BDSL test: Testing for non-linear dependencies in time series (Excel)

Вставка

- Опубліковано 25 лип 2024

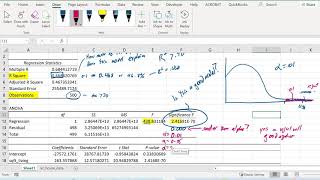

- Is there a model that would allow you to potentially predict a time series? What if it is a very complicated non-linear model? The Brock-Dechert-Scheinkman-LeBaron test (BDSL test; or BDS test) is designed just for that! It cleverly combines the insights from probability theory and graph theory to develop a rather simple procedure to test for any dependencies in your data. Today, we are applying this very test in Excel. Econometrics is easy with NEDL!

Please consider supporting NEDL on Patreon: / nedleducation

You can find the spreadsheets for this video and some additional materials here: drive.google.com/drive/folders/1sP40IW0p0w5IETCgo464uhDFfdyR6rh7

Please consider supporting NEDL on Patreon: www.patreon.com/NEDLeducation

Thank you sir 🙏

Please suggest on how to check nonlinear dependency in panel data

Hello thank you for this , tplease can you do a video on how to estimate BDS test on eviews ?

Thank you for the video! Do you think BDS test can be done this way with big samples of data?

Hi Niko, and thanks for the question! Conceptually, this is still the relevant procedure, however Excel is computationally very inefficient with large datasets as all the calculations are quadratic (so with 1,000 data points you will need 1,000,000 calculations, etc.)

Do you mind sharing the excel files of this and previous tuts? It will be time saving. Wonderful tut, keep going on!

Hi Rustu and glad you liked the video! Please check the Google Drive link in the pinned comment, the file should be there already :)

@@NEDLeducation Thanks!

Hey thanks so much for this video.

I still have one question regarding the optimal choice of epsilon. You mention that the optimal choice is 70 %, but I couldn't find that specific value in the original paper by Brock et al. Am I missing something, or is there another source for that value ?

Hi Tristan, and glad you liked the video! Excellent question, 70% stems from the idea that the test reaches maximum power when approximately half of pairs of pairs are within the distance and half are not, and if we assume independence, then (70%)^2 = 49% which is approximately a half.

Hey Savva, Just wanted to say thank you so much for this video and others like it. I recently completed my Masters thesis investigating information efficiency of cryptocurrency returns, and your videos were a huge help when it came to deciphering these tests! Best wishes from KCL!

Hi Alexander, and happy to hear my videos were helpful in your research!

Hi and thanks for your help, you’re amazing!! I wanted to ask what does non linear dependency mean?

Hi JaVale, and happy the videos helped! Non-linear dependence implies that there exists some non-linear model that has predictive power over future stock returns, without necessarily specifying what this model is. It is quite nicely related to the concept of deterministic chaos, if you are approaching it from the chaos theory perspective. Hope it helps!

@@NEDLeducation thank you, and what is meant by nonlinear and independent in this case as we are only looking at a single time series?

@@javalemcgee4723 Hi, independent here would mean time-independent, i.e., of previous realisations of the variable. Non-linear would mean that there can be a non-linear model that can predict future values of time series. For example, if a series is linearly independent, i.e., a model of form x(t) = a + b*x(t-1) has no explanatory power, a non-linear model of form, e.g., x(t) = a + b*x(t-1) + c*x^2(t-1) (not necessarily polynomial and not necessarily of lag one, any model that uses past variables) can have explanatory power, which would imply non-linear dependence. Hope it helps!

Hi Sava! I would like to ask you a question. What is the difference between BDS test (1996 in Econometrics, EViews Programme) and BDSL test? And the other question is that a small time series which has 25 years time series (t=25) can be applied this BDS test ? Thank you, have a nice day.

Hi Alim, and thanks for the question! As far as I know, there is no fundamental difference between the two, the test is the same, it is just the same concept that is being referred to from two different papers (one including LeBaron, hence "L").

Hi, I wanted to know where would I be able to find other datasets like this? Thanks.

Hi and thanks for the question! You can get many data series for financial markets free of charge from YahooFinance for example.

@@NEDLeducation Thank you for replying, I really appreciate it. I also wanted to know how You calculated the daily returns too if its not too much trouble. Thanks again.

The daily returns are calculated using the usual formula price today/price yesterday - 1.

Hi, what does it mean for the time series to be independent? Thank you.

Hi again, and thanks for the question! Independent series, broadly, are those that cannot be predicted from their past values.

By the way, the video on approximate entropy is here, check it out if you are interested: ua-cam.com/video/aDFs09eEiAU/v-deo.html

What do u think about my result ?

Percentile 70%

Epsilon 0.5936%

N 512

C1(pairs) 70%

K(triples) 54.03%

m=2 (pairs of pairs)

c2 (pairs of pairs) 51.81%

c12(pairs in trimmed sample) 69.95%

difference 2.88%

variance 0.010103043

stdev 0.44%

z-stat 6.4837

p-value 0.00%

m=3 (triple of pairs)

c3 (triple of pairs) 39.53%

c12(pairs in trimmed sample) 69.92%

difference -9.35%

variance 0.025260526

stdev 0.70%

z-stat -13.2898

p-value 0.00%

Hi, and thanks for sharing your results! This looks legit, seems there are significant non-linear dependencies in your data. Hope it helps!

@@NEDLeducation thanks for the fast response, any idea how to build prediction model based on that results?