✅ New to options trading? Master the essential options trading concepts with the FREE Options Trading for Beginners PDF and email course: geni.us/options-trading-pdf

This is just superb, I've been looking for "when should you exercise a call option?" for a while now, and I think this has helped. Ever heard of - Fiyarper Conspicuous Future - (do a search on google ) ? It is a smashing exclusive product for learning binary options trading signals minus the headache. Ive heard some unbelievable things about it and my work buddy got great results with it.

Hi, Thanks for the Video. Very knowledgeable. I have a question on the IV. @ 4:22 you have mentioned that, there would be "Larger expected movements" if IV is more. Does it mean that, the Option price will go up further? or it can be either upside or can be downside too?

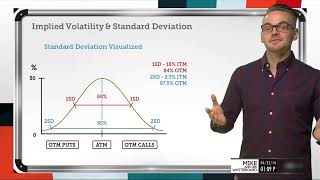

@@vijayk9457 The IV applies to both the upside and downside. If an option has an IV of 10%, there is a 68% chance the stock will be at either $90 or $110 over the period of the option. That accounts for 1 standard deviation.

@@johnfisher4910 First question, does the implied volatility change during the course of a contract? Second question, if that is the case is it safe to assume that hoping that implied volatility increases wether you’re long or short is what we’re look for? Third question, should we be looking for lower implied volatility hoping that it increases? Fourth question, where can we find the average implied volatility of a particular stock if there even is such a thing?

Chris, I just wanted to give you my compliments. This was incredibly well done. I'm a relatively new options trader, and I feel more connected to my trading when I take the time to truly dive into the concepts and the math. Thank you for creating this. I've watched it multiple times while taking notes.

This is brilliant! I don't generally comment on videos but this is exactly what I was looking for! Other videos did explain the concept but didn't explain how it can be used practically! Thank you!

AHHHH, this video is SOOOO AWESOME!!! This guy is the ONLY Trading Guru on the internet who isn't a Brokerage Pimp.. SO INFORMATIVE..AHHHHHHHH!!!! Buy this product!!!

Chris. I've watched loads of videos trying to explain what IV is to people new to options, but this is the best yet by far. If you haven't done statistics at high school don't worry, just remember these basic formulae and you're home and dry!

This video far exceeded my expectations, I was expecting just the implied volatility calculations and how to use it to your advantage, but we ended up getting more simple calculations that can put you ahead of others.

I've watched so many videos on IV and none of them make sense... I was actually able to wrap my head around this. Thanks for giving some practical examples of how to interpret it as well.

Awesome explanation - makes understanding IV very easy . Thanks a lot for this info . Even for a stock trader with limited Options experience or people wanting to switch to stock trading for a limited amount of time. A lower IV over a short period with a higher IV for a longer period will help assess if that stock is worth investing on for long term

Excellent video….the order in which you covered topics tracked perfectly with where my brain wanted to go next…..the questions that popped up in my head. Thanks!

Is there a roughly ideal IV for selling the wheel? In other words, the best balance of premium earned relative to the risk of a big move that might put the share price too far away from where I can sell the next call?

Great video! So ideally you’d want to buy long options with low IV before the IV explodes when the stock moves? What is confusing is that one would think that IV explodes when the stock moves to the downside, but it can happen both ways

How to take call options decisions based on the IV? Let's say stock X has 20% IV but stock Y has 50% IV with X and Y being $100 each. Which option to buy?

Awesome video and thanks for the information the only thing that bothers me is that there is only 252 days of trading. Do I still divide 30/365 for the monthly to get the monthly

Thanks for the comment! You can either use Trading Days / 252 or Calendar Days / 365. Both will give you virtually the same result. So, if you're using 30 calendar days then you'd use 365 as the denominator to get the monthly figure. -Chris

Thanks for this video but I'm still trying to use my calculator yo do the square root of the calendar days before expiration is that part divided by 365. I keep doing it and I get these numbers that's wwaayyy off. I got the stock price x implied volatility but it's the next part that puzzles me. Is it x ✓ time remaining÷ 365. Im not getting a solid answer like that. I'm using the calculator on my phone btw.

Implied volatility was very confusing concept for me....thanks to your videos I am able to understand it fairly.....you re doing a great job!! chris......Just one quuestion.....whey do different strike price has different IV....when the underlying is the same......

Hi Vinay, The IV I'd use is the overall IV you see listed for that particular options expiration cycle, which essentially calculates one IV number from the calls and puts in that expiration cycle. Typically, the brokerage software will have the IV listed on the expiration. Here's what it looks like on tastyworks: imgur.com/a/i79j2jq I would use the IV of the cycle closest to the target timeframe you're looking at. -Chris

Thanks for this great video. Still curious about one thing though. Where does square root come from when calculating price range for arbitrary time frames? I was thinking a root mean square situation or from the standard deviation formula. Thanks

Can you explain to me why my put options go up even when the stock goes up? Conversely my call options stay the same when my stock goes up. I understand it's related to time value of money/ how much time is left on the option but I still don't understand

hi, when you calculated the 30 days, you said there's a 68% probability that stock will go + or - 10.75, how did you come up with the 68%. sorry, just trying to get a clear understanding of high IV works. And should a lower IV be a better buy than a higher IV?

