@Jakers2009 thanks! Just one clarification that is common source of confusion: the gradient (slope) at x is the "dollar duration" rather than duration (note i am careful to say dollar duration when referring to slope of tangent line). b/c duration = dy/dx*-1/P; i.e., "infected" by price. So, above, the gradient is actually -436.95, i.e., -$436 per 100% (1 unit) or ~$4.36 per 1% (rise/run)

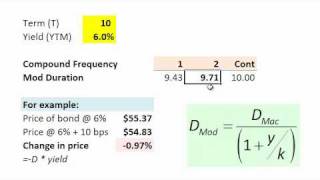

@Jakers2009 Actually, technical correction to my previous reply: the gradient (slope) of the above tangent line at x = 5% is -426.3. That is the "dollar duration" such that the (modified) "duration" = -426 * -1/Price = ~4.458. And modified duration 4.458 = Mac duration / 1 + (y/k) = 4.57 / (1+5%/2); see @4:05

Hi, would you please explain where the 0.5 comes from, from the first example? To calculate the time^2 weighted PV, why add the 0.5? Why not simply time^2?

i think your videos are great - i also resolved my past confussion regarding the duration and the 1st derivative. I realised that the 1st derivative is the gradient function and that if you take the 1st derviative of any function and then substitute the values of the x-axis at any point on that function then you would get the gradient at that point.

Calculate the convexity for a three-year 3.5% coupon rate with a face value of $500,000 loan with amortised payments? How do I do this in excel or on paper?

Thx for video. Need ur help desperately! 1st, Can u say the convexity is a friend at current situation? assuming fed rate keep going up incrementally (ie 25bps) for a short of period of time. 2nd, is 1 yr or 10 yr treasuries more vulnerable to convexity based on the current situation? 3rd, is High yield or treasuries more resilient to increasing convexity? Many thx !

For the Convexity, I'm confused on how you quantified the errors in both the PVs and the convexity calculation. Also, if my bond has semiannual coupons, but I'm only given an annual effective yield, what yield should I be using in the convexity calculation?

From what I understand, the dollar duration cannot be the actual slope of that tangent at that point as these are discrete values plotted at different pointers and for a true tangent, we need a continuous curve really. what is your take on the same sir?

I agree, the dollar duration here seems to be just an approximation of the first derivative of a hypothetical/superimposed continuous price-yield curve

I absolutely love your tutorials. I'm terrible at reading formulas; your examples help me understand them.

If not for these videos, I'd be spending an hour plugging in random numbers in the formula from my textbook LOL

@Jakers2009 thanks! Just one clarification that is common source of confusion: the gradient (slope) at x is the "dollar duration" rather than duration (note i am careful to say dollar duration when referring to slope of tangent line). b/c duration = dy/dx*-1/P; i.e., "infected" by price. So, above, the gradient is actually -436.95, i.e., -$436 per 100% (1 unit) or ~$4.36 per 1% (rise/run)

@Jakers2009 Actually, technical correction to my previous reply: the gradient (slope) of the above tangent line at x = 5% is -426.3. That is the "dollar duration" such that the (modified) "duration" = -426 * -1/Price = ~4.458.

And modified duration 4.458 = Mac duration / 1 + (y/k) = 4.57 / (1+5%/2); see @4:05

Hi, would you please explain where the 0.5 comes from, from the first example? To calculate the time^2 weighted PV, why add the 0.5? Why not simply time^2?

Could not find the spreadsheet

Good video. You mentioned something about opening the spreadsheet. Where is the link to open it please? I just see a video. Thanks.

i think your videos are great - i also resolved my past confussion regarding the duration and the 1st derivative. I realised that the 1st derivative is the gradient function and that if you take the 1st derviative of any function and then substitute the values of the x-axis at any point on that function then you would get the gradient at that point.

Calculate the convexity for a three-year 3.5% coupon rate with a face value of $500,000 loan with amortised payments?

How do I do this in excel or on paper?

@Jakers2009 Yes, i hadn't tackled convexity yet....hard to do quickly, hope you like?

What is the excel?

Cant find spreadsheet

It's Great, thanks..I understood more than on lecture

Thx for video. Need ur help desperately! 1st, Can u say the convexity is a friend at current situation? assuming fed rate keep going up incrementally (ie 25bps) for a short of period of time. 2nd, is 1 yr or 10 yr treasuries more vulnerable to convexity based on the current situation? 3rd, is High yield or treasuries more resilient to increasing convexity? Many thx !

For the Convexity, I'm confused on how you quantified the errors in both the PVs and the convexity calculation. Also, if my bond has semiannual coupons, but I'm only given an annual effective yield, what yield should I be using in the convexity calculation?

APOLOGIES FOR MY BAD ENGLISH .

I can not find the spreadsheet . I could help locate the spreadsheet ? thank you very much

From what I understand, the dollar duration cannot be the actual slope of that tangent at that point as these are discrete values plotted at different pointers and for a true tangent, we need a continuous curve really. what is your take on the same sir?

I agree, the dollar duration here seems to be just an approximation of the first derivative of a hypothetical/superimposed continuous price-yield curve

the second method is sooooo helpful

Great job man, thanks for that! Just wondering if you could send me the spreadsheet or the link. cheers

Amazing videos! Keep it up dood!

how did you plot the graph?

hi david your still doing the bond videos

🎉🎉🎉

Thanks