you're actually a better teacher some of my finance professors in college (I was gonna do banking but ended up in prop so I'm watching these as a refresher before my internship ends and I gotta do the interview for the full time job) Thanks a bunch

Hi Mahyar: History informs params but that's all: it gives us average & volatility. But then I don't use history, i.e., for normal (parameteric) distribution. I use only the smooth (but unrealistic) curve. A HISTORICAL SIM has NO params. For historical sim, you only need to SORT the historical return and look down the list to 95th-99th %ile, etc. You have a point, under most VaR approaches, historical series at least implicitly informs going-forward model. Thanks for viewing!

Brian, of course you are correct. The reason the normal is used (here and often) is merely to introduce VaR as the quantile of a distribution (i.e., any distribution!) ... those normal is friendliest to the new learner...once we explain how VaR is "merely a quantile" then we can deal in the various approaches, parameteric or otherwise...although re: power law & heavy-tail distributions, you still have the issue of "does any parametric distribution" *really* fit the tail? David

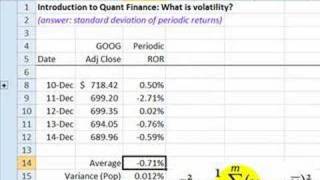

David, Thanks for posting these videos. I'd like to point out one oversight in this illustration. When the mean is non-zero (here, it is -0.71%), you must take it into account. So in your spreadsheet, C18 should =C14+C16*C17. Of course, the mean is commonly approximately zero and can be ignored, but in this example it's worth including. Thanks again for posting these videos, they are useful! Aviad

Thanks Aviad, I appreciate that. And I agree, I am showing the so-called absolute VaR without reference to the mean; which is sort of okay for short trading (daily or less) periods. But yours (so-called relative VaR) is just better as it is the general case and treats VaR as the unexpected loss. Thanks for making this point! David

@akathetruthteller right, agreed but it's not incorrect so much as i should have clarified this is a relative VaR not an absolute VaR where the relative VaR ignores the drift (i.e., relative to future expected value) and the absolute VaR--to your point-- is the VaR reduced by the drift (if drift is zero, they are the same). Please note my comment from two years ago has the terms mistakenly reversed, should be: relative VaR = volatilty*deviate absolute VaR = -mean + volatilty*deviate thanks!

I am a casual student of econ/finance, and this has always perplexed me. If the normal distribution is so clearly an false assumption for the distribution of many different types of asset returns, does mathematical expediency truly make its use necessary? Why not use (at least) a "fat-tailed", or even a skewed (asymmetrical) variant as the standard density function for financial practice, depending on the historical data?

David, thank you! Simplification of the complex things makes me understand quant finance. Also could tell me please how to create a chart of density in Excel?

@briano8713 Yes, historically, bubbles and crashes appear when the markets move several standard deviations beyond the "historical mean"(historical mean is useless, since the inputs to that mean are changing every second with new data/behavior).

Hi sir..i am new to your channel..started from old ..just wanted to point out the formula used is for volatility, is the population not for saample .. should we use this? Thanks anyway for explaining

@Bionic, how did you get cell C8, that first return? are you supposed to show one more data point of last Friday price, if you use it? Or you don't use it? Confused. Please advise, thanks.

Very helpful indeed, thanks a lot for sharing. Just one question, what is the difference between the losses wont exceed -1.80% and the losses wont exceed say 1.80%?

i have to ask that basically value at risk is that .05% loss? then what will be the other0.95%? please answer me i am very confusing in this point an i am new in this and why we use quantile function here?

Tell me, David! Can VaR be considered the expected loss (for a high enough probability)? For instance, if you know the value of the asset along with the default probability, can you compute VaR? Is the VaR(%) in that case the default probability itself? Thank you and keep up the good work (love your videos)! Vlad

in VaR Variance Covariance method, Stock returns we physically convert into normal distribution or just we assume that returns are normally distributed ? Please answer ASAP....I M WAITING...

Hi! I also do not think this is correct. You say that VaR is z-alpha*std away from zero which you implicitly assume to be the mean. This would only be the case if you assume that the distribution is standard normal. Nevertheless, your mean is -0.71% so sth is wrong here. What about VaR=z-alpha*std - 0.0071 ?

dude, i don't think your VAR calculation is correct. your assuming that the distribution of the return has mean 0 then the var is simply a scaled variance.but you didn't mention anywhere that your are assuming that the access return is 0. or risk free

The Gaussian has proven to be a terrible predictor of extreme events in this context, and other methods (like using a "power law" or a polynomial with scale invariance) have been much more accurate. What gives?

you're actually a better teacher some of my finance professors in college (I was gonna do banking but ended up in prop so I'm watching these as a refresher before my internship ends and I gotta do the interview for the full time job)

Thanks a bunch

Hi Mahyar: History informs params but that's all: it gives us average & volatility. But then I don't use history, i.e., for normal (parameteric) distribution. I use only the smooth (but unrealistic) curve. A HISTORICAL SIM has NO params. For historical sim, you only need to SORT the historical return and look down the list to 95th-99th %ile, etc. You have a point, under most VaR approaches, historical series at least implicitly informs going-forward model. Thanks for viewing!

Brian, of course you are correct. The reason the normal is used (here and often) is merely to introduce VaR as the quantile of a distribution (i.e., any distribution!) ... those normal is friendliest to the new learner...once we explain how VaR is "merely a quantile" then we can deal in the various approaches, parameteric or otherwise...although re: power law & heavy-tail distributions, you still have the issue of "does any parametric distribution" *really* fit the tail? David

David,

Thanks for posting these videos. I'd like to point out one oversight in this illustration. When the mean is non-zero (here, it is -0.71%), you must take it into account. So in your spreadsheet, C18 should =C14+C16*C17.

Of course, the mean is commonly approximately zero and can be ignored, but in this example it's worth including.

Thanks again for posting these videos, they are useful!

Aviad

Thanks Aviad, I appreciate that.

And I agree, I am showing the so-called absolute VaR without reference to the mean; which is sort of okay for short trading (daily or less) periods. But yours (so-called relative VaR) is just better as it is the general case and treats VaR as the unexpected loss. Thanks for making this point!

David

@TheStormPulse I don't think we have one, I added to our requested topics list, thanks for your interest!

@akathetruthteller right, agreed but it's not incorrect so much as i should have clarified this is a relative VaR not an absolute VaR where the relative VaR ignores the drift (i.e., relative to future expected value) and the absolute VaR--to your point-- is the VaR reduced by the drift (if drift is zero, they are the same).

Please note my comment from two years ago has the terms mistakenly reversed, should be:

relative VaR = volatilty*deviate

absolute VaR = -mean + volatilty*deviate

thanks!

I am a casual student of econ/finance, and this has always perplexed me.

If the normal distribution is so clearly an false assumption for the distribution of many different types of asset returns, does mathematical expediency truly make its use necessary? Why not use (at least) a "fat-tailed", or even a skewed (asymmetrical) variant as the standard density function for financial practice, depending on the historical data?

Samran, belatedly: thank you for liking the videos! David H

Bionic Turtle, you are a God among Quants.

David, thank you! Simplification of the complex things makes me understand quant finance.

Also could tell me please how to create a chart of density in Excel?

@briano8713 Yes, historically, bubbles and crashes appear when the markets move several standard deviations beyond the "historical mean"(historical mean is useless, since the inputs to that mean are changing every second with new data/behavior).

Hi sir..i am new to your channel..started from old ..just wanted to point out the formula used is for volatility, is the population not for saample .. should we use this? Thanks anyway for explaining

@Bionic, how did you get cell C8, that first return? are you supposed to show one more data point of last Friday price, if you use it? Or you don't use it? Confused. Please advise, thanks.

Very helpful indeed, thanks a lot for sharing. Just one question, what is the difference between the losses wont exceed -1.80% and the losses wont exceed say 1.80%?

i have to ask that basically value at risk is that .05% loss? then what will be the other0.95%? please answer me i am very confusing in this point an i am new in this and why we use quantile function here?

Very well explained, thanks matey

Thank you for watching!

@prodigee411 Do you mean to say trend-following (as an approach) creates the observed fat-tailed/asymmetric distributions of returns?

Tell me, David! Can VaR be considered the expected loss (for a high enough probability)? For instance, if you know the value of the asset along with the default probability, can you compute VaR? Is the VaR(%) in that case the default probability itself? Thank you and keep up the good work (love your videos)! Vlad

in VaR Variance Covariance method, Stock returns we physically convert into normal distribution or just we assume that returns are normally distributed ?

Please answer ASAP....I M WAITING...

Does anyone know if there is a bionic turtle video about "spectral risk measure"? - I can't find one at least

do you have vdo about copula VaR? I really need it.

thanks ^^

Thank you very much. Very informative. Subscribed.

i thing the correct is VaR=z*std - 0.0071. right?

Hi! I also do not think this is correct. You say that VaR is z-alpha*std away from zero which you implicitly assume to be the mean. This would only be the case if you assume that the distribution is standard normal. Nevertheless, your mean is -0.71% so sth is wrong here. What about VaR=z-alpha*std - 0.0071 ?

dude, i don't think your VAR calculation is correct. your assuming that the distribution of the return has mean 0 then the var is simply a scaled variance.but you didn't mention anywhere that your are assuming that the access return is 0. or risk free

Can you just write my textbook? My textbook is horrible at explaining everything.

The Gaussian has proven to be a terrible predictor of extreme events in this context, and other methods (like using a "power law" or a polynomial with scale invariance) have been much more accurate. What gives?

@briano8713 Trend Following.