Joan, The 68% probability comes from one standard deviation around the stock price. In statistics, about 68% of outcomes fall within one standard deviation of the average. When it comes to options trading, the "average" we use is the current stock price. So, if the current one standard deviation move is ±10.70 from the stock price, then the market is pricing in an approximate 68% probability that the stock price will be within 10.70 of the current price in X number of days. In the example, the number of days was 30. Here's more on standard deviation: www.investopedia.com/terms/s/standarddeviation.asp Regarding buying options in low IV vs. high IV, it's relative, in my opinion. Low IV occurs when option prices get cheap. Option prices only get cheap if the market is expecting less volatile stock price movements. So, while you're buying cheaper options in low IV relative to high IV, you're buying options when the stock is barely moving. Conversely, when you buy options in high IV, you're paying more money because the stock price is fluctuating more and more on a daily basis (and that's why IV is high--option prices are expensive because traders will pay more for an option on a stock that moves around a lot more). So, buying options in low IV is better if you correctly time when the market will become more volatile. However, both plays require correct market timing to make money. Otherwise, the positions will lose money from decay.

Why wouldn't you use the 100 day simple moving average (SMA) of the underlying to make this calculation instead of current stock price? The std deviation is geared towards averages, and a stock price in time is NOT an average. GME is a great example albeit extreme. If the u/l is far off the 100 day SMA one way or the other, then the calculation should begin with the average of the price/100 day SMA. In my opinion.

when you apply this formula do you have to use the current stock price at what the security is trading at this very moment multiplied by the IV of the stock price option you're willing to buy, or is it the price of the stock you're speculating the security is going to reach multiplied by the IV

Maxine, I used the thinkBack feature on thinkorswim to find the estimated implied volatility. However, you can likely find the same information on your trading platform if you're able to plot implied volatility on one of the lower subplots. Please email me if you'd like to discuss this further: www.projectoption.com/contact-us -Chris

You deserve an A. bro. I am buying AMZN tomorrow Monday. I wonder if the price will move to 2000 in this 30 days due to big holidays's momentum? thanks. I am trying to understand IB Probability Lab . What % is consider high IV so big moves coming up? and which time frame? (one week, 30 days or other)

Hi Chris! A little clarification I heard you say this twice in your other videos: option prices drive implied volatility. I got a little confused. So I dug around a little and Is it not the other way around? Don't people pay more/less for an option if they feel the stock is more/less volatile?

I say that because you trade the option, which has a price. When buying/selling of an option occurs, the price changes. The option's price is what determines IV. A huge increase in option buying activity due to higher stock volatility will drive option prices higher, and therefore IV. We do not turn a dial on IV and make the option prices change.

@@projectfinance You are right! Moreover, implied volatility is actually calculated from the Black Scholes with the current option's price as input. I was conflating implied with historical volatility. This has always eluded me 👍🏿

Great article, but it doesn't explain how or why EXPR's IV is at 237% (High?) while the option price has fallen steadily for days and at two days until expiration the option is almost worthless. The stock has dropped by 7% in the past five days and opened this morning at its lowest in ten days

Hi, you are doing great.. your videos are so informative. Please clarify my doubt. How come you show only one IV for both call and put options for pepsi and UNP ? call and put, don't they have different IV ? thanks.

Hi there, That's a great question. For these examples, I used the aggregate IV from each stock just to illustrate the concept of higher/lower implied volatility. But, you're right. Each option has its own respective amount of price/extrinsic value (and therefore IV). Comparing OTM call and put IVs is a good way to assess skew in a particular product/stock. -Chris

Hi, by high and low implied volatility do you mean higher and lower implied volatility when compared to the historical implied volatility or the historical volatility of the underlying stock itself ? thanks

In this video, I did mean "higher" and "lower" as in relative to each level of IV. Of course, 10-25% IV in some stocks could be incredibly low overall. For this video, the two IV levels were compared relatively to illustrate the concept of higher/lower option prices and the stock's "expected range." -Chris

Sure! I've been planning to do a video on that topic. The short answer is that the two are related because if option/stock prices move out of line from put-call parity, then the buying/selling from arbitrage trades that present themselves will bring the prices back in line with put-call parity (thus eliminating arbitrage opportunities). -Chris

68% represents a range of "one standard deviation" around the mean/average. In the stock market, the "mean/average" is the current stock price. The one standard deviation stock price range is the implied range for a stock with about 68% likelihood. Here's an article that explains it nicely: www.optionsplaybook.com/options-introduction/what-is-volatility/

Square Root is effectively a number raised to the 1/2 or 0.5 power. So, you could do the following: $250 x .15 x (30/365)^(0.5) I'd recommend using WolframAlpha if you're doing the calculation with a PC calculator or online: www.wolframalpha.com/input/?i=250*.15*sqrt(30%2F365) I hope this helps!

What kind of calculator are you using? Depending on the calculator, you might already have a square root function on your calculator. The symbol is √ . To get SQRT(30/365), you'd likely have to first solve for 30/365. Once the result is on your screen, hit the √ button and that should give you the square root of 30/365. I hope this helps. If not, maybe this webpage could help: www.squarerootcalculator.co/. Let me know. -Chris

Hi Chris, In your video there is a part that mentioning on 2 standard deviation, on what circumstances that we needed to look into that? As the general was only 1 standard deviation. Also as I notice that you are using thinkorswim platform, the studies for predicting the future prices was it the ProbabilityofExpiringCone?

@@projectfinance I love your video. Its been so long since I did square root. Please help with this. I multipllied 250x.15=37.5 now I divided 30/365= its 12.16 or .08. I am not get 10 dollars. Can you show the math on the square root of 30/365, Thank you in advance.

Just a quick question of the stock price and figuring it out. Is the computation of a stock the (close price?) or (open price?) before being multiplied by the (IV) implied volatility?

How would you calculate the true implied 1 m volatility on the VIX ? Is there actually an implied vola on an implied vola on the S&P ? Thanks for answers in advance :D

Great question! Actually, there is a VIX of the VIX, it's called VVIX: www.cboe.com/products/vix-index-volatility/volatility-on-stock-indexes/the-cboe-vvix-index/vvix-whitepaper VVIX measures the implied volatility of the VIX Index, which means VVIX is the implied volatility of SPX implied volatility, as you've already mentioned! -Chris

Justin, That's correct. The overall IV of a stock represents the 1 standard deviation expected range for a stock over a given time period. However, keep in mind that all IV numbers are annualized. I hope this helps! -Chris

@@projectfinance Aren't they always annualized? If I see a 32 days to expiration IV at 46% for AAPL. Isn't 46% IV annualized? Or I have to calculate the annual IV? (46%*365/32)

Hi, not sure my question will get answered since this video is quite awhile ago, I will try luck anyway. Does that mean an option extrinsic value will not only decrease over time as the time value decay? If a highly volatile stock suddenly step into a period that it becomes less volatile, the option price will therefore jump significantly than a normal time decay ? Appreciate it!

Yes exactly. An option's price is a function of expected stock volatility in the future. "Expected" meaning from the market. And expected future volatility is tied to the historical or realized volatility of a stock (a high volatility stock is expected to stay high volatility and vice versa). If a highly volatility stock sees a big drop in its volatility, the option prices will account for that and likely become much cheaper due to the lower volatility of the stock (smaller stock price movements => cheaper option prices). It's a continuously adjusted process.

@@projectfinance thanks for prompt reply Chris. I guess that will be leading to a topic on when to select buying or selling an option. From your explanation, it doesn't sound like a good idea to open a long call option for any stock that suddenly raises up a lot in short period of time (e.g. PLTR or ACB recent trend) if one believe that short term momentum is hard to continue. Even the price will then be stablized at a high level, the call option price will still depreciate a lot during the stablized period, if I understood you correctly. Is there any video around this topic ? Many thanks!

Now I sat and did the calcs and put them on my spreadsheet, problem.. I can't have the linear figure it out ☢️. On the graph. ( but I can see it in my mind)

What about interest rate. Do you want to convey that interest rates have no role to play in calculation? Because if we reverse calculate IV using expected move, days to expiry does not assume any significant. As per your explanation: Exp Move = SP * IV% * Sqrt ( Days to expire / 365) Now there for IV = Exp Move / SP * Sqrt ( DTE /365) = IV

Interest rates do make a difference with option prices, but on a short time period, the difference is minuscule and outside the scope of this video. As an example, I plugged in some option pricing factors into a calculator and tested the difference in option prices with a 2.5% interest rate and a 5% interest rate: 2.5% Interest Rate: imgur.com/hGDH0nZ 5.0% Interest Rate: imgur.com/wjiwOrt As you mentioned, the interest rate does make a difference, but for the purposes of this video, I didn't feel it was a big enough factor to include because it would only complicate the topic even more. To my current understanding, interest rates are much more important to consider when discussing long-term options, say with more than a year to expiration.

@@projectfinance at India, ivs are calculated using interest rate of 10℅, in this case which will make difference. Further, check using formula derived from your video and change the day parameter you will get huge change in ivs value, but since it's corrsponigly acting, option prices are not changing... Does drop and increase in IV, with change in days with significant variation should be treated as miniscule, I doubt that. That too when IVs are calculated assuming interest rate @10℅?

Well thanks so much for commenting! I appreciate it. I made an updated version of this video with a nicer presentation and additional information, which can be viewed here: ua-cam.com/video/H-NHZq-skFo/v-deo.html I personally think the new video is much better. Many of the first examples are the same, but the newer video has additional lessons included in it.

The rule stating 68% of the data in the distribution is contained within +/- 1 standard deviation only applies if the underlying distribution is normal. Stock prices are anything but normal. While yes, it's possible for the underlying distribution of stock prices to be normal over a specific period, assuming that will hold true indefinitely is like assuming your 7/11 scratchie will be a winner every time--it simply wont happen. Having said that, it's still great to learn about normal distributions. Also, it would be apt to use 252 when annualizing volatility data, seeing as the markets don't operate on a 365-day calendar

Hi. Really appreciate your videos. Sorry for a stupid question but I want to calculate 2Sd range for 15 days. can you please comment an example? I understood till SP x IV x (sqrt of days/365). but where should i multiply 2 for 2Sd range for 15days as example? Would be really helpful. Thank you

Thank you, Rajesh! That is not a stupid question at all. For a 2 SD range over a 15-day period, the calculation would be: [Stock Price x IV x SQRT(15/365)] x 2 So, multiply the result from Stock Price x IV x SQRT(DTE/365) by 2 for a 2 SD move. Please let me know if you need more help. -Chris

