So basically current yield is the return that the investment actually makes in a year. And yield to maturity is the investor's required rate of return. And current yield will keep reducing to ultimately match yield to maturity because an above-par bond price will move downwards towards par thanks to market correction. Alright, let's see if I can understand reinvestment risk now.

There is a graphing functionality in Excel, rather simple to use. I’d search up something like “how to draw charts using Excel”’on UA-cam (Sorry don’t have a video of my own on that!) 😀

Great question! Basically, In order to drive home the point that the total return (YTM) on the bond is comprised of current yield and capital gains (just like a stocks total return is comprised of dividend yield and capital gains). I don’t HAVE to make this assumption - we can still do current yield and capital gains calculation. But if the YTM changes in one year, then the price at the end of one year will adjust accordingly, and the sum of current yield and capital gains will no longer add up to the initial YTM at which the investor bought the bond. Does that help?

Nice, but, isn’t this explanation in fact incorrect? I understand that current yield does not take into account compounded interest but yield to maturity does. If it is like that then in the case of bonds bought at par you should never have a situation where current yield = yield to maturity (as indicated in the video). YTM should always be bigger - because it includes interest on interest on the coupons received.

The distinction between current yield and yield to maturity is not based on compoun interest, per se. YTM accounts for changes in the price of the bond over time, while current yield doesn't. In some sense, it is the same as the distintion between dividend yield and stock return: If you buy a stock for $50, and then one year later you get a $5 dividend, AND the price of the stock is $60, then dividend yield is 10% ($5/$50) and capital gains (or return from price appreciation) is 20% [(60-50)/50]. Thus, your TOTAL return from investing in the stock is 30%. In this example, IF the stock were instead a bond, then you could say that 10% is the current yield, whereas the TOTAL return is the Yield to Maturity [This is not technically correct, but I just want you to understand the conceptual distinction)]. Hope this helps. P.S. No YTM is NOT always bigger than current yield. If the price of the stock decreases, you can make a loss and your total return can be less than your dividend yield. Just like that, if the price of bond falls, YTM can be less than current yield.

Best explanation I've seen

Thank you for your effort, my concept has become more clear after this video

Wow! Fascinating!

Great video, perfectly explained!

Lovely explanation.

So basically current yield is the return that the investment actually makes in a year. And yield to maturity is the investor's required rate of return. And current yield will keep reducing to ultimately match yield to maturity because an above-par bond price will move downwards towards par thanks to market correction. Alright, let's see if I can understand reinvestment risk now.

great stuff

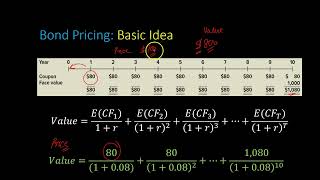

he didint say that the face value was 1000 dollars and without that he cant calculate nothing

That’s true. The $1,000 Face Value is assumed, as that is the most common denomination of Treasuries.

how can I make that excel chart of YTM with changing bond prices?

There is a graphing functionality in Excel, rather simple to use. I’d search up something like “how to draw charts using Excel”’on UA-cam (Sorry don’t have a video of my own on that!) 😀

Why do you assume that YTM does not change after one year?

Great question! Basically, In order to drive home the point that the total return (YTM) on the bond is comprised of current yield and capital gains (just like a stocks total return is comprised of dividend yield and capital gains). I don’t HAVE to make this assumption - we can still do current yield and capital gains calculation. But if the YTM changes in one year, then the price at the end of one year will adjust accordingly, and the sum of current yield and capital gains will no longer add up to the initial YTM at which the investor bought the bond.

Does that help?

Nice, but, isn’t this explanation in fact incorrect? I understand that current yield does not take into account compounded interest but yield to maturity does. If it is like that then in the case of bonds bought at par you should never have a situation where current yield = yield to maturity (as indicated in the video). YTM should always be bigger - because it includes interest on interest on the coupons received.

The distinction between current yield and yield to maturity is not based on compoun interest, per se. YTM accounts for changes in the price of the bond over time, while current yield doesn't. In some sense, it is the same as the distintion between dividend yield and stock return: If you buy a stock for $50, and then one year later you get a $5 dividend, AND the price of the stock is $60, then dividend yield is 10% ($5/$50) and capital gains (or return from price appreciation) is 20% [(60-50)/50]. Thus, your TOTAL return from investing in the stock is 30%.

In this example, IF the stock were instead a bond, then you could say that 10% is the current yield, whereas the TOTAL return is the Yield to Maturity [This is not technically correct, but I just want you to understand the conceptual distinction)].

Hope this helps.

P.S. No YTM is NOT always bigger than current yield. If the price of the stock decreases, you can make a loss and your total return can be less than your dividend yield. Just like that, if the price of bond falls, YTM can be less than current yield.