Maybe it's not clear to you, but my video is about financial volatility not chemistry. Even in finance, volatility has five (5) different definitions. One of my pet peeves is the tendency, sometimes borne of academic hubris, to assume that some words are "owned" and/or concrete. To use stable here would be utterly confusing. Only the Ego wants to confuse. Humpty Dumpty the wise egg said, the word means what I choose it to mean...

I like the comparison of equation to transposing into Excel for it gives a complete . Don't discount a 7 day to 14 day time frame as being too short. When trading earnings this is the best time frame for volatile assets prior and after releasing their Earnings Per Share. Totally blown away by your break down of the equation when calibrating it to Excel.

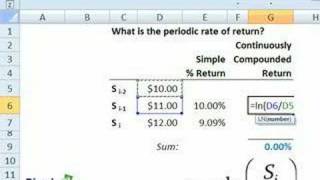

he doesn't have dec-9 shown, but I assume he would take the natural logarithm of google's close on dec 10 divided by google's close on dec 9 ... =ln(B8/B7)

Maybe it's not clear to you, but my video is about financial volatility not chemistry. Even in finance, volatility has five (5) different definitions. One of my pet peeves is the tendency, sometimes borne of academic hubris, to assume that some words are "owned" and/or concrete. To use stable here would be utterly confusing. Only the Ego wants to confuse. Humpty Dumpty the wise egg said, the word means what I choose it to mean...

@linagee Thanks, considering this one one of my first videos (over 4 years ago) and I can't bear to view the early ones :(

I like the comparison of equation to transposing into Excel for it gives a complete . Don't discount a 7 day to 14 day time frame as being too short. When trading earnings this is the best time frame for volatile assets prior and after releasing their Earnings Per Share.

Totally blown away by your break down of the equation when calibrating it to Excel.

Is this a daily volatility or annual volatility for rate of return?

I think the variance should be 1/m-1 since its the sample variance, except I am missing something.

No, you are correct. Turtle is using the population rathen than the sample, m-1, to account for degrees of freedom.

he doesn't have dec-9 shown, but I assume he would take the natural logarithm of google's close on dec 10 divided by google's close on dec 9 ... =ln(B8/B7)

Right

Nice introduction. Thanks, Kukan

Thank you so much. Very helpfull!...

You're welcome! We are happy to hear that our video was so helpful :)

@yellowwitch1 You are watching this...

Thank you

very nice.. brow...

Denmark