Hi Chris. Below is a link option chain of BANKNIFTY Index in India. I tried calculating range of 23500 ATM with IV of 15.35 (16 days left to expiry) on the above formula. The output shows is 74938. I am not able to figure out how this works for Indian Markets. If you have free time, would appreciate your help. www.nseindia.com/live_market/dynaContent/live_watch/option_chain/optionKeys.jsp?symbolCode=-9999&symbol=BANKNIFTY&symbol=BANKNIFTY&instrument=-&date=-&segmentLink=17&symbolCount=2&segmentLink=17

Rajesh, The issue is that you're multiplying the stock price by 15.35 instead of .1535. Since implied volatility is a percentage you need to convert the implied volatility number to a percentage (divide by 100). So, the calculation would be: 23,500 x .1535 x SQRT(16/365) = ±$757 I hope this helps! -Chris

So basically because people are expecting a big move the price per option goes up? And if no moves are expected then the volume goes down which drives the option price down?

Moves are always expected (which scale relative to the time frame), but essentially, if a stock's options experience a broad decrease in prices, that's an indication that less volatility is expected from the stock in the future (therefore, lower implied volatility). The opposite is true when a stock's options experience a broad increase in prices relative to the time left until expiration.

How do I find implied volatility for individuals stocks or etfs..in the options sections in td ameritrade each option price has its own implied volatility ...

You can look at the IV on the expiration cycle. Specifically, a "stock's IV" is the implied volatility near the 30-day expiration cycle. Please see this image below to see the IV of various expiration cycles: imgur.com/D4NMS8a

I think the implied volatility in an option contract is annualised implied volatility and not volatility for DTE of the option contract. The derivation of BS model makes it clear that the volatility is annualised and time period is also expressed in terms of years. Infact, the final BS model states risk free rate as annualised rate and time also in terms of years.

You're correct. Implied volatility is always expressed as an annualized percentage. However, implied volatility measures the amount of extrinsic value in option contracts relative to the time they have until expiration (factoring in the strike price, of course). No matter the time to expiration left in the option, implied volatility is always presented as an annualized figure, but that doesn't mean a 30-day option can't be used to demonstrate what implied volatility represents (extrinsic value relative to the time to expiration).

✅ New to options trading? Master the essential options trading concepts with the FREE Options Trading for Beginners PDF and email course: geni.us/options-trading-pdf

This is just superb, I've been looking for "when should you exercise a call option?" for a while now, and I think this has helped. Ever heard of - Fiyarper Conspicuous Future - (do a search on google ) ? It is a smashing exclusive product for learning binary options trading signals minus the headache. Ive heard some unbelievable things about it and my work buddy got great results with it.

Hi, Thanks for the Video. Very knowledgeable. I have a question on the IV. @ 4:22 you have mentioned that, there would be "Larger expected movements" if IV is more. Does it mean that, the Option price will go up further? or it can be either upside or can be downside too?

@@vijayk9457 The IV applies to both the upside and downside. If an option has an IV of 10%, there is a 68% chance the stock will be at either $90 or $110 over the period of the option. That accounts for 1 standard deviation.

Lpm

@@johnfisher4910 First question, does the implied volatility change during the course of a contract?

Second question, if that is the case is it safe to assume that hoping that implied volatility increases wether you’re long or short is what we’re look for?

Third question, should we be looking for lower implied volatility hoping that it increases?

Fourth question, where can we find the average implied volatility of a particular stock if there even is such a thing?

Thank you for sharing this video, I've watched like 100 times over the course of a week and I finally get it!

Dude ... you're my spirit animal ...

Hats off to these guys for providing free education

This is by far the most complete yet straight to the point, simple and practical explanation among the many I have watched.

Chris, I just wanted to give you my compliments. This was incredibly well done. I'm a relatively new options trader, and I feel more connected to my trading when I take the time to truly dive into the concepts and the math. Thank you for creating this. I've watched it multiple times while taking notes.

Thank you! I appreciate you taking the time to leave an awesome comment.

-Chris

When you said “In the next 30 days, there’s a 68% probability…” where did you get 68% from? 10:42

One of the best video’s explaining the IV theory - a beautiful way to combine the math with reality trade impact.

This is brilliant! I don't generally comment on videos but this is exactly what I was looking for!

Other videos did explain the concept but didn't explain how it can be used practically! Thank you!

Well structured diagnosis of implied vol. Thank goodness for your analysis. Thank you

AHHHH, this video is SOOOO AWESOME!!! This guy is the ONLY Trading Guru on the internet who isn't a Brokerage Pimp.. SO INFORMATIVE..AHHHHHHHH!!!! Buy this product!!!

Chris. I've watched loads of videos trying to explain what IV is to people new to options, but this is the best yet by far. If you haven't done statistics at high school don't worry, just remember these basic formulae and you're home and dry!

Thank you Frank! I’m actually planning to redo this video with the new and improved editing :)

Best Option educational channel that I am following. Thank you so much for the great work!

Best video I have seen on IV. In fact all your videos are very good. You should teach. You have a knack for it.

Thank you! I appreciate your comment.

This is great. I added these formulas right into my excel spreadsheets so I can do a quick check of where the stocks might go.

This video far exceeded my expectations, I was expecting just the implied volatility calculations and how to use it to your advantage, but we ended up getting more simple calculations that can put you ahead of others.

I've watched so many videos on IV and none of them make sense... I was actually able to wrap my head around this. Thanks for giving some practical examples of how to interpret it as well.

thanks for explaining this in a simple but really clear way.

Thank you for this video. I can understand volatility well than reading by myself. Really appreciate it.

Thank you so much for a very simple and clear explanation on implied volatility and option price! ❤❤❤

Awesome explanation - makes understanding IV very easy . Thanks a lot for this info .

Even for a stock trader with limited Options experience or people wanting to switch to stock trading for a limited amount of time. A lower IV over a short period with a higher IV for a longer period will help assess if that stock is worth investing on for long term

You seriously are the greatest teacher! I appreciate all the work you put in

Thank you! I appreciate the comment.

-Chris

he's good at explaining things. i understood this better than a stat class i took

Thanks so much! I appreciate that. Thanks for watching/commenting.

Excellent video….the order in which you covered topics tracked perfectly with where my brain wanted to go next…..the questions that popped up in my head. Thanks!

Is there a roughly ideal IV for selling the wheel? In other words, the best balance of premium earned relative to the risk of a big move that might put the share price too far away from where I can sell the next call?

My compliments! Excellent (brilliant) explanation. Thank you.

Thank you! I appreciate the comment!

-Chris

Very crisp explanation. I like how the statistical explanation (ie. IV is 1 sigma) is made simple. Good job

Glad it was helpful!

Brilliant video! Great, clear, concise examples and explanations! Thank you

Such an excellent explanation. Easy to understand and comprehend. Great job.

Glad it was helpful!

Great video!

So ideally you’d want to buy long options with low IV before the IV explodes when the stock moves?

What is confusing is that one would think that IV explodes when the stock moves to the downside, but it can happen both ways

So if a stock has high IV meaning is going down? Or meaning stock will go any direction? that apply to every stock?👾

You are the man, Chris!💯💯💯

by far, best and clear video on internet

Ajinkya,

Thank you for the awesome comment! I'm glad you liked the video.

-Chris

Excellent presentation. Keep it up, so clear and well explained.

Very informative, exactly what I was looking for

Glad to hear it, Joel! Thanks for the comment.

-Chris

How to take call options decisions based on the IV? Let's say stock X has 20% IV but stock Y has 50% IV with X and Y being $100 each. Which option to buy?

When calculating the price range over the calendar days, do you use the STOCK price or the STRIKE price of a particular option?

Best explanation of IV ever seen. Anyone knows why 68% at 6:49 part?

Clear and concise explanation. I give the man an A+

Awesome video and thanks for the information the only thing that bothers me is that there is only 252 days of trading. Do I still divide 30/365 for the monthly to get the monthly

Thanks for the comment!

You can either use Trading Days / 252 or Calendar Days / 365. Both will give you virtually the same result.

So, if you're using 30 calendar days then you'd use 365 as the denominator to get the monthly figure.

-Chris

Good explanation! Just wondering why you use +/-1.68 for 1 standard deviation instead of +/- 1.65 as the z table shown? Thx

Project option your teaching is impeccable 👌

I appreciate it and thank you for commenting!

Thanks for this video but I'm still trying to use my calculator yo do the square root of the calendar days before expiration is that part divided by 365. I keep doing it and I get these numbers that's wwaayyy off. I got the stock price x implied volatility but it's the next part that puzzles me. Is it x ✓ time remaining÷ 365. Im not getting a solid answer like that. I'm using the calculator on my phone btw.

Implied volatility was very confusing concept for me....thanks to your videos I am able to understand it fairly.....you re doing a great job!! chris......Just one quuestion.....whey do different strike price has different IV....when the underlying is the same......

Super useful and clear, thanks for the lecture

What is the IV calculation with leaps that have more than 1 year on them?

So how does one use the range of the price to call or put options.

Very useful. Thanks a lot. Good luck to you 👍🙂

This video helped so much!!! Thank you

You're welcome! Thanks for watching!

Fantastic explanation. Better than every other video.

Thank you!

Thanks for the video however when you say to calculate for any time range then what side IV we have to take .. call or put

Hi Vinay,

The IV I'd use is the overall IV you see listed for that particular options expiration cycle, which essentially calculates one IV number from the calls and puts in that expiration cycle.

Typically, the brokerage software will have the IV listed on the expiration. Here's what it looks like on tastyworks:

imgur.com/a/i79j2jq

I would use the IV of the cycle closest to the target timeframe you're looking at.

-Chris

Okay. Great explanation, easily understood. So what do I do with that info?

Thanks for this great video. Still curious about one thing though. Where does square root come from when calculating price range for arbitrary time frames? I was thinking a root mean square situation or from the standard deviation formula. Thanks

you are an awesome teacher saw few of your videos and so easy to understand!!! Thanks a lot

Thank you for watching!

Very informative and understandable. Thank You

honestly you explained Iv in the easiest way

Excellent, thank you for the clear explanation!

