Conditional fixed-effects logistic model

Вставка

- Опубліковано 24 лют 2022

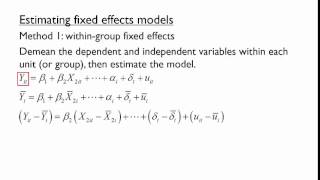

- Estimating fixed effects in multilevel generalized linear models is challenging. This is because increasing the number of clusters (e.g., firms, persons) also increases the number of cluster-level fixed effects that need to be estimated. This is called the incidental parameter problem, and it invalidates the proof that maximum likelihood estimation produces consistent estimates. This is because the presence of cluster means in the model means that when the sample size approaches infinity, so does the number of model parameters.

Conditional logistic fixed effects regression is one workaround to this problem. The conditional logistic regression model assumes that just one observation (or alternatively any other constant number) in each cluster receives a 1 and others receive a 0. This model is useful, for example, for various problems that involve selecting one observation among many alternatives. The lecture explains the problem that conditional fixed effects addresses, how conditional fixed effects logistic regression estimate can be interpreted by calculating predictions or by plotting, and concludes with a simulation that demonstrates why fixed effects are needed. At the end, the conditional fixed effect logistic regression is compared to the linear fixed effects regression model, which is a simpler and useful alternative for many research problems.

Link to the slides: osf.io/n7mgu

bravo! Many thanks! you have offered very constructive and clear explanations!

You are welcome!

do you have reference of paper that uses conditional fixed logistic regression, and how they write the mathematical euqation of the model being estimated, in your example there is no error term.

I would write it in terms of expectations E[y] instead of y. This is what I have seen in empirical applications. If you want to write in in terms of observables, you can just write:

y=logit-1(β0 + β1x1ij + β2x2ij + … + βkxkij + aj ) + uij

But that would be awkward because uij is not independent between observations. Explaining its distribution would be bit challenging for you and your potential readers alike, and for this reason I would use expectations instead of observations in the equation.

Is it possible to have two groups for conditional Logit? I assume it’s not possible? And also does it work for poisson?

Two groups sound awfully small. If your overall sample size is large enough, why not just use a dummy variable to indicate which of the two groups the observation belongs to.

I do not see how conditional model would work conceptually in the case of poisson. How would you conceptually understand the conditional part "the number of selected cases is fixed" and what specific problem would you solve by using conditional poisson?

What about a hybrid effects model? Does it suffer from these same issues?

Defina what you mean by "hybrid effects model". I am unfamiliar with that term.

🇺🇦🤟😂