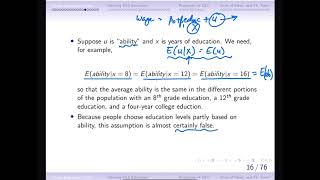

Zero conditional mean of errors - Gauss-Markov assumption

Вставка

- Опубліковано 2 чер 2013

- This video provides some insight into the 'zero conditional mean of errors' Gauss-Markov assumption. Check out ben-lambert.com/econometrics-... for course materials, and information regarding updates on each of the courses. Quite excitingly (for me at least), I am about to publish a whole series of new videos on Bayesian statistics on youtube. See here for information: ben-lambert.com/bayesian/ Accompanying this series, there will be a book: www.amazon.co.uk/gp/product/1...

- Навчання та стиль

Really good supplementary material for my Econometrics class, Thank you!

You are the hero of the year, thanks Ben! for all the videos!

Many thanks mate!!!!

Super helpful! This basically means that whatever is in the error term is uncorrelated with the x variable(s), which is why this may not ever be true in social science research as there may be some overlap that we just don't know yet.

thank you for this explanation lol

@@josh.c36 be careful! zero conditional mean rules out non-linear relationships as well and it a stronger assumption that uncorrelatedness

Thank you so much!!!!! super helpful and will let me pass my course

Hi can you explain why you use ui given xi I don't understand the intuition behind that?

Cool !!!

But we are assuming least squares so doesn't the line of best fit always lie right between the observations thus having a zero conditional mean? I don't quite understand

That would be the line of best fit if you plot y against x, but in this case we're plotting u against x.

@@Donutscanfly Thanks, I passed my statistics class :). Thanks for the help.

Please I don't really understand the concept behind zero mean

Why does E[u|x]=0 then cov[u,x]=0?

Using discrete case, (continuous is the same), say E[u] = 0. For E[u|x], this can be expressed as: E[u|x] = sum(u * Pu|x(u)), so if x and u are independent, the term Pu|x(u) can be expressed (from conditional probability formula) as the joint PMF of u and x divided by P of x: Pu|x(u) = Pu,x(u,x) / Px(x), and as we said they are independent, the Pu,x(u,x) = Pu(u)*Px(x), so, Pu|x(u) = Pu(u)Px(x)/ Px(x) = Pu(u), so E[u|x] = sum(u*Pu(u)) = E[u]. Since we already said that E[u] = 0, so E[u|x] = E[u] = 0 QED. Second, cov[u, x] can be expressed as: E[(u-Mu_u)(x-Mu_x)], where Mu is the mean (average/expected) value. Expanding this formula, we can get: E[ux - u*Mu_x - Mu_u*x + Mu_u*Mu_x], since any Mu is a constant, the expected value of a constant is a constant, then it can be written as: E[ux] - E[u]E[x], so this is the expression of covariance. When u and x is the same, this is the formula of variance of u, var[u,x] when u=x is: E[u^2] - E[u]^2. Back to the topic, since u and x are uncorrelated, which means they are independent, then E[ux] = E[u]E[x], this is a property you can verify. Then cov(u,x) = E[ux] - E[u]E[x] = E[u]E[x] - E[u]E[x] = 0. QED

Knowing the value of x doesn't change what you expect from u. So they are independent and don t vary together, witch is quantified by a 0 covariance

given

E(u|x)=0, there is no need for a further assumption of independence to demonstrate no correlation, Cov(u,x)=0

---------------------

E(u*x) = E(E(u*x|x)) ........... The outer parenthesis designate expectation along X

............ in case X is a random variable (which it is not :-).

E(E(u*x|x)) = E(x*E(u|x)) ........... since X is held constant in the inner conditional

............ expectation

E(x*E(u|x)) = E(x*0)=0 .............. using the given Gauss-Markov assumption, E(u|x)=0

So,

Cov(u,x) = E(u*x) - E(u)*E(x) = E(u*x) - E(E(u|x))*E(x) = 0 - 0 * E(x) = 0

@@kottelkannim4919 great explanation thanks

@@nadekang8198 THIS IS THE BEST EXPLANATION I'VE EVER SEEN IN MY LIFE. BETTER THAN ALL THE CLASSES I'VE HAD THIS SEMESTER. THANK YOU SO MUCH!!!!

don't understand one thing not even to save a life I wouldn't understand a thing here

You must be related to my professor. 0 to 60 in under 4 seconds. You left me behind : /