Can you explain to me why my put options go up even when the stock goes up? Conversely my call options stay the same when my stock goes up. I understand it's related to time value of money/ how much time is left on the option but I still don't understand

Can I ask where did you get the 68% probability of Netflix moving between 54.60 and 140.40 ? At 5:52 I know some will beat me up for asking this

hi, when you calculated the 30 days, you said there's a 68% probability that stock will go + or - 10.75, how did you come up with the 68%. sorry, just trying to get a clear understanding of high IV works. And should a lower IV be a better buy than a higher IV?

Joan,

The 68% probability comes from one standard deviation around the stock price. In statistics, about 68% of outcomes fall within one standard deviation of the average. When it comes to options trading, the "average" we use is the current stock price.

So, if the current one standard deviation move is ±10.70 from the stock price, then the market is pricing in an approximate 68% probability that the stock price will be within 10.70 of the current price in X number of days. In the example, the number of days was 30. Here's more on standard deviation: www.investopedia.com/terms/s/standarddeviation.asp

Regarding buying options in low IV vs. high IV, it's relative, in my opinion.

Low IV occurs when option prices get cheap. Option prices only get cheap if the market is expecting less volatile stock price movements. So, while you're buying cheaper options in low IV relative to high IV, you're buying options when the stock is barely moving.

Conversely, when you buy options in high IV, you're paying more money because the stock price is fluctuating more and more on a daily basis (and that's why IV is high--option prices are expensive because traders will pay more for an option on a stock that moves around a lot more).

So, buying options in low IV is better if you correctly time when the market will become more volatile.

However, both plays require correct market timing to make money. Otherwise, the positions will lose money from decay.

Thank you!!! Where is a good place to find a stock's implied volatility?

Your trading platform will provide it. Some platforms let you plot historical IV readings.

Is IV system useful for Intraday and equity delivery purpose ??

Why wouldn't you use the 100 day simple moving average (SMA) of the underlying to make this calculation instead of current stock price? The std deviation is geared towards averages, and a stock price in time is NOT an average. GME is a great example albeit extreme. If the u/l is far off the 100 day SMA one way or the other, then the calculation should begin with the average of the price/100 day SMA. In my opinion.

when you apply this formula do you have to use the current stock price at what the security is trading at this very moment multiplied by the IV of the stock price option you're willing to buy, or is it the price of the stock you're speculating the security is going to reach multiplied by the IV

Stanley,

When using the formula you should use the current stock price multiplied by the current implied volatility.

thank u for a prompt reply, I subbed :)

Where did you find the IV on NFLX? If you pulled up the stock on 092816, where does it show the IV @ 44% on the stock chart?

Maxine, I used the thinkBack feature on thinkorswim to find the estimated implied volatility. However, you can likely find the same information on your trading platform if you're able to plot implied volatility on one of the lower subplots.

Please email me if you'd like to discuss this further: www.projectoption.com/contact-us

-Chris

You deserve an A. bro. I am buying AMZN tomorrow Monday. I wonder if the price will move to 2000 in this 30 days due to big holidays's momentum? thanks. I am trying to understand IB Probability Lab . What % is consider high IV so big moves coming up? and which time frame? (one week, 30 days or other)

Hi Chris!

A little clarification

I heard you say this twice in your other videos: option prices drive implied volatility.

I got a little confused. So I dug around a little and

Is it not the other way around? Don't people pay more/less for an option if they feel the stock is more/less volatile?

I say that because you trade the option, which has a price. When buying/selling of an option occurs, the price changes. The option's price is what determines IV.

A huge increase in option buying activity due to higher stock volatility will drive option prices higher, and therefore IV. We do not turn a dial on IV and make the option prices change.

@@projectfinance You are right!

Moreover, implied volatility is actually calculated from the Black Scholes with the current option's price as input.

I was conflating implied with historical volatility. This has always eluded me 👍🏿

Great article, but it doesn't explain how or why EXPR's IV is at 237% (High?) while the option price has fallen steadily for days and at two days until expiration the option is almost worthless. The stock has dropped by 7% in the past five days and opened this morning at its lowest in ten days

Hi, you are doing great.. your videos are so informative. Please clarify my doubt. How come you show only one IV for both call and put options for pepsi and UNP ? call and put, don't they have different IV ? thanks.

Hi there,

That's a great question.

For these examples, I used the aggregate IV from each stock just to illustrate the concept of higher/lower implied volatility. But, you're right. Each option has its own respective amount of price/extrinsic value (and therefore IV).

Comparing OTM call and put IVs is a good way to assess skew in a particular product/stock.

-Chris

thank you sir for simple analysis

If the VIX goes up, does the implied volatility of a stock always go up as well?

thanks for explaining clearly much appreciated ,mate

Fantastic video. What a guy

Finally I get it how to look at IV. Big thanks for that!

Hi, by high and low implied volatility do you mean higher and lower implied volatility when compared to the historical implied volatility or the historical volatility of the underlying stock itself ? thanks

In this video, I did mean "higher" and "lower" as in relative to each level of IV.

Of course, 10-25% IV in some stocks could be incredibly low overall.

For this video, the two IV levels were compared relatively to illustrate the concept of higher/lower option prices and the stock's "expected range."

-Chris

Thanks a lot for patiently replying my questions. Can you please make a video on option arbitrage and how it is different from put call parity..

Sure!

I've been planning to do a video on that topic.

The short answer is that the two are related because if option/stock prices move out of line from put-call parity, then the buying/selling from arbitrage trades that present themselves will bring the prices back in line with put-call parity (thus eliminating arbitrage opportunities).

-Chris

Great explanation! I wish I could go back to the days where Netflix was 98 dollars! I would buy so many options expiring in 2020!

@@lucasbenjamin4991 do you think im dumb you pos scammer

Thiss is Gold!! Thank you so much

This video really helps your odds. Thanks!!!!!!

I'm glad you liked the video! Thanks for the comment!

-Chris

Thank you for the excellent vedio, just one question, why the implied vol represent the 68% probability range of stock price movement?

68% represents a range of "one standard deviation" around the mean/average. In the stock market, the "mean/average" is the current stock price. The one standard deviation stock price range is the implied range for a stock with about 68% likelihood. Here's an article that explains it nicely: www.optionsplaybook.com/options-introduction/what-is-volatility/

Why do we assume 68% for 1 standard deviation and 95% for 2 standard deviation?

So so so helpful, thank you very much!

How do you calculate sq root? As your video shown $250x15%x 30/365. How to calculate the square root

Square Root is effectively a number raised to the 1/2 or 0.5 power.

So, you could do the following:

$250 x .15 x (30/365)^(0.5)

I'd recommend using WolframAlpha if you're doing the calculation with a PC calculator or online:

www.wolframalpha.com/input/?i=250*.15*sqrt(30%2F365)

I hope this helps!

projectoption it helps a lot on the website. However, the final part

^ 0.5, how do I do it on calculator 🤔

What kind of calculator are you using? Depending on the calculator, you might already have a square root function on your calculator. The symbol is √ .

To get SQRT(30/365), you'd likely have to first solve for 30/365. Once the result is on your screen, hit the √ button and that should give you the square root of 30/365.

I hope this helps. If not, maybe this webpage could help: www.squarerootcalculator.co/.

Let me know.

-Chris

Hi Chris, In your video there is a part that mentioning on 2 standard deviation, on what circumstances that we needed to look into that? As the general was only 1 standard deviation.

Also as I notice that you are using thinkorswim platform, the studies for predicting the future prices was it the ProbabilityofExpiringCone?

@@projectfinance I love your video. Its been so long since I did square root. Please help with this. I multipllied 250x.15=37.5 now I divided 30/365= its 12.16 or .08. I am not get 10 dollars. Can you show the math on the square root of 30/365, Thank you in advance.

Just a quick question of the stock price and figuring it out. Is the computation of a stock the (close price?) or (open price?) before being multiplied by the (IV) implied volatility?

You use the current stock price when doing implied volatility/expected move calculations.

How would you calculate the true implied 1 m volatility on the VIX ? Is there actually an implied vola on an implied vola on the S&P ? Thanks for answers in advance :D

Great question! Actually, there is a VIX of the VIX, it's called VVIX:

www.cboe.com/products/vix-index-volatility/volatility-on-stock-indexes/the-cboe-vvix-index/vvix-whitepaper

VVIX measures the implied volatility of the VIX Index, which means VVIX is the implied volatility of SPX implied volatility, as you've already mentioned!

-Chris

IV is always based on one standard deviation? Hence 68% probability?

Justin,

That's correct.

The overall IV of a stock represents the 1 standard deviation expected range for a stock over a given time period. However, keep in mind that all IV numbers are annualized.

I hope this helps!

-Chris

@@projectfinance Aren't they always annualized? If I see a 32 days to expiration IV at 46% for AAPL. Isn't 46% IV annualized? Or I have to calculate the annual IV? (46%*365/32)

Which implied volatility do you use IV or IV percentile, or IV rank? Great video thanks a lot!

Hi, not sure my question will get answered since this video is quite awhile ago, I will try luck anyway.

Does that mean an option extrinsic value will not only decrease over time as the time value decay? If a highly volatile stock suddenly step into a period that it becomes less volatile, the option price will therefore jump significantly than a normal time decay ?

Appreciate it!

Yes exactly. An option's price is a function of expected stock volatility in the future. "Expected" meaning from the market. And expected future volatility is tied to the historical or realized volatility of a stock (a high volatility stock is expected to stay high volatility and vice versa).

If a highly volatility stock sees a big drop in its volatility, the option prices will account for that and likely become much cheaper due to the lower volatility of the stock (smaller stock price movements => cheaper option prices). It's a continuously adjusted process.

@@projectfinance thanks for prompt reply Chris. I guess that will be leading to a topic on when to select buying or selling an option. From your explanation, it doesn't sound like a good idea to open a long call option for any stock that suddenly raises up a lot in short period of time (e.g. PLTR or ACB recent trend) if one believe that short term momentum is hard to continue. Even the price will then be stablized at a high level, the call option price will still depreciate a lot during the stablized period, if I understood you correctly.

Is there any video around this topic ? Many thanks!

Victor Yeung where are you from?

Now I sat and did the calcs and put them on my spreadsheet, problem.. I can't have the linear figure it out ☢️. On the graph. ( but I can see it in my mind)

What about interest rate. Do you want to convey that interest rates have no role to play in calculation? Because if we reverse calculate IV using expected move, days to expiry does not assume any significant.

