Bond Duration Explained Simply In 5 Minutes

Вставка

- Опубліковано 14 чер 2024

- Ryan O'Connell, CFA, FRM explains bond duration simply.

Chapters:

0:00 - Bond Duration Definition

0:27 - Key Factors Affecting Bond Duration

2:01 - How to Calculate Macaulay Duration

🎓 Tutor With Me: 1-On-1 Video Call Sessions Available

► Join me for personalized finance tutoring tailored to your goals: ryanoconnellfinance.com/finance-tutoring/

📚 CFA Exam Prep Discount - AnalystPrep:

► Get 20% off CFA Level 1, 2, and 3 complete courses with promo code "RYAN20". Explore here: analystprep.com/shop/all-3-levels-of-the-cfa-exam-complete-course-by-analystprep/?ref=mgmymmr

*Disclosure: This is not financial advice and should not be taken as such. The information contained in this video is an opinion. Some of the information could be wrong. This channel is owned and operated by Portfolio Constructs LLC. Some of the links above are affiliate links, meaning, at no additional cost to you, I will earn a commission if you click through and make a purchase.

🎓 Tutor With Me: 1-On-1 Video Call Sessions Available

► Join me for personalized finance tutoring tailored to your goals: ryanoconnellfinance.com/finance-tutoring/

Finally I was able to understand how duration is calculated. Thanks for the clear and well-organized explanation.

Great to hear! My pleasure Bovino

This is the only explanation that I ever understood! It’s bothered me decades that I never understood it. Thanks.

I have watched videos of 30- 60 Mins on Duration and none of those explained the meaning and calculation so easy to understand as yours. Thanks man.

The best explanation ever! literally summarised 2 weeks of uni lecture into 5 mins. Brilliant work!

Thank you so much! It means a lot

Thanks for the explanation. Really liked your approach in making it easy to understand.

I like how you breakdown everything, it's a lot easier to understand. ty :)

Glad it was helpful Alyssa! I try to make it as simple as possible

Thank you! This really helped me for my level 1 CFA study

My pleasure and glad it helped!

I really enjoyed a discussion of bonds that develops it beyond "if interest rates go up, the price of the bond will go down and vice versa". Thank you!

My pleasure, there is a lot more to it than that!

At last!!!someone who actually makes sense..thanks mate!!!

Appreciate the feedback Nkosi!

Great video and done so easy to comprehend. Thank you

My Mahendra! Thanks for the feedback

Thank you for the explanation, you just solved my problem.

My pleasure and thanks for the feedback Guobo!

Thank you soooo much, finally got that part! Wish you all the best!

Glad it helped! Thank you

thank you for the explanation, very well explained

Glad it was helpful!

Easiest way to understand.....thnk a ton

Thank you Priti!

I love you, Ryan! Not in weird way, just a big fan of your teaching😊

Haha thank you! I really appreciate the support 🙏

THANKS A LOT...... GOT CLARITY.. VERY USEFUL FOR MY PROFESSIONAL COURSE❤

Glad to hear that!

Finally someone explain it clearly

Appreciate it!

Great Explanation !

Glad you liked it!

Quick question, isn't modified duration what tells you how the price of a bond reacts to changes in interest rates while duration is the number of years for a bond to repay the investor?

I LOVE YOU!! You explain amazingly. Thanks so much for this amazing content!

It is my pleasure Lidia! Thanks for the nice comment

Well explained.Thanks so much.

Personally I think they could have used a better word than "Bond duration" for this. it doesn't make much intuitive sense why the word duration will be used for such a sensitivity calculation.

Glad it was helpful! It is also a measure of duration of time outstanding until you expect to get the payments for the bond so I think that is why they called it duration

This is FUCKING AMAZING THANK YOU SO MUCH!

Very short and clear explanation

Glad it was helpful!

Finally, I understand

Glad to hear!

太感谢你了!

Thank you!

You're welcome!

爱你的教程,love from China

Much appreciated!

Good explanation

Thank you!

Thank you ☺️

You’re welcome 😊

God bless you this is super helpful

Thank you!

Great video. Loved the explanation of the friend owing you money. Would you be able to explain intuitively why bonds with lower yields have higher durations?

Yes, it is because the lower the yield, the lower the coupon, which means you will be getting your money back later on. For example, a zero yield bond will pay no coupons and all of the money will be paid back at the very end. So with lower yields, it takes longer time (or a higher duration of time) to get the money back from the loan

Thank you 😭

No problem 😊

You are the GOAT

Much appreciated!

You are combining two measurements of duration.

Macauley is a measurement of time in which, for example, the appreciation gain of the bond due to a decrease in interest rates, is completely off set by the re-investment risk assumed by YTM. YTM assumes that the coupon payments can be re-invested at the YTM, when rates drop, the coupon payments must be reinvested at a lesser rate, this lowers overall YTM. At the same time, the bond appreciates due to the interest rate decrease - raising YTM. The point in time in which these two values are completely off-setting is Macauley Duration.

