UA-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, support my Channel with your subscription and sharing my videos with your cohorts.

hello i need some help. I have the following requirement: Estimate a univariate time series model (white noise, autoregressive, moving average or ARMA) that you think best describes the time series you have chosen and interpret your results. I tried using KO (coca cola) returns but i'm not understanding which is the best prcoess#

Excellent videos. To the point. Very helpful specially from an application perspective. Have watched a lot of your content. You are doing brilliant work. Please keep this going!! Best wishes!! :)

Hi Prateek, I am humbled and encouraged by your positive feedback. I hope to do more to help as many that are willing to learn..may I know from where (location) you are reaching me?

Hi Alexandra, I am humbled by your positive feedback and remarks. I will continue to do my best to simplify the technicalities involved in econometric analysis. I hope that you will subscribe (it's FREE) and encourage your friends and colleagues to do same. Please may I know from where (location) you are reaching me?

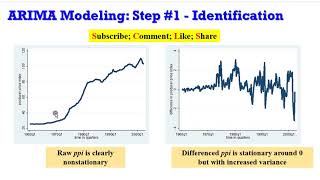

Dear Madam, Thanks for the clear presentation. Anyway, I may have a question. Your estimation was done in two parts; first: ARMA (1, 1), ARMA (1, 1), ARMA (1, 8), ARMA (8, 1) and ARMA (8, 8). We found that ARMA (1, 8) was the best based on the criteria (AI, SBC, …). Then, the second stage was the estimation of AR(1) AR(12) MA(8) and AR(1) MA(8) MA(12). Getting the result, we found also that AR(1) MA(8) MA(12) was selected for forecasting. So, my question is why we should estimate into two steps like that? Isn’t it a wrong path if we estimate all the possible equation at once: ARMA (1, 1), ARMA (1, 1), ARMA (1, 8), ARMA (8, 1), ARMA (8, 8), ARMA (1, 12), ARMA (12, 1), ARMA (12, 8), ARMA (8, 11), and ARMA (12, 12); then, we will choose the best based on these set criteria? Because we know from the correlogram that lag 12 is significant. If we would do that; could we get the same result? I wanna try but I do not find the link of the downloadable data. Thanks for your coming response and also for your good explanation.

Hi Lala, no harm in exploring your procedure. After all, there is no end to learning and there are several ways to get a bird. Also, the link to the dataset is shown in the video and available in the video description. May I know from where (location) you are reaching me?

@@CrunchEconometrix Lala from Madagascar; let me try to find the data and launch my e views. I ll be back in the discussion for the result ... Many thanks again for ur kindness

Thanks for the video...But I would like to ask...if re-estimation is done to include an additional AR or MA term...how would the new ARIMA expression look like?

Are the t-statistics for ARMA coefficients adjusted for the bias of the estimator? there is no really a good way to estimate ARMA coefficients bias free like in a regular regression setting. if not, they are wrong even in large samples as the bias is very persistent and consistency kicks in in the limit.

Thank you for the extremely beneficial videos! I would like to ask, if one finds that there are some lags lying outside the bounds when he tests for autocorrelation, what could be the reason for this and what are the possible ways to solve this? Thanks in advance!

Hi Musah, I explained this and also showed what to do either in this clip or in the Stata version. So, you may need to watch both and adapt the information to your study. Thanks.

Hi! Thanks for your videos, I found them really helpful. May I just ask a technical question, please? If I am using EViews8, do I have to write: ar(1) ar(2) ar(3) .... ar(8) ma(1) ma(2) ...ma(8) and so on when estimating ARIMA(8,1,8), for instance? Or can I only include the necessary lag order without writing them from the first one to the necessary one? Thank you in advance

Hello Mrs. Thanks a lot for your videos. They are really helpful. I'd like to ask a quick question. When you adjust the model arima (1,1,8) with ma(12), how should we then write the new adjusted model ? Arima (1,1,8,12) ? I guess not, I'd like to understand this part. Thank you.

Hi Dimitri, if I were to do this, I will only make a note in my work on the adjusted model....and not necessarily specify another having initially done so. Thanks.

Thanks you for your video, I have learnt a lot... i just have 1 question, i am comparing 2 models, one of them has high adjusted R2, low AIC & SBIC, but the sigmasq is also higher... which model should I choose madam?

