Crystal clear! if the statistical properties can be deduced from a single sufficiently (namely going to inf) long random sample, then the process is ergodic! This is my 3rd video and I finally heard a satisfying definition. Thank you, sir!

Bro Please can u help me by writing here ,What is the exact definition of band width, standard deviation... Because i didn' understand from the next video.. Thanks alot

Very good explanation. I was expecting a numerical example based on the very example of driving a car. That would have made things extremely lucid. Thanks.

Regarding your heuristic description prior to your formal definition: if all you need is that the statistics of a sufficiently long time-segment of your one sample path approximate the statistics of the subsequent future behaviour of that same sample path, then I think you don't need ergodicity - just having stationarity is sufficient. Ergodicity will then give that these statistics are the same across the different sample paths (as in your formal definition) 🙂

Crystal clear! if the statistical properties can be deduced from a single sufficiently (namely going to inf) long random sample, then the process is ergodic! This is my 3rd video and I finally heard a satisfying definition. Thank you, sir!

you have a clear concept

Thanks

I'm taking a communications course and my teacher couldn't even explain it this well. Hope I do well on my exam.

Thanks a lot! Good luck for your exam..

The best explanation ever, thank you from Việt Nam 😍😍😍

Clean Explaination

Thank you a lot!

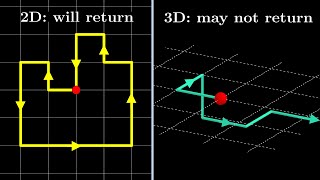

I was reading Nassim Taleb and ergodicity confused me :)

Glad I could help!

Awesome explanation! Thank you very much

Nice explanation, thank you!

Very clearly and patiently explained! Thanks a ton!

Bro Please can u help me by writing here ,What is the exact definition of band width, standard deviation...

Because i didn' understand from the next video..

Thanks alot

Thank you for the explanation. Very clear.

Super clear! ! Thanks a lot

You're welcome!

This fits well with Nassim Taleb's explanation. I was thinking about tyre punctures in the projected scenario.

A tyre puncture or axle break are catastrophe for the scenario you explained, which Taleb might call a Black Swan.

One of the very nice explanation of erogodic process I have seen. Keep it up man.. God bless you

How does this definition relate to the definition that it is a recurrent aperiodic Markov chain?

very clear! Thank you so much!

Glad it was helpful!

Thanks a lot. It was so clear and convincing

Thank you.

very good.thanks

Very good explanation. I was expecting a numerical example based on the very example of driving a car. That would have made things extremely lucid. Thanks.

Thank you. Will look in to that

Bhai so much underrated channel

Bro give a video on random vibration of crankshaft

One of the best explanations so far. Thank you !!

Very clear explanation! Thank you so much!!

thank you so much sir

Regarding your heuristic description prior to your formal definition: if all you need is that the statistics of a sufficiently long time-segment of your one sample path approximate the statistics of the subsequent future behaviour of that same sample path, then I think you don't need ergodicity - just having stationarity is sufficient. Ergodicity will then give that these statistics are the same across the different sample paths (as in your formal definition) 🙂

Good pronounciation.😀

Ha ha .I know my pronunciation is bad! Will try to improve..