between coupons (T - 3 months to next coupon). Could be anything depending on T - ? to next coupon.

Cash flows are independent of discounting. First, get the cash flows. Second, discount them. And the cash flows are based on, fixed at 8% semi and floating, based on 6 month libor i.e. 1/2 of 5.5%

@sammyjny We you say is valid (of course) except it would give the same result. So it is merely a simplification that is possible only on the exact moment of settlement. When you asked why the bond isn't valued at par (100), that is the correct idea, at settle: our basis for determining future floating coupons is the forward rates and these necessarily reconcile with the discount rate. Similar to 100 * (1+r) / (1+r) = 100 but works for series of forwards.

...i'm not clear on your second part

I remember starting on the swaps desk at First Chicago (now J.P. Morgan) in 1991 and a letter was sent to me, Simon Rogers, on the S.W.A.P.S desk. Someone thought it stood for something, like Special Weapons And Products (!). It only means you are "swapping" cash flows. Always draw them out to make sure you are using the correct side of the bid/offer spread.

Hi soncheeba, it could use discrete (annual) compounding instead. For my given continuous rate, there exists a higher annual rate that is equivalent. But continuous is more convenient/common in academic finance, is all. David

Hi, thank you for the video. Quick question on the idea of pricing the legs.

When you price the fixed leg, you take into account all the future coupon payments and notional and then discount them. However, when you price the floating leg, you consider just one coupon and the notional. I may be understanding something incorrectly and I would appreciate if you could help me understand the concept behind the pricing of floating leg.

@sammyjny ...(append) You've identified the two difficult ideas here:

1. Determination of (future) coupon cash flow is a function of the floating swap &, any time valuation is between coupon settlements, will differ from discount because the time horizon won't match (i.e., coupon is 6 month rate but discount is < 6 mo rate. Also, here the compound freq complicate)

2. At the future settlement exactly (here, +0.25 months), we do have a match. Then indeed discounted PV = par

the timing of the valuation is important, we valuate the swap at 9th month, 3 months after the first coupon payment, thus, we receive next floating coupon in 3 months time base on the 6 months floating rate (5.5%). however, we discount the fv base on 3 months floating rate (5%) because the discount period is only 3 months

Thank you!!! omg i finally got it now! you have no idea how struggle i was !!!

@@irislynn4970 Yes, even i was struggling that why we took 6 months for calculating future cash flow, and for PV we took 3 months rate. Thanks, David :)

i still don't understand - we are going to pay coupon in 3 Mo but why take 6 Mo rate?

1. the rate that we are going to pay is already agreed 3 Mo back right? that rate is not given anywhere?

2. there are 3 floating coupon left but why only one pay coupon is taken in right side

please explain

no the main point is the implied forward curve, but thanks for trolling

Always a fan of yours David.. once again thanks a lot..

@sammyjny.... the point is that the ISP is being valued in mid of the first leg of 6 months and hence if at that point of time want to know what am i getting i would need to take into account the fixed income part in toto while the payment in first leg that is floating leg is yet 3 months away and at 3 months form deal is what the example points to and hence the 3 month value of floating cupon is subtracted.... when we calculate at 0.5 yrs the value of ISP will be diff. hope some bit is clear...

Hello David. I think the uncertainty on the floating rate side of this is here you use the 6m rate to calculate the floating coupon. It comes across on the video that you are using the 6m at the 3m point in time rater than the 6m rate at inception. However as you said the libor curve is not changing then this does in fact make sense.

There is an error in your calc. For Floating rate PV, you took discount rate on 5% LIBOR instead of 6 Mo LIBOR of 5.5%.

everything makes sense to me except for the following: when the bond expires at t = 1.25, why do we use the libor rate only at t = .5 and not at .5, 1, and 1.25?

Because we assume the libor curve does not change over time and the floating rate is based on the .5 year rate. Probably 8 years to late.

Shouldn't the FV of floating-rate cash flows be the LIBOR rate on the previous payment date divided by 2 (semi-annually)plus notional? Why have we taken the value to be the 6m future LIBOR rate divided by 2 plus notional?

Excellent vid. However, are we making an assumption by saying that LIBOR curve will remain fixed? How do we get around this assumption?

I am getting the value of swap as $3.6 when I took the 6 month LIBOR at 5.5%. The continuous compounding rate is 5.4257%. So the value of swap should be (4-2.75)e^(-0.0542*(3/12))+(4-2.75)e^(-0.0542*(9/12))+(4-2.75)e^(-0.0542*(15/12)) = 3.6.

Please tell where I am going wrong?

swap leg is not continuously compounded in the video (like the coupon leg) only the discounting is continuous not the payment legs

finally got the whole idea clearly and systematically, AWESOME EXPLANATION!!!!

