Ten signs a company's in trouble - MoneyWeek Investment Tutorials

Вставка

- Опубліковано 27 лип 2011

- Like this MoneyWeek Video? Want to find out more on companies in trouble?

Go to www.moneyweekvideos.com/ten-si...

now and you'll get free bonus material on this topic, plus a whole host of other videos.

Search our whole archive of useful MoneyWeek Videos, including:

· The six numbers every investor should know...

www.moneyweekvideos.com/six-nu...

· What is GDP?

www.moneyweekvideos.com/what-i...

· Why does Starbucks pay so little tax?

www.moneyweekvideos.com/why-do...

· How capital gains tax works...

www.moneyweekvideos.com/how-ca...

· What is money laundering?

www.moneyweekvideos.com/what-i...

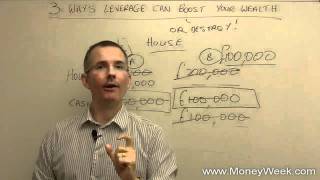

1. Goodwill

2. Current Ratio

3. Gearing

4. Off Balance Sheet

5. Plunging Cash Flow

6. Adjusted EBITDA

7. Key Management Changes

8. Directors Dumping Shares

9. One Customer

10. Rapid Expansion

I cant still believe this information is free! Awesome videos

This is a great video. Before watching this video I always thought that the cash flow statement was the most important financial report but now I see why the balance sheet has more valuable information. It is important to calculate the current ratio to find out if a business can pay off its current liabilities immediately and the debt to equity ratio to find out if it is over leveraged.

thanks for sharing the knowledge . you make it look so simple. i am big fan of your videos !

Thank you Tim, brilliant explanations

PLEASE share MORE RED SIGNS/SIGNALS of a comp drowning? Thanks Tim!

Great video Mr. Bennett however, I would've loved it if you used these numbers to predict a future bankruptcy of sorts instead saying that you knew this all along with Southern Cross.

Great video, Tim. Thank you, so much for this!!

Your videos are great thank you so much for providing us this info

You are great! Thank you very much!

Brilliant, awesome. Can not stop watching. Thank you so much.

I would think that the Cash Flow Statement (CFS) is the most important financial statement to analyse because it shows activities across the whole financial year whereas the Balance Sheet is a snapshot of just one day. I agree that profit and loss statements are not as important as the other two but I do think the CFS should be the first statement one looks at.

In this particular example (based solely on this video), if you look at the INVESTING ACTIVITIES in the CFS, you will discover the various acquisitions made and how it was financed - Cash Flow from Operations (CFO) or Cash Flow from Financing (CFF). Since you said the acquisitions were made with cheap money, we would see an increase in CFF therefore an increase in gearing (the leverage would be determined by examining the balance sheet) and interest payments. Under CFO, we would be able to see the changes in working capital which lead to a current ratio of 0.5.

Moreover, you can compare the CFO with Sales for a better measure.

Thoughts?

Excellent - still today in 2019

Hi Tim, your videos are awesome. Just wondering, are there any books in the market for stock investing that you would recommend? I would like to get a comprehensive guide. Of course if you think you can do a series of comprehensive videos on how to chose and value stocks that would be a lot better! Keep up the good job!

Thank you very much for this and other videos!

?? Where is it possible to find those souhern cross data??

thank you... it was very informational

Thank you so much Mr.Tim.I can't believe that you give us all this information on the house

NICE ADVICE, THANKS

Great info.

These are the best, thank you so much

Excellent, just excellent, please make more

"read accounts backwards" a good lesson on it's own.

This is an interesting video. I am using accounting ratios to analyse some current companies at the moment. A lot seem to have current ratios of slightly below 1:1 and gearing of around 70-75%. GSK and Coca Cola are two that I have looked at recently that fall into this category.

This guy either is from devon and/or is matt bellamy's father... I'm convinced :)

Excellent video. Congratulations.

Thanks for this

Excellent content, clear as cristal. Thanks

An excellent video. Thank you for this.

Your videos are gold.

He is able to go deep into the material while keeping cyou engaged. The perfect blend of style and substance.

Or the D/E combined with the artificially high value of equity due to the over inflated intangible asset. That's a 'robbing Peter to pay Paul' scenario.

Hi, how should the “listing market” ,, maybe London stock exchange has reacted to these signs ? What should they have done ?