Hello sir. Thank you for this helpful video. I have a question. With the ARIMA method, how can we obtain the results of the volatility of that variable for each period of a variable, for example in an annual data set, for each year. For example, 1990 --- 1991 ---- 1992. Thank you.

Thanks Berk for the positive feedback...appreciated! I have no idea about the approach you are suggesting. You may need to check other online resources. Regards.

Dear Professor, On determining the optimal model and including number of lags in the ARIMA (P, d, q) what is the decision when the Sigma2 and Adjusted R2 are not moving at the same direction. Consider the results below; Model 1: Significant Coefficient : 3 Sigma2 (volatility): 879.2982 Adjusted R2: 0.277531 AIC: 9.769049 SBIC: 9.910767 Model 2: Significant Coefficient : 3 Sigma2 (volatility): 855.7793 Adjusted R2: 0.296856 AIC: 9.754889 SBIC: 9.896608 Which one is a better combination, i mean, which one i should use? Thanks

Shaf, please "adapt" explanations. Not in my place to decide for you. I gave clear explanations on the criteria...please use them. You may need to watch the clip again. Thanks.

Hi Tuki, thanks for the positive feedback. Deeply appreciated! But it appears you skipped the prerequisite videos on "model estimation and selection". Kindly watch them for more information. Please may I know from where (location) you are reaching me?

Hi thanks for the vidio but i have question. I see you remodelling from (1,1,8) in prev video and include the 12 because correlogram shows a not-flattened pattern, but why in the estimate in eviews u include ma (8) and ma (12) simultaneously? Can I just write the formula "c ar(1) ma(12)"? or still need to write "c ar(1) ma(8) ma(12)"?

Hi Pradipta, you may decide to follow my approach or do what you feel is right. You may also check other online resources for more information. Regards.

Hi Shriya, as detailed in econometric textbooks, articles and online resources there are several reasons for log transformation - to control for heteroscedasticity, outliers etc. Kindly read up, thanks.

hello Madam. MY name is Abu Bakar. thank you so much for this humanitarian gesture. i really appreciate your effort. my question is: I am working on panel data. but couldn't run ARIMA with this panel data in eviews. can you kindly help. Thank you

thanx for the lecture I have one question that to check serial correlation in ARIMA model we need to check correlogram Q statistics or correlogram residual squared

Dear mam, My AR terms are : 96, 192 and my MA terms are 84, 90, 96, 100 and 192 My best fit ARIMA model is (96,1,96) and I deliberately left the combinations with 192. When I ran the correlelogram of Q statistics for (96,1,96), I got significant values in 1, 4 for both ACF and PACF which is not at all there in my original AR and MA terms (AR terms are : 96, 192 and my MA terms are 84, 90, 96, 100 and 192 ). Now what should I do for Diagnostics mam? I should go for AR(96),MA(96),MA(192) and AR(96),AR(192),MA(96) ???? or I should proceed with the following combinations: AR(96),MA(96),MA(1) AR(96),AR(1),MA(1) AR(96),MA(96) , MA(4) AR(96),AR(4),MA(96) Please do help me mam. .

Hello Madam. First off I would like to say thank you so much for making this video as it helps me for my thesis. A question though; my q statistics checks out fine but I'm having some trouble for my residual squared correlogram. All the probability is valued below 5% and lags 1 through 10 isn't flat. Any solutions for this madam?

Hi, lags 1 to 10 are outside their CIs may imply that you did not use the appropriate ARIMA model from onset. Those lags still contain some information left uncaptured.

Hi very informative madam can you please tell me how can i run or use AR(1)AR(12)MA(8),we use ARIMA (12,1,8)?how can i write two AR terms together .i use the R software .very greatful.

good evening sir, i am camara from malaysia. i actually have two problem to run the arima model: 1) i transformed my annually data to quaterlly but i still have problem to run it. 2) i used also my annually data for arima modeling but if i want to forecast, the eviews tells me to not put new year. To sum up, i followed all your step in order to run it but there is no way, please help me.... Thank you in advance

UA-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, support my Channel with your subscription and sharing my videos with your cohorts.

hello i need some help. I have the following requirement: Estimate a univariate time series model (white noise, autoregressive, moving

average or ARMA) that you think best describes the time series you have

chosen and interpret your results.

I tried using KO (coca cola) returns but i'm not understanding which is the best prcoess#

Excellent videos. To the point. Very helpful specially from an application perspective. Have watched a lot of your content. You are doing brilliant work. Please keep this going!! Best wishes!! :)

Hi Prateek, I am humbled and encouraged by your positive feedback. I hope to do more to help as many that are willing to learn..may I know from where (location) you are reaching me?

