why is s&p the independent variable? it should be the other way around since s&p is the representation off of the rest of market movements depending on the performances of top 500 companies.

Very well done! you have explained some complex concepts in very simple terms. Can you also suggest me some resources from where I may learn statistical terms and their implementation in excel?

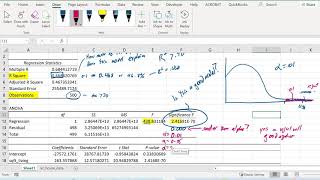

This is good but with R squared of 0.10 interprets there is no Determination i.e. only 10% of variance is identified by the model equation and further with very weak correlation R of 0.31.

when we are using daily data of stock index and comparing it with some other variable for which you have also daily data available. For instance, I have been encounavailableterd a problem that daily data of stock is not available as Sat and Sun are off days. What should i do

Closing price is just the last price in trading day. so if stock split than you could find your stock half at closing and you would die if see your stock price got down from 20 to 10 but you won't find this prom in adjusted price. So it is more acceptable for traders.

so i download s&p and its one of the company IBM one years or so record right? Hello Sir can you interpret one of the data i prepared... This is from my countries stock exchange.

I don't think so, because it is the independent variable. IBM's growth is dependent on the growth of the market as a whole to an extent, so it is the dependent variable, y.

I don't see why this doesn't have a million views. This is one gnarly video. I was able to do it for my paper!

Words cant explain how much this helped me with my research paper. Thank you so much for the great explanation and details

Keep it up, u r really contributing to youtube, its creating value

why is s&p the independent variable? it should be the other way around since s&p is the representation off of the rest of market movements depending on the performances of top 500 companies.

Very well done! you have explained some complex concepts in very simple terms. Can you also suggest me some resources from where I may learn statistical terms and their implementation in excel?

Thank you, this helped me through my Finance 101 class!

Excellent video and perfect explanation. Many thanks for the video and time dedicated to making this video!

THIS SO AMAZING FOR MY ASSIGNMENT

THANKS!I REALLY NEED THIS! I ALMOST FAILED MY COURSE T_T

Thank you helped me a lot, with an assignment I am about to do.

Thank you for your excellent videos, very educational and direct to the point! keep up the good work :)

Genius! made it soo easy to follow! huge help for my securities analysis class!

Thank you a lot for this video! You helped me to save a lot of time

thank you so much...great help

This is good but with R squared of 0.10 interprets there is no Determination i.e. only 10% of variance is identified by the model equation and further with very weak correlation R of 0.31.

Very well explained. It helped me a lot in my project. Thank you!

THANK YOU. That was very helpful and easy to understand

Good explanation. Many thanks

I LOVE THIS GUY!

Shouldnt we first verify regression assumptions ?

Why would you do that though? This is such a powerful method for getting the answer you want (shakes magic 8 ball).

thank you

thank you so much sir for being helpful

Excellent.. very much informative

Great and informative video, thanks!!

when we are using daily data of stock index and comparing it with some other variable for which you have also daily data available. For instance, I have been encounavailableterd a problem that daily data of stock is not available as Sat and Sun are off days. What should i do

Bro, why did you choose IBM with S&P-500. Why the independent variables are S&P and why Dependent variable is IBM?? Btw, Wishes for keeping up.. (y)

so simple. thanks. mate !!!!!

hi, Codible why did you use adj close price not the close price?

Closing price is just the last price in trading day. so if stock split than you could find your stock half at closing and you would die if see your stock price got down from 20 to 10 but you won't find this prom in adjusted price. So it is more acceptable for traders.

you are the best love you

thanks for the video and good explanation...

Thank you so much for this

What's the basis to take companies for making comparison

Your chart needs to be colored, for example dots on the Y axis takes RED color and the Y axis BLUE to ease your explanation ! Thanks

Dude we love you❤️

and what is about the risk free return?

How come the return is negative? did you get the formula right?

thanks. great video

so i download s&p and its one of the company IBM one years or so record right? Hello Sir can you interpret one of the data i prepared... This is from my countries stock exchange.

Good One.

why subtract 1?

nice!

good !

should not the S&P 500 be your Y variable?

I don't think so, because it is the independent variable. IBM's growth is dependent on the growth of the market as a whole to an extent, so it is the dependent variable, y.

legend

10.56% correlation isn't strong enough

Rsquare value is 0.1 and this model sucks

hard :(