As per your explanation:

Exp Move = SP * IV% * Sqrt ( Days to expire / 365)

Now there for IV =

Exp Move / SP * Sqrt ( DTE /365) = IV

Interest rates do make a difference with option prices, but on a short time period, the difference is minuscule and outside the scope of this video.

As an example, I plugged in some option pricing factors into a calculator and tested the difference in option prices with a 2.5% interest rate and a 5% interest rate:

2.5% Interest Rate: imgur.com/hGDH0nZ

5.0% Interest Rate: imgur.com/wjiwOrt

As you mentioned, the interest rate does make a difference, but for the purposes of this video, I didn't feel it was a big enough factor to include because it would only complicate the topic even more.

To my current understanding, interest rates are much more important to consider when discussing long-term options, say with more than a year to expiration.

@@projectfinance at India, ivs are calculated using interest rate of 10℅, in this case which will make difference.

Further, check using formula derived from your video and change the day parameter you will get huge change in ivs value, but since it's corrsponigly acting, option prices are not changing... Does drop and increase in IV, with change in days with significant variation should be treated as miniscule, I doubt that. That too when IVs are calculated assuming interest rate @10℅?

You are an awesome teacher, really

Thank you!

never comment, but this video is awesome

Well thanks so much for commenting! I appreciate it. I made an updated version of this video with a nicer presentation and additional information, which can be viewed here: ua-cam.com/video/H-NHZq-skFo/v-deo.html

I personally think the new video is much better. Many of the first examples are the same, but the newer video has additional lessons included in it.

The rule stating 68% of the data in the distribution is contained within +/- 1 standard deviation only applies if the underlying distribution is normal. Stock prices are anything but normal. While yes, it's possible for the underlying distribution of stock prices to be normal over a specific period, assuming that will hold true indefinitely is like assuming your 7/11 scratchie will be a winner every time--it simply wont happen. Having said that, it's still great to learn about normal distributions.

Also, it would be apt to use 252 when annualizing volatility data, seeing as the markets don't operate on a 365-day calendar

So basically my AMC calls today were going up in premium when the stock price was going down because, people were willing to pay more for them?

Hi. Really appreciate your videos. Sorry for a stupid question but I want to calculate 2Sd range for 15 days. can you please comment an example?

I understood till SP x IV x (sqrt of days/365). but where should i multiply 2 for 2Sd range for 15days as example? Would be really helpful. Thank you

Thank you, Rajesh!

That is not a stupid question at all.

For a 2 SD range over a 15-day period, the calculation would be: [Stock Price x IV x SQRT(15/365)] x 2

So, multiply the result from Stock Price x IV x SQRT(DTE/365) by 2 for a 2 SD move.

Please let me know if you need more help.

-Chris

projectoption Thank you so much Chris. Really appreciate it 💗🙆

You're welcome! Anytime!

Hi Chris. Below is a link option chain of BANKNIFTY Index in India. I tried calculating range of 23500 ATM with IV of 15.35 (16 days left to expiry) on the above formula. The output shows is 74938. I am not able to figure out how this works for Indian Markets. If you have free time, would appreciate your help.

www.nseindia.com/live_market/dynaContent/live_watch/option_chain/optionKeys.jsp?symbolCode=-9999&symbol=BANKNIFTY&symbol=BANKNIFTY&instrument=-&date=-&segmentLink=17&symbolCount=2&segmentLink=17

Rajesh,

The issue is that you're multiplying the stock price by 15.35 instead of .1535. Since implied volatility is a percentage you need to convert the implied volatility number to a percentage (divide by 100).

So, the calculation would be: 23,500 x .1535 x SQRT(16/365) = ±$757

I hope this helps!

-Chris

So basically because people are expecting a big move the price per option goes up? And if no moves are expected then the volume goes down which drives the option price down?

Moves are always expected (which scale relative to the time frame), but essentially, if a stock's options experience a broad decrease in prices, that's an indication that less volatility is expected from the stock in the future (therefore, lower implied volatility). The opposite is true when a stock's options experience a broad increase in prices relative to the time left until expiration.

Thanks a lot...!

Very greatful for all the videos and your efforts...!

How do I find implied volatility for individuals stocks or etfs..in the options sections in td ameritrade each option price has its own implied volatility ...

You can look at the IV on the expiration cycle. Specifically, a "stock's IV" is the implied volatility near the 30-day expiration cycle. Please see this image below to see the IV of various expiration cycles:

imgur.com/D4NMS8a

Great info this will bhelp me in option trade another tool in my tool box

I think the implied volatility in an option contract is annualised implied volatility and not volatility for DTE of the option contract. The derivation of BS model makes it clear that the volatility is annualised and time period is also expressed in terms of years. Infact, the final BS model states risk free rate as annualised rate and time also in terms of years.

You're correct. Implied volatility is always expressed as an annualized percentage. However, implied volatility measures the amount of extrinsic value in option contracts relative to the time they have until expiration (factoring in the strike price, of course).

No matter the time to expiration left in the option, implied volatility is always presented as an annualized figure, but that doesn't mean a 30-day option can't be used to demonstrate what implied volatility represents (extrinsic value relative to the time to expiration).

Will you make a video on IV crush ?

Yes, I can do that!

How do you find? IV? Guessing you can google it for most stocks?

Outstanding!