Great Vid. Wished I had watched it before buying Aurora.

I love this guy 👍 intelligence and humor

Thank you so much for explaining in detail, very helpful in understanding. I am a mature (age 35 going on 36) BSc Accounting and Finance student.

Good luck!

@@xaviersharma707 Thank you for the encouraging words.

This is enormous gift to just be given at cost of few KBs of data.. thank you Ben for your generosity!!

love this guy! Especially his wit and ability to try break a complexity to layman terms - a genius. Who is he ?

Awesome!

great video

good intel. need to apply it to late 2020 companies.

Good video

Thank you Money Week

Bennett please would you help understand why a company can have straight (signifigant) book losses when it was set up to be a healthy business by the time it is transferred to Government in about 7 years......

I'm very intrigue of your 10 points etc

Appreciate your time and help

Thank you

What then is the optimal level of debt-to-equity ratio?

Hello, absolutely LOVE your videos, thankyou so much for sharing them.

I see your number 1 red flag is goodwill, I wonder what would be considered an acceptable good will amount. I.e. 10% shareholder equity, 20% etc...

Obviously in this vide you say 2x shareholder equity is bad so where is the line roughly?

Thankyou! :)

"By the time you get to note 34 most people have lost the will to live." Lol

lmao

Every accounting and finance student should watch this video.

14:47 So true!!

As American, I am not familiar with the balance sheet term 'good will'. Does it translate from GB to USA in any way? Is it like tax credits?

Say a company has a building worth $80,000 on their balance sheet. Ludivico Ltd. buys the building for $100,000. On Ludivico's balance sheet, $80,000 would be added to Property Plant & Equipment (PP&E), and $20,000 is added to goodwill.

Say Ludivico Ltd. bought the building for $120,000. Then goodwill would increase by $40,000.

Basically, if you overpay for an asset then goodwill increases more. Which is a bad sign.

It's called Goodwill in the US, too. For Example, Hain Celestial currently carries a Goodwill total over a billion, greater than 50% of their total market cap. Not as bad as the Southern Cross example, but bad enough to make me not buy.

Brilliant

:-) ... THIS GENTLEMAN's SARCASTIC UPPER-CUT (punch like) humor - swiftly SMACKS Jeremy Clarkson's humor out of the water/park.

How is no one else not saying this guy is 100% Christian Bale playing British Michael Burry.

He flips us off at 3:52 :(

Keith Cheok he's clearly British and they use two fingers. Seems like a nervous reaction subconscious. Still bad form in public speaking.

LMAO

Number 7: Uber nowadays. Be aware.

Non-profit all the way

The "one customer" thing, big problem.

Adjusted EBITDA is similar to the nonsense community EBITDA that Wework was espousing

So is Gearing a debt to shareholder equity ratio?

More or less. It is like having credit card debt compared to how much equity/personal income you have. The more the gearing, in this case, the more the credit card debt you have compared to your income/equity, the higher the risk you won't be able to pay off your credit card debt. Companies always look for an optimal level of gearing but I would want to say "optimal" is dependent on the Directors. The same way your optimal level of debt could be different to your friend's optimal level of debt.

Great content, just a big long winded. It would be nice if he kept it brief.

Good stuff but basic accounting stuff.

I've noticed the same about EBITDA, because, I give a damn shit about depreciation and amortization, I want earnings, no matter what. And they love to show EBITDA, why would they?

rimless glasses was a fashion, clean open face look ... how times have changed

i would so go to class if you where my professor to learn an more some haha yum eye candy

Wework? Except Wework couldn't go public .

At first i though he said savile cross

I would've just looked at the FREE CASH FLOW and taken it as a red alarm.

obviously your using hindsight, but your still wrong as you said people were buying/selling

regardless of the red flags so someone made some money plus that is what happens if you buy stock for the long term which i think you suggest?

you don't understand Tim's video, investing is not for you I'm afraid

Starts at 5:33

I cannot stand people talking without substance. Thanks for the videos. But more signal, less noise.

You could have been less rude, you know

please get to the point quickly.

you have really good videos. :-)

And then there was Covid...

Hihi, have you seen this program called the Intellitus Cash System? (google it). My mother says it gets people tons of income.

Far to much talking and not enough action. Get to the point mate we dont have all day

NICE ADVICE, THANKS