Excellent videos. Big thanks from the UK, subscribed, liked and shared your videos to my friends.

U're da best, Sean!😄 I'm humbled by your comment and subscription. May God bless you...and thanks for sharing too🙏

very informative and clear concept video maam. thank you so much for sharing.

You are welcome, Ali! 💞

The vedio is wonderrulf thnks for sharing.

Thanks for your encouraging feedback, deeply appreciated 🥰🙏

Is my pleasure!

Hi thank you so much these are incredible, no other videos like these available. Brilliant!!!

Thanks, Lisa for the positive feedback and remarks on my videos. Deeply appreciated! May I know from where (location) you are reaching me?

Maam, u are the best and i love you fir for saving my life

Hahahaha Esse, glad you find this helpful!

love your videos, please keep sharing!!

Thanks, Camilla for the encouraging feedback. Deeply appreciated!!! May I know from where (location) you are reaching me?

thank you for saving my life, i love you.

Hahahaha Firas, compliments well taken! 💕 😊 May I know from where (location) you are reaching me?

@@CrunchEconometrix I'm from Tunisia(North Africa), I'm a Risk Management Student

@@firasmbarki4793 Awesome Firas! 💕 Kindly spread the word about my videos to your friends and academic community in Tunisia 🇹🇳! 💕 😊

Thank you so much, this videos help me perfectly! Way better explanation than my professor´s

Hi Alexandra, I am humbled by your positive feedback and remarks. I will continue to do my best to simplify the technicalities involved in econometric analysis. I hope that you will subscribe (it's FREE) and encourage your friends and colleagues to do same. Please may I know from where (location) you are reaching me?

Dear Madam,

Thanks for the clear presentation. Anyway, I may have a question.

Your estimation was done in two parts; first: ARMA (1, 1), ARMA (1, 1), ARMA (1, 8), ARMA (8, 1) and ARMA (8, 8). We found that ARMA (1, 8) was the best based on the criteria (AI, SBC, …). Then, the second stage was the estimation of AR(1) AR(12) MA(8) and AR(1) MA(8) MA(12). Getting the result, we found also that AR(1) MA(8) MA(12) was selected for forecasting. So, my question is why we should estimate into two steps like that? Isn’t it a wrong path if we estimate all the possible equation at once: ARMA (1, 1), ARMA (1, 1), ARMA (1, 8), ARMA (8, 1), ARMA (8, 8), ARMA (1, 12), ARMA (12, 1), ARMA (12, 8), ARMA (8, 11), and ARMA (12, 12); then, we will choose the best based on these set criteria? Because we know from the correlogram that lag 12 is significant. If we would do that; could we get the same result? I wanna try but I do not find the link of the downloadable data.

Thanks for your coming response and also for your good explanation.

Hi Lala, no harm in exploring your procedure. After all, there is no end to learning and there are several ways to get a bird. Also, the link to the dataset is shown in the video and available in the video description. May I know from where (location) you are reaching me?

@@CrunchEconometrix Lala from Madagascar; let me try to find the data and launch my e views. I ll be back in the discussion for the result ... Many thanks again for ur kindness

Superbly done. Plz discuss seasonal data or SARIMA model. plz discuss (3,1,1)(3,1,1) SARIMA model with Model equation.

At the moment, I have no idea about SARIMA. But I have noted the topic. Thanks.

Thanks for the video...But I would like to ask...if re-estimation is done to include an additional AR or MA term...how would the new ARIMA expression look like?

I showed what to do. You may want to check out other online resources for more information.

Are the t-statistics for ARMA coefficients adjusted for the bias of the estimator? there is no really a good way to estimate ARMA coefficients bias free like in a regular regression setting. if not, they are wrong even in large samples as the bias is very persistent and consistency kicks in in the limit.

Since you know these, thanks for knowledge sharing. Appreciated 🙏

A very clear explanation to be understood.

Should we do heteroskedasticity test for the chosen model before go to forecast step?

Thank you.

Yes, you can.

Thank you for the extremely beneficial videos! I would like to ask, if one finds that there are some lags lying outside the bounds when he tests for autocorrelation, what could be the reason for this and what are the possible ways to solve this?

Thanks in advance!

