Monte Carlo Simulation of Temperature for Weather Derivative Pricing

Вставка

- Опубліковано 2 чер 2024

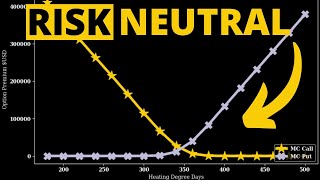

- In this online tutorial series dedicated to weather derivatives we have estimated the parameters of our modified mean-reverting Ornstein-Uhlenbeck process which defines our Temperature dynamics, and have now implemented different models for our time varying volatility. Now we move on to simulating temperature paths using Monte Carlo simulation method under the physical probability measure.

Once we have completed these simulation functions we can move onto implementing the Monte Carlo method under the risk-neutral pricing methodology for valuation of our temperature options.

Online written tutorial: quantpy.com.au/weather-deriva...

In this series we take a deep dive into a type of exotic financial products weather derivatives. Weather derivatives are financial instruments that can be used to reduce risk associated with adverse weather conditions like temperature, rainfall, frost, snow, and wind speeds.

Historical Data, Weather Observations for Sydney, Australia - Observatory Hill: www.bom.gov.au/climate/data/st...

★ ★ Code Available on GitHub ★ ★

GitHub: github.com/TheQuantPy

Specific Tutorial Link: github.com/TheQuantPy/youtube...

★ ★ QuantPy GitHub ★ ★

Collection of resources used on QuantPy UA-cam channel. github.com/thequantpy

★ ★ Discord Community ★ ★

Join a small niche community of like-minded quants on discord. / discord

★ ★ Support our Patreon Community ★ ★

Get access to Jupyter Notebooks that can run in the browser without downloading python.

/ quantpy

★ ★ ThetaData API ★ ★

ThetaData's API provides both realtime and historical options data for end-of-day, and intraday trades and quotes. Use coupon 'QPY1' to receive 20% off on your first month.

www.thetadata.net/

★ ★ Online Quant Tutorials ★ ★

WEBSITE: quantpy.com.au

★ ★ Contact Us ★ ★

EMAIL: pythonforquants@gmail.com

Disclaimer: All ideas, opinions, recommendations and/or forecasts, expressed or implied in this content, are for informational and educational purposes only and should not be construed as financial product advice or an inducement or instruction to invest, trade, and/or speculate in the markets. Any action or refraining from action; investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied in this content, are committed at your own risk an consequence, financial or otherwise. As an affiliate of ThetaData, QuantPy Pty Ltd is compensated for any purchases made through the link provided in this description.

I hope everyone is enjoying the weather derivative series so far, I am looking forward to implementing this monte carlo method in the next tutorial to finally price some temperature options under the risk-neutral probability measure!

Wow. Thank you 🙏

Great video series. Eagerly waiting for next video in pricing the option. When can we expect 🙏🙏

Within the week

Hi, how to sample f(X1,X2,X3 I X1+X2+X3 = z) where f(.) is normal distribution ? f(X1 I X1+X2 = z) we can generate from conditional normal distribution

Hey its soo good that ı just can not thank enough. Wanna have a financial engineering degree can ı send you curriculum for you to check?

Hello, great video, thank you! I have a couple of questions:

1) What if I want to price a weather derivative and there is no market (it would be a sort of parametric insurance)? We should price under P or we should price under Q adding the market price of risk?

2) How do different models of variance impact the simulation study? I read that someone also use Garch model to model the volatility of the temperature (with DAT temperature dynamics given by season + AR process)

Thank you in advance, I really appreciate your work.

Thanks for the questions

1) risk-neutral pricing under Q, stay tuned for next video.

2) in the last video we investigated some different options for volatility models, but yes you can use many models to capture both the physical and risk-neutral pricing dynamics. Depends on your validation metrics, comes down to the art/science of modelling

maths for the advancement of money-hoarding psych05