Good question! Technically, you are correct, down-arrows in cash flow diagrams should be considered negative values in calculations! Sometimes for problems where the 'sign' doesn't really matter, they are eliminated. I should have mentioned this in the video. I will 'pin' this comment to the top of the comments in case anyone else has the same concern. Thanks!

I really enjoy watching your videos. Everything is explained thoroughly with easy to follow examples. I just don't understand something in this video as well as the video that is ranked before this one in the interest playlist. How are the quarterly (or monthly in the previous video) contributions are factored in the formula for the future value? Because the formula is the same as when there was no regular contributions. I think I might have missed something.

Thanks for the kind words regarding my videos. I'm glad you like them. Yes, I think you are missing an important point. While it 'appears' that the formula for Future Value is the same for annual pmts, quarterly pmts, and monthly pmts, etc. - the values of 'N' and 'i' that are used in the formula are different! ...otherwise, why bother? Please have a look at some of the first videos in the Cash Flow playlist on my main Channel page - I think this would help you.

Greetings, I was wondering, in the alternative method of solving the problem, when the payment was broken into quarterly payments, why did we use 24 instead of 8 since we are dealing with quarterly values and not monthly values? Thank you!

Thanks for the question! In the alternate solution, starting at about 07:00 in the video, the quarterly payments are transformed into 3 equivalent monthly payments. So, after this transformation, we are dealing with 24 periods and 24 payments. I hope this helps.

You could do something similar to what you've described but it would look like this: 1500 (A/F, 0.5%, 3) * (P/A, 0.5%, 24) * (F/P, 0.5%, 24) However, it would be easier to just calculate the FV directly from the equivalent monthly annuity like this: 1500 (A/F, 0.5%, 3) * (F/A, 0.5%, 24) I hope this makes sense!

It's really Amazing to watch yours video, btw I have a question Here we have given that i= 6% comp per month then why we divide 0.06/12 = 0.5%, I mean that due to finding this we have two different "i" values, in question we are given 6% and we have also find another "i" value which is 0.5% ? I am bit of confused here.

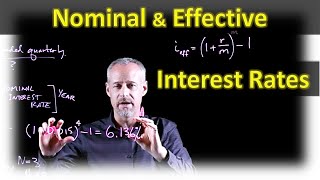

Great question. 6% is what we call the NOMINAL rate. Since the Nominal rate is quoted as "compounded monthly", that tells use we need to divide by 12 to get a monthly rate which is the true mathematical rate we use in the time value of money calculations...this is just how the financial world quotes interest rates. You just need to learn how to interpret the words. Please note, when we use a rate of 0.5% interest (i), we must use a value of N measured in months! Please search for my video explaining "Nominal and Effective Interest Rates".

Very reasonable to not understand that! The explanation has its own video! Watch my video on Nominal and Effective interest rates. How interest rates are quoted follow rules that you just need to learn!

Start with this video: ua-cam.com/video/aT1n_bbQQbM/v-deo.html Then I invite you to explore my video playlist titled: "Interest". ua-cam.com/play/PLcfz9wmNxKqjTG5dsXDnIyUT8mCtA44Wu.html You will need to understand how to manipulate nominal and effective interest rates before you can move on with more time-value-of-money calculations. Good luck!

F/A is a special notation used in finance. It represents a time-value-of-money-compound-interest-factor. F stands for 'future' and A stands for 'annuity'. You read this factor as "F given A". The formula for this factor is [((1+i)^n - 1) / i ], where i is the interest rate for each period and n is the number of periods. You are 'given' A (the annuity, i.e. the regular payments each period), and you calculate the Future value 'F' by multiplying A * (F/A). I would encourage you to visit my main channel page to link to other videos that explain all of this. Good luck!

hello sir thank you so much for such a informative and easy to understand video. i have one question that how to solve this equation = 1500(F/a,1.5075%, 8) , by solving [(1-i)^n - 1]/i , i am getting 1036.07 answer and afTER THAT i am not getting the 12652.61 answer can you please explain how to calculate it ? thank you

Hi sir, thank you so much for your videos, it helps so much for my exam. Just another dump question, I think, if the interests rate is 6% annual, isn’t the interest rate for a quarter is 1.5%. I know it’s not but I still can’t quite grab the concept of effective interest rate?

In this problem the interest is 6% compounded monthly. In this case, the monthly interest rate is 0.5% (6%/12). This means the effective quarterly rate is (1 + 0.005)^3 -1, or about 1.5075125%. You should review my video on Nominal and Effective interest rates. I hope my other videos will help you.

@EngineeringEconomicsGuy thank you so much sir. I get it now after going through your Interest Playlist. You are literally saving me days of self studying.