Can you also guide towards valuation of a Loan product

in this case, the video adopts respective LIBOR rate as risk free rate. Can we also use OIS rate as risk free rate? (OIS= overnight index swap)

Something is off, or perhaps it's escaping me: the basic assumption of an IRS swap is the PV for both legs at time of inception must be equal. If fixed payment is 8%/year the Libor should be equal to 8%, unless the agreement is for Libor +1, 2% or so. I think the LIBOR curve is unrealistic but also incorrect...what am I missing?

no, only if the spot/zero rate curve is flat (which would actually be unrealistic, to have no term premium). Otherwise, we expect the swap rate to be different than the current (libor) spot rate. I don't know what you mean by unrealistic LIBOR. A fair swap rate at inception reflects the term structure which tends to be non-flat. This is all really basic, established theory (true the video is over 10 years old, as you can see by the date). Please note that I have a more current playlist including more current IRS valuation here ua-cam.com/video/tFWoVTHc3AM/v-deo.html

Perhaps a stupid question. But why do you use the LIBOR rates as the yield for the fixed rate bond when calculating the present value? why is not r fixed in the formula?

Coupons can be fixed required rate of returns are dynamic

Hey David, in an interest swap deal hull claims a fixed rate receiver is long the fixed rate bond and short the floating rate bond -- and the reverse is for the fixed rate payer. I am little confused by this construct because if the FR receiver is long the FR bond he/she is expecting interest rates to go down hence the increase in value of the FR bond (right?). But won't this be the same change in direction/value (i.e. an increase) for the FL rate bond since LIBOR would have gone down too.

Thanks for putting this up. How did you get the $102.75? What were your calculations?

Why is there only one floating coupon?

why 8% annual par coupon becomes $4 as the quaterlly payments? I thought it is 8%/4*100=$2

Can you please share the link where the swap spreadsheet can be downloaded? Thanks

Thanks David for this explanation but can you/someone please explain for the Floating Leg Calculation as to why you use 5.5% for calculating the FV but use 5% for calculating the PV

Why is an Internet rate swap treated as a Bond for pricing?

Hi, thank you sir for your kind explanation. I was wondering if you could please post something on accounting for derivatives?

Hi, which john hull's text are u using as reference for this example? Thanks

Hi Bionictutle.

Firstly thank you for such a simple to understand tutorial on IRS. the only thing I don't understand is, by definition the variable leg of the swap is unknown, so how do you know what the swap rates should be? in your tutorial you made up those numbers, which means if i choose my own interest rate i can make the value of the swap to positive or negative.

@bionicturtledotcom I dont understand what you did with the exponential function rather then discount factor?

perfect. Exactly the method I got in class. Thanx

What does it mean if the LIBOR rates are annualized?

Hi David! Where can we get this valuing sheet? thanks.

I am currently struggling to find out how discount factors are calculated and how that formula is formed/proof. Can you give some insights please?

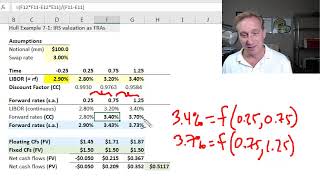

Discount factor = exp(-rate*T), for DF in 9month that with 6% rate that will be, exp(-6%*0,75)=0,955997

JareBMF I sort of figure it out. But I have faced more rock-walls while building zero curve... Someone told me if we use new proxies like OIS and Fed Fund Rates that there's no need for building discount factor curve, infact we could simply bootsratp OIS curve to derive zero curve. From there calculate Fwd rates to define the floating leg's cashflows... Does it make sense to you?

which software is used for valuing interest rate options, Credit default swaps, MBS etc?

Thanks David It helps a lot

I am not sure the logic presented here is very accurate for the floating leg, the floating rate should be unknown other than the first floating-rate cash flow payment. the actual valuation for the floating leg should be the first floating discounted plus 1 discounted to the present day for those unknown LIBOR rate cash flows.

Topman! It helped me soooo much

The rates for the floating leg are forward rates. In this case they are made up, but in reality they would be know ie: 3 month Forward LIBOR in 6 months from now.

Did he say "Inception"? I must be in a dream, where's my totem, I knew they were trying to extract my bank account password! :P

@adaseth you have been in a dream the entire time: your totem is also unreal. We already have your account info :)

its really helpfull.

I see it is from your added “l” at the end 🤦🏻♂️🙅♂️

thaaannksss so much👌👌👌👌

You're welcome! Thank you for watching!

@88sinduja Actually I saw your previous comments on bootstrapping. Which makes sense I guess. Thanks for the vid, made things clear :-)

SORRY!!!! HE DID TELL US!

Floating leg pay-off is unclear.

dude your formula is incorrect

MAIN POINT IS THE DISCOUNT RATE AND THERE HE TELLS US NOTHING, THE DUMMY.