Hello Thank you for the video. what if ARDL bound test expressed where short-run coefficients and long run coefficients are used together in one equation. t-1 included. How to run it?

Hello. Thank you for your video. I have a question about the max lags. The optimal lags of my each variable is 1 1 1 1 3 4, is it right to use maxlags(2)?

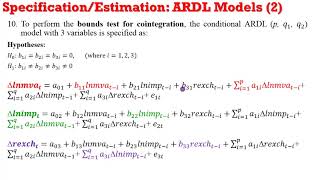

Hi thank for the explanation. I have comment on the bound test of cointegration. That is please try to listen the test part of the tutor. You do not talk about the higher bound and the decision is not right. Because the F test is higher that the upper bound at 5% critical value. Thank you

dv is stationary at first difference and some of Independent vs are stationary at level , long panel data , so is this video will help me to do cointegration test ?

Hi Naomi, Thank you very much for your explanation. However, I am looking for the following video about short term and ec, but I could not find it? could you share me where is the link? thanks

Thank you @derickpyro4137. Transforming data to log form helps standardize the units of measurement since you may have different variables having different units of measurement

You explained very well the decision criteria. However you did not interpret the results well. From the results F statistic is > that I(1) so we reject Ho except for 1% and conclude cointegration. F statist is also > than I(0) we therefore reject Ho and conclude cointegration

@@excellingwithnaomi I appreciate your efforts in putting useful vidoes out and thank you for confirming there is cointegration in the bound test result

Hi jayshreeacharaz9023 . are you asking how you decide on the max lags to use for your variables? The command for determining the maxlags for each variable is the same for the model that is varsoc variablename. If you find the maxlag for your variable is 2, then add the option maxlag(2) when running your ARDL model. e.g ardl dependentvariable independnetvariable1 independentvariable2, maxlags(2)

@@excellingwithnaomi Hi Naomi, first of all thank you for this informative video. Much appreciate. Regarding the maxlags , if i have 4 independent variables in my study so my maxlags will be maxlags(4). Am i right?

thank you so much, you saved my life !

Thanks from Bangladesh

Hello Thank you for the video. what if ARDL bound test expressed where short-run coefficients and long run coefficients are used together in one equation. t-1 included. How to run it?

Great suggestion! I will be coming up with this tutorial

Hello. Thank you for your video. I have a question about the max lags. The optimal lags of my each variable is 1 1 1 1 3 4, is it right to use maxlags(2)?

thanks from indonesia!

why u select max lag (2), is there any reason , the optimum lag u get is 1 from the lag selection

Hi thank for the explanation. I have comment on the bound test of cointegration. That is please try to listen the test part of the tutor. You do not talk about the higher bound and the decision is not right. Because the F test is higher that the upper bound at 5% critical value.

Thank you

I will check it out. Thanks

Realized the same too,

Thank you very mutch

You are welcome

dv is stationary at first difference and some of Independent vs are stationary at level , long panel data , so is this video will help me to do cointegration test ?

The bounds test is only applicable for time series. Instead you can perform other tests such as Westerlund, Kao and Pedroni

Hi Naomi, Thank you very much for your explanation. However, I am looking for the following video about short term and ec, but I could not find it? could you share me where is the link? thanks

Hi @t4859. Thanks for your comment. The video for short run and ec is coming soon

Thanks for the tutorial it's really helpful. But i'd is it necessary to transform the data into log form before performing the ARDL model?

Thank you @derickpyro4137. Transforming data to log form helps standardize the units of measurement since you may have different variables having different units of measurement

Log transformation is also used to address skewness problem

You explained very well the decision criteria. However you did not interpret the results well. From the results F statistic is > that I(1) so we reject Ho except for 1% and conclude cointegration. F statist is also > than I(0) we therefore reject Ho and conclude cointegration

correct. It might have been a slip of tongue. There is in fact cointegration

@alexgitau4499. sorry for that error.

@@excellingwithnaomi I appreciate your efforts in putting useful vidoes out and thank you for confirming there is cointegration in the bound test result

I have a question how to we decide on the maxlags(2)

Thank you

Hi jayshreeacharaz9023 . are you asking how you decide on the max lags to use for your variables? The command for determining the maxlags for each variable is the same for the model that is varsoc variablename. If you find the maxlag for your variable is 2, then add the option maxlag(2) when running your ARDL model. e.g ardl dependentvariable independnetvariable1 independentvariable2, maxlags(2)

@excellingwithnaomi maxlag for each variable and I choose the one with the highest?

@@jayshreeacharaz9023 yes

@excellingwithnaomi Thank you

@@excellingwithnaomi Hi Naomi, first of all thank you for this informative video. Much appreciate. Regarding the maxlags , if i have 4 independent variables in my study so my maxlags will be maxlags(4). Am i right?