If you can divide the yearly interest rate of 6% by 12 to get the monthly one, why can't you just muliptly the monthly one by 3 to get the quarterly one?

Excellent question! Welcome to the 'conventions' for compound interest. If a rate is 'quoted' as "6%-compounded-monthly", that MEANS - by definition - that you divide 6% by 12 (for 12-months in a year). You then use 0.5% as the true mathematical compound interest rate with 'months' as the compounding period. You just need to learn this convention. Watch my video on "Nominal and Effective Interest" for a good description. Also watch my video on 'Continuous Interest' for an explanation of 'WHY' the financial world uses this convention... it actually does make sense! Hope this helps.

so do you only use the effective interest rate equation when compounding is less than payment periods & round-up annuity to the given compounding period if it is greater than the payment period? (disregarding the second method you showed, I found that a bit confusing)

I think I understand what you're asking... perhaps if you watch my other video titled "Compounding Less Frequent than Payments" you will get clarification. If not, please comment again and I will try to answer again.

@@EngineeringEconomicsGuy i have. what i got out of it was, you make the compounding period irate equivalent to the annuity period but converting to effective int rate. & when comp period is more than annuity period you just add up the annuities that come in between to the end of each compounding period therefore just using the r/m equation & not the i(eff). would that be correct ?

@@EngineeringEconomicsGuy thank you for taking the time to respond! your explanations are perfect 🙏🏾 feeling confident going into my exam this coming week!

Why is the value of Annuity(1500) not represented as -1500 in the calculations. I am confused.

Good question! Technically, you are correct, down-arrows in cash flow diagrams should be considered negative values in calculations! Sometimes for problems where the 'sign' doesn't really matter, they are eliminated. I should have mentioned this in the video. I will 'pin' this comment to the top of the comments in case anyone else has the same concern. Thanks!

I love how u just taught me what my professor couldn't in 5 minutes, Thank u soo much !!!!!!

You are so welcome!

Best youtube channel sir very helpful for commerce and economics student

Thank you! Glad you like it!

Thank You so much for making it easier to understand

You are most welcome! I'm happy to help.

This is the best video ever thank you so so much for this video

I'm not sure it's the "best video ever", but I definitely appreciate the kind words! Good luck in your Engineering Economics course!

I really enjoy watching your videos. Everything is explained thoroughly with easy to follow examples. I just don't understand something in this video as well as the video that is ranked before this one in the interest playlist. How are the quarterly (or monthly in the previous video) contributions are factored in the formula for the future value? Because the formula is the same as when there was no regular contributions. I think I might have missed something.

Thanks for the kind words regarding my videos. I'm glad you like them. Yes, I think you are missing an important point. While it 'appears' that the formula for Future Value is the same for annual pmts, quarterly pmts, and monthly pmts, etc. - the values of 'N' and 'i' that are used in the formula are different! ...otherwise, why bother? Please have a look at some of the first videos in the Cash Flow playlist on my main Channel page - I think this would help you.

thank you so much, sir. hopefully you would save me from today's test

I hope so too! Good luck!

Greetings, I was wondering, in the alternative method of solving the problem, when the payment was broken into quarterly payments, why did we use 24 instead of 8 since we are dealing with quarterly values and not monthly values? Thank you!

Thanks for the question! In the alternate solution, starting at about 07:00 in the video, the quarterly payments are transformed into 3 equivalent monthly payments. So, after this transformation, we are dealing with 24 periods and 24 payments. I hope this helps.

I have a quick question here: we we push everything to P and then find F? I was doing something like: 1500(A/F,0.5,3)(P/A,0.5,3)(F/P,0.5,8) ?

You could do something similar to what you've described but it would look like this: 1500 (A/F, 0.5%, 3) * (P/A, 0.5%, 24) * (F/P, 0.5%, 24)

However, it would be easier to just calculate the FV directly from the equivalent monthly annuity like this: 1500 (A/F, 0.5%, 3) * (F/A, 0.5%, 24) I hope this makes sense!

It's really Amazing to watch yours video, btw I have a question

Here we have given that i= 6% comp per month then why we divide 0.06/12 = 0.5%, I mean that due to finding this we have two different "i" values, in question we are given 6% and we have also find another "i" value which is 0.5% ? I am bit of confused here.

Great question. 6% is what we call the NOMINAL rate. Since the Nominal rate is quoted as "compounded monthly", that tells use we need to divide by 12 to get a monthly rate which is the true mathematical rate we use in the time value of money calculations...this is just how the financial world quotes interest rates. You just need to learn how to interpret the words. Please note, when we use a rate of 0.5% interest (i), we must use a value of N measured in months! Please search for my video explaining "Nominal and Effective Interest Rates".

Thank you for great explanation professor.

You are most welcome! Good luck in your course!

I don't not get the division of the interest by 12

Very reasonable to not understand that! The explanation has its own video! Watch my video on Nominal and Effective interest rates. How interest rates are quoted follow rules that you just need to learn!

@@EngineeringEconomicsGuy

Where can I get those videos please

Start with this video: ua-cam.com/video/aT1n_bbQQbM/v-deo.html

Then I invite you to explore my video playlist titled: "Interest".

ua-cam.com/play/PLcfz9wmNxKqjTG5dsXDnIyUT8mCtA44Wu.html

You will need to understand how to manipulate nominal and effective interest rates before you can move on with more time-value-of-money calculations.

Good luck!

Thank you for explanation

You're welcome!

Isn't there a formula for when the compundind frequency is less than payment frequency

There isn't really a formula, however, you may find the companion-video helpful: ua-cam.com/video/plotBZ-kvpc/v-deo.html

Sorry, what does "F/A" mean? Where do I get "F" to divide it by "A"?

F/A is a special notation used in finance. It represents a time-value-of-money-compound-interest-factor. F stands for 'future' and A stands for 'annuity'. You read this factor as "F given A". The formula for this factor is [((1+i)^n - 1) / i ], where i is the interest rate for each period and n is the number of periods. You are 'given' A (the annuity, i.e. the regular payments each period), and you calculate the Future value 'F' by multiplying A * (F/A). I would encourage you to visit my main channel page to link to other videos that explain all of this. Good luck!

Thank you@@EngineeringEconomicsGuy

hello sir thank you so much for such a informative and easy to understand video.

i have one question that how to solve this equation = 1500(F/a,1.5075%, 8) , by solving [(1-i)^n - 1]/i , i am getting 1036.07 answer and afTER THAT i am not getting the 12652.61 answer can you please explain how to calculate it ? thank you

i got it sir . please don't waste your time explaining this . thank you

OK - thanks! Good luck in your course!

Hi sir, thank you so much for your videos, it helps so much for my exam. Just another dump question, I think, if the interests rate is 6% annual, isn’t the interest rate for a quarter is 1.5%. I know it’s not but I still can’t quite grab the concept of effective interest rate?

In this problem the interest is 6% compounded monthly. In this case, the monthly interest rate is 0.5% (6%/12). This means the effective quarterly rate is (1 + 0.005)^3 -1, or about 1.5075125%. You should review my video on Nominal and Effective interest rates. I hope my other videos will help you.

Here is the link: ua-cam.com/video/aT1n_bbQQbM/v-deo.html

@EngineeringEconomicsGuy thank you so much sir. I get it now after going through your Interest Playlist. You are literally saving me days of self studying.

a nice video !! Thank u so much !!

You're welcome! Glad you liked it!

If you can divide the yearly interest rate of 6% by 12 to get the monthly one, why can't you just muliptly the monthly one by 3 to get the quarterly one?

Excellent question! Welcome to the 'conventions' for compound interest. If a rate is 'quoted' as "6%-compounded-monthly", that MEANS - by definition - that you divide 6% by 12 (for 12-months in a year). You then use 0.5% as the true mathematical compound interest rate with 'months' as the compounding period. You just need to learn this convention. Watch my video on "Nominal and Effective Interest" for a good description. Also watch my video on 'Continuous Interest' for an explanation of 'WHY' the financial world uses this convention... it actually does make sense! Hope this helps.

@@EngineeringEconomicsGuy Thank you!

so do you only use the effective interest rate equation when compounding is less than payment periods & round-up annuity to the given compounding period if it is greater than the payment period? (disregarding the second method you showed, I found that a bit confusing)

I think I understand what you're asking... perhaps if you watch my other video titled "Compounding Less Frequent than Payments" you will get clarification. If not, please comment again and I will try to answer again.

ua-cam.com/video/plotBZ-kvpc/v-deo.html

@@EngineeringEconomicsGuy i have. what i got out of it was, you make the compounding period irate equivalent to the annuity period but converting to effective int rate. & when comp period is more than annuity period you just add up the annuities that come in between to the end of each compounding period therefore just using the r/m equation & not the i(eff). would that be correct ?

Yes, I think you've got it!

@@EngineeringEconomicsGuy thank you for taking the time to respond! your explanations are perfect 🙏🏾 feeling confident going into my exam this coming week!

Thank you so much that was helpful

Glad it helped

Thank you so much sir!

Most welcome!

I wish you all the best in your studies!

@@EngineeringEconomicsGuy Really appreciated!!

Isn't it 0.06/12 = 0.005 instead of 0.5

Yes! However, 0.5% is the same as 0.005, but I can see the potential for confusion! Thanks for the comment.