Hi Musah, I explained this and also showed what to do either in this clip or in the Stata version. So, you may need to watch both and adapt the information to your study. Thanks.

@@CrunchEconometrix , thank you ma'am

Hi! Thanks for your videos, I found them really helpful. May I just ask a technical question, please? If I am using EViews8, do I have to write: ar(1) ar(2) ar(3) .... ar(8) ma(1) ma(2) ...ma(8) and so on when estimating ARIMA(8,1,8), for instance? Or can I only include the necessary lag order without writing them from the first one to the necessary one? Thank you in advance

Hi Diana, I showed what to in ARIMA (Estimations). Kindly watch and adapt. Thanks.

excellent videos --- I mean excellent

Thanks for the positive feedback, Yannick!!!

Hello Mrs. Thanks a lot for your videos. They are really helpful. I'd like to ask a quick question. When you adjust the model arima (1,1,8) with ma(12), how should we then write the new adjusted model ? Arima (1,1,8,12) ? I guess not, I'd like to understand this part. Thank you.

Hi Dimitri, if I were to do this, I will only make a note in my work on the adjusted model....and not necessarily specify another having initially done so. Thanks.

@@CrunchEconometrix Thank you very much.

How do you Write down the adjusted Model? I have the same question

Hi Seidias, there's no need to write down the adjusted model. Explaining what you did should suffice.

Thanks you for your video, I have learnt a lot...

i just have 1 question, i am comparing 2 models, one of them has high adjusted R2, low AIC & SBIC, but the sigmasq is also higher... which model should I choose madam?

Bishal, use the guides I gave to picking the ideal model and take a decision. Thanks.

@@CrunchEconometrix alright ma'am, thanks for your response

Hello sir. Thank you for this helpful video. I have a question. With the ARIMA method, how can we obtain the results of the volatility of that variable for each period of a variable, for example in an annual data set, for each year. For example, 1990 --- 1991 ---- 1992.

Thank you.

Thanks Berk for the positive feedback...appreciated! I have no idea about the approach you are suggesting. You may need to check other online resources. Regards.

It is good and simple to understand Thanks, Is it possible to forecast the best ARIMA model even the residual is not normal?

Hi Gebeyehu, thanks for the positive feedback. Normality of the residual must be established.

Dear Professor,

On determining the optimal model and including number of lags in the ARIMA (P, d, q) what is the decision when the Sigma2 and Adjusted R2 are not moving at the same direction. Consider the results below;

Model 1:

Significant Coefficient : 3

Sigma2 (volatility): 879.2982

Adjusted R2: 0.277531

AIC: 9.769049

SBIC: 9.910767

Model 2:

Significant Coefficient : 3

Sigma2 (volatility): 855.7793

Adjusted R2: 0.296856

AIC: 9.754889

SBIC: 9.896608

Which one is a better combination, i mean, which one i should use?

Thanks

Shaf, please "adapt" explanations. Not in my place to decide for you. I gave clear explanations on the criteria...please use them. You may need to watch the clip again. Thanks.

The results are not aligned with you said in the video. The Siqma2 and Adjusted R2 are moving in different direction.

@@MShaf-ic9td Use AIC Criteria and follow my explanation.

Thank you so much for the explanation and sorry for asking too many question.

thank you very much this videos. may us you, how can choice the best models all of alternative?

Hi Tuki, thanks for the positive feedback. Deeply appreciated! But it appears you skipped the prerequisite videos on "model estimation and selection". Kindly watch them for more information. Please may I know from where (location) you are reaching me?

Great video...can you please tell me how did you obtain column "dppires" (residuals)... Which command did you use to transform dppi to dppires?

Which part? In this video?

Hi thanks for the vidio but i have question. I see you remodelling from (1,1,8) in prev video and include the 12 because correlogram shows a not-flattened pattern, but why in the estimate in eviews u include ma (8) and ma (12) simultaneously? Can I just write the formula "c ar(1) ma(12)"? or still need to write "c ar(1) ma(8) ma(12)"?

Hi Pradipta, you may decide to follow my approach or do what you feel is right. You may also check other online resources for more information. Regards.

thanks professor

why you didnt choose ARIMA(12 1 12)

I explained why in the video and the preceding one. Kindly watch again. Thanks.

You are welcome, Sir.

if i added the variable but the correlogram of the residuals is not flat then what should i do?

Then redo the test with the instruction I gave in the video.

how do you perform correlogram for this residual

Kindly watch the entire videