It is not appropriate, we only check unit Root test, Augmented dickey fuller and Philips person, these boht tests tells us which variable are stationary on level and 1st difference, we can't check stationarity on 2nd difference

Hello Respected, thank you for your lecture, and I have a question as we have seen from your video your optimal lags are(4 4 2) for gdp,co and inv respectively. But how we run ARDL if optimal lags (0 2 4) respectively?

Hi, thank you for your detailed explanation! I have a question for conducting bound test. The result of my bound test shows that F-critical value is bigger than the upper bound so that I can reject the null hypothesis, but the t-critical value is a positive number which is bigger than upper bound as well so that I cannot reject the null hypothesis... Why this will happen? And how can I solve this problem?

Hello sir, thank you for making this video. I find it very useful. I have one question about interpreting my result. I am trying to establish the long run and short-run effect. I have a cointegration in my series, hence I am running "ardl ec". My main question is which short run coefficient I should use to determine the impact of X on Y (ardl ec or ardl)? Is it correct to use "ardl" coefficients on the short run and LR coefficients from "ardl ec" for the long run? As I understand, the only useful information from "ardl ec" are the error correction term and long run coefficients. Is that correct?

For the bounds test, do you use the t-statistic in absolute terms (i.e. do you ignore the negative sign) or consider it as a negative value while analysing whether its is above the lower bound or below the upper bound?

I think there is a mistake in interepreting the long run relationship. The dependent variable in long run is D.gdpn instead of gdpn. Hence consumption 1.67 means with unit rise in consumption the deviation of gdpn from its long run value increases by 1.67 .

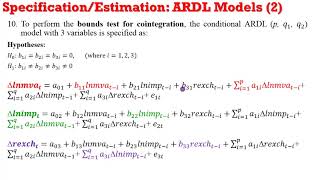

Very nice effort. A few questions.The values of coefficients in the short-run are different when EC command is used compared to only ardl . You said these are to be interpreted as before. Second, in the case of short run should we interpret only the levels coefficient ?. Third please explain what are D1, LD ? I am not good at Stata so asking basic questions.

Interpreted as before means they way interpretation was done before only the value of coefficient will be changed... Secondly it is better to interpret both i.e. Level and interval coefficient

I have a question for you Sir. Your video has been so helpful, but based on the output below, since the F-stat is > I(1) bound at 10% significance level, do i still have cointegration? Grateful if you could help me out i really need to know.... Pesaran/Shin/Smith (2001) ARDL Bounds Test H0: no levels relationship F = 4.008 t = -2.506 Critical Values (0.1-0.01), F-statistic, Case 3 | [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1] | L_1 L_1 | L_05 L_05 | L_025 L_025 | L_01 L_01 ------+----------------+----------------+----------------+--------------- k_3 | 2.72 3.77 | 3.23 4.35 | 3.69 4.89 | 4.29 5.61 accept if F < critical value for I(0) regressors reject if F > critical value for I(1) regressors Critical Values (0.1-0.01), t-statistic, Case 3 | [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1] | L_1 L_1 | L_05 L_05 | L_025 L_025 | L_01 L_01 ------+----------------+----------------+----------------+--------------- k_3 | -2.57 -3.46 | -2.86 -3.78 | -3.13 -4.05 | -3.43 -4.37 accept if t > critical value for I(0) regressors reject if t < critical value for I(1) regressors

hello sir thank you very much for this wonderful explanation please make us estimate ardl panel on stata and how to find the optimal offset (e.g. (1 0 0 2 1) on stata for an ardl panel model

Thank you very much u saved me from my econometrics course!

Very useful the students who have dissertation. Thank you man:)

A HUGE thank you, professor. Very clear explanation

I was hanging around all my day until I come across to your video. It help me so much. Would you mind doing another video?

The video was explained in a simple way. It helped a lot in my Project. Thank you. Keep it up.

You have saved my life. Thank you :)

Thank you for making this video.

Thank you so much for the video. It will be a massive help for the paper I am working on

Thanks, very helpful.

Thank you very much ♥ Useful video ♥

Thank You it is Really Very Interesting

it is Verry interesting. I thank You Very Much

very clear to understand, thanks a lot

Thank you very much

thank you so much sir the video is very informative and it helps me a lot in my research paper.

what a coincidence sheeba. I watched too....really its vey helpful

econ academy listen plz

Yes?

Your video is good. Like your approach to ARDL. Please come again with the interpretation of the short run and long run coefficients.

I will come back to it whenever I have some time INSHAA ALLAH

do we need to perform differencing before running ardl model ?

what will happen if you run an ardl model with a variable that is stationary at second difference?

It is not appropriate, we only check unit Root test, Augmented dickey fuller and Philips person, these boht tests tells us which variable are stationary on level and 1st difference, we can't check stationarity on 2nd difference

Hello Respected, thank you for your lecture, and I have a question as we have seen from your video your optimal lags are(4 4 2) for gdp,co and inv respectively. But how we run ARDL if optimal lags (0 2 4) respectively?

Hi, thank you for your detailed explanation! I have a question for conducting bound test. The result of my bound test shows that F-critical value is bigger than the upper bound so that I can reject the null hypothesis, but the t-critical value is a positive number which is bigger than upper bound as well so that I cannot reject the null hypothesis... Why this will happen? And how can I solve this problem?

both usually has same conclusions. In this case, rejecting the null.

You help me so much with my dissertation. Would you mind doing another video for us, clearer and with more variables?

Hello sir, thank you for making this video. I find it very useful. I have one question about interpreting my result. I am trying to establish the long run and short-run effect. I have a cointegration in my series, hence I am running "ardl ec". My main question is which short run coefficient I should use to determine the impact of X on Y (ardl ec or ardl)?

Is it correct to use "ardl" coefficients on the short run and LR coefficients from "ardl ec" for the long run?

As I understand, the only useful information from "ardl ec" are the error correction term and long run coefficients. Is that correct?

Good job. I like

For the bounds test, do you use the t-statistic in absolute terms (i.e. do you ignore the negative sign) or consider it as a negative value while analysing whether its is above the lower bound or below the upper bound?

T-stats is always use in absolute form

So we disregard negative sign of t stat and negative sign of critical values?

Yes they only show inverse relation between dependent and independent variable

@@econacademy16 thank you so much!!

Hello. What if my R2 is low around 30-40% in the short run. However, in the long run, 60-70-% is it ok?

I think there is a mistake in interepreting the long run relationship. The dependent variable in long run is D.gdpn instead of gdpn. Hence consumption 1.67 means with unit rise in consumption the deviation of gdpn from its long run value increases by 1.67 .

its helpful

Sir please make one video on cointegration test.

Sir,would you tell me the stata command for granger causality tests in ARDL

?

If suppose my variables are stationary at 2nd Difference what shall I do?

Very nice effort. A few questions.The values of coefficients in the short-run are different when EC command is used compared to only ardl . You said these are to be interpreted as before. Second, in the case of short run should we interpret only the levels coefficient ?. Third please explain what are D1, LD ? I am not good at Stata so asking basic questions.

Interpreted as before means they way interpretation was done before only the value of coefficient will be changed... Secondly it is better to interpret both i.e. Level and interval coefficient

Brother good work

Sir , how can I explain the adustment term as shown in the long run results?

thanks, but i want to ask about how to estimate thershold-ardl at stata.thank you again

I have a question for you Sir. Your video has been so helpful, but based on the output below, since the F-stat is > I(1) bound at 10% significance level, do i still have cointegration? Grateful if you could help me out i really need to know....

Pesaran/Shin/Smith (2001) ARDL Bounds Test

H0: no levels relationship F = 4.008

t = -2.506

Critical Values (0.1-0.01), F-statistic, Case 3

| [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1]

| L_1 L_1 | L_05 L_05 | L_025 L_025 | L_01 L_01

------+----------------+----------------+----------------+---------------

k_3 | 2.72 3.77 | 3.23 4.35 | 3.69 4.89 | 4.29 5.61

accept if F < critical value for I(0) regressors

reject if F > critical value for I(1) regressors

Critical Values (0.1-0.01), t-statistic, Case 3

| [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1] | [I_0] [I_1]

| L_1 L_1 | L_05 L_05 | L_025 L_025 | L_01 L_01

------+----------------+----------------+----------------+---------------

k_3 | -2.57 -3.46 | -2.86 -3.78 | -3.13 -4.05 | -3.43 -4.37

accept if t > critical value for I(0) regressors

reject if t < critical value for I(1) regressors

Hi, Could you pls help me learning bayer & hanck cointegration in stata or eviews. thanx

Hello,

I am having collinearity problem when I perform the test. Can you help me out please?

Drop less important variable

@@econacademy16 thank you

hello sir thank you very much for this wonderful explanation please make us estimate ardl panel on stata and how to find the optimal offset (e.g. (1 0 0 2 1) on stata for an ardl panel model

you can watch it from the link given below:

ua-cam.com/video/udgr-iCAp6M/v-deo.html

where is EC coefficient in results?

Sir, please have one lacture on NARDL model in Stata

I will try my best INSHA'ALLAH

good explanation but you spent to much time, it`s possible to make a short video (10 min max)

Sorry but for clear explanation it should take some time