Modified duration is the sensitivity change to bond prices with a change in interest rates.

Hello, this video is a simplified explanation of duration! The explanation you provided conflates a few distinct financial concepts. Macaulay Duration measures the time it takes to recover a bond's cost through its cash flows, not the specific interaction between price appreciation and reinvestment risk that you've described. Modified Duration, on the other hand, accurately captures a bond's price sensitivity to interest rate changes, separate from the concept of Yield to Maturity (YTM), which deals with the total expected return assuming all payments are reinvested at the YTM rate.

For anyone looking for an accurate and nuanced video on the differences between macaulay, modified and effective duration, you can find that here: ua-cam.com/video/2tXjJR1W0YU/v-deo.html

Just to be clear, this example would have the bond only paying 1 annual coupon payment right? In reality most bonds pay semi-annual right?

Yes, that is correct. I find it easier to explain by using an annual bond as an example

@@RyanOConnellCFA Hey, thank you for the response. Do you have a video example using semi-annuals? Or is the calculation the same? I have seen it done a couple different ways with regards to the discount factors exponent ...some use 1 2 3 4 5 6...while some use 1, 1.5, 2, 2.5, etc. I noticed the results are different. (I maybe calculating it wrong)

How can IRS hedge portfolio duration?

Great video btw and you just earned yourself a new subscriber!

Thanks Mirza! I think this article will answer your question better than I could in a simple comment:

etfdb.com/rising-interest-rates/duration-hedging-and-rising-rates/

Does that help?

@@RyanOConnellCFA great video, thanks.

@@robertcesar9752 Much appreciated my friend

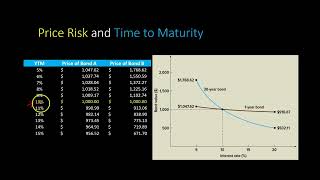

I get how a bond duration tells you its price sensitivity in connection to a change in market interest rates. Doesn't Duration also tell you how long it takes for the investor to get their money back on their investment? If so, what would the 2.75 mean in terms of that?

Yes, you're correct that bond duration can also be interpreted as the length of time it takes an investor to recoup their investment in a bond. However, it's important to note that it's not simply a matter of waiting 2.75 years in the case of a bond with a duration of 2.75. Rather, duration in this sense is a weighted average of the present value of a bond's cash flows, which include periodic interest payments and the eventual repayment of the bond's face value.

What this means is that if a bond has a duration of 2.75, the investor would, in theory, recover their initial investment over the course of 2.75 years, considering both the regular coupon payments and the principal repayment, and adjusted for the time value of money.

However, this assumes a constant interest rate environment, which is rarely the case. Changes in market interest rates can significantly impact the actual time it takes to recoup an investment, which is why duration is also used as a measure of a bond's sensitivity to interest rate changes.

Remember, lower duration means lower interest rate risk, and vice versa. So, a bond with a 2.75 duration would be less sensitive to interest rate changes compared to a bond with higher duration.

@@RyanOConnellCFA helps. Thank you 🙏🏼

So if the Macaualy Duration is 2.5Yr. That means it takes us 2.5 yr to recover our initial investment, and also means if rates go up 1% that our price changes by 2.5%? What confuses me is how the concept of years and % is interchangeable

That is not entirely correct. You are thinking about it more like a break even point of a project you'd learn about in corporate finance. It is a weighted average, not a breakeven time period. The percentage change component of what you said is correct however. Just know this is a simplified assumption that doesnt account for convexity

@@RyanOConnellCFA Got it, thank you.

Wouldn't the 2.75 that you calculate at the end be the modified duration, not the Macaulay duration as it is measuring the % change to a 1% change in interest rates and not measuring the time in years??

It is the Macaulay Duration that I calculated but you are correct that the Modified Duration better describes the relationship of how bond prices change with yield. Check out this video that I just published that goes into the nuanced details of Macaulay Duration, Modified Duration, and Effective Duration: ua-cam.com/video/2tXjJR1W0YU/v-deo.html

it actually is the Macauley duration but the last sentence is wrong in my opinion. The unit of the macaulay duration is years and not unitless..

Thanks for clarifying this. I know understand that Macaulay duration is the years required to receive the fixed cash flows from the bond. Modified duration measures the sensitivity of the bons price to changes in int. Rate.

life saving love fromhong kong

Thats great! Glad you enjoyed

The video won’t load

I think this has more to do with your internet connection than the video or UA-cam

So, regard Macaulay duration (not ModMacDur) - can it be thought of as the amount of time to receive your initial purchase price back? Essentially the break even amount of time?

Yes. Think like you would with discrete probability: at each time, there's a proportion of the bond's price that occurs at that time. MacDur is then the "expected time" regarding these proportions (i.e. "probabilities").

Hey Erick, I wouldn't necessarily say break even point as you don't make money on every bond (due to an uncertain interest rate environment). It is the weighted average amount of time that you expect the present value cashflows to pay out. Don't worry about the initial price you paid