Thank you! I was under the impression that the volatile forward rate will be some sort of expansion of the forward rates we calculated earlier, but I see that without calibration this is imposible

Thanks alot, this was very helpful Fabian. I think there is a small error in the text in red highlights at 12:00, Although in the formula you've calculated correctly on the spot rate, it looks like you've mentioned par rate in the red highlighted text box (0.0450)

@fabianmoa, around the 19:00 mark you build a 2 year par curve, but use rates from T0 and T1? Why not T2 for the 2nd year ... I'm confused as to why there are not 3 ends to the binomial tree for the 2 year bond?

Why did you calculate the spot/forward rates for all subsequent periods than the first one? If at the end you just ended up using the first par rate (=S1) to initially generate the model. Then for calibration, you just relied on the assumption that we needed to achieve the 100 (par value).

Nope. It will be given. But you may be given the interest rate volatility and an interest rate in one of the nodes and asked to find the interest rate in the upper/lower node.

Fabian, you are the best teacher for Fixed Income I have come across.

Simply A M A Z I N G! Cant describe how much time you save me with this explanation!

Thank you Fibian, I am actually going to pass my test next week thanks to you. I was really lost until I found your videos!

very well done Fabian, absolute stunning work here buddy. cheers !

Hi Fibian, I just want to thank you for the great videos. Really admire how you simplifying such concepts that sound so difficult in classrooms.

Thanks for the lesson. You are an amazing teacher I can say.

I appreciate that!

Such a simple and wonderful explanation!!

Thanks a lot :)

Thank you so much for this video. I am struggling with this topic. Now my problem is slove.

Thanks for all your amazingly made short videos Fabian!

You're welcome, Arnold. Thanks for watching.

helped me on something I have been stuck on for days

Thank you! I was under the impression that the volatile forward rate will be some sort of expansion of the forward rates we calculated earlier, but I see that without calibration this is imposible

Yes, you're right. It is dependent on the volatility assumption and the price of the benchmark bond

Thanks a lot Fabian. It was great.

No problem!

Thanks alot, this was very helpful Fabian. I think there is a small error in the text in red highlights at 12:00, Although in the formula you've calculated correctly on the spot rate, it looks like you've mentioned par rate in the red highlighted text box (0.0450)

wtf this video is sooo good !!! incredible teacher

thanks..great teaching.well explained.

Hi Fabian, thanks a lot. Great explanation!

so well explained!!! thank you so much

Thank you! 😄

@fabianmoa, around the 19:00 mark you build a 2 year par curve, but use rates from T0 and T1? Why not T2 for the 2nd year ... I'm confused as to why there are not 3 ends to the binomial tree for the 2 year bond?

Why did you calculate the spot/forward rates for all subsequent periods than the first one? If at the end you just ended up using the first par rate (=S1) to initially generate the model. Then for calibration, you just relied on the assumption that we needed to achieve the 100 (par value).

Hi Fabian, how would this change for a zero coupon bond?

Great video, thank you

great. easy to follow.

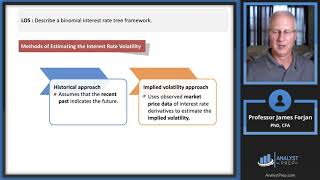

How do you come up with, calculate, or find the interest rate volatility if it's not given?

Hi Fab are u required to construct the tree for the exam? Like how on earth are u supposed to do that without excel?

Nope. It will be given. But you may be given the interest rate volatility and an interest rate in one of the nodes and asked to find the interest rate in the upper/lower node.

@@FabianMoa ok thank u Fab.

THANKS A LOT

You're welcome!

What a legend

Thank you!

The middle rate for period 2 (6,9007%) shouldn't be equal to the forward rate ( F(2,1)=7,1297 ) ?

Hi George, it will not be equal

Could you please do the same using the Ho-Lee Model?

Why is the distance between up node and down node set at 2 standard deviations?

Hi Arun I will answer that in another video 👌

@@FabianMoa sure, thank you.

I wonder how do you do this in exam?

This is for educational purposes. It is unlikely that they will test the generation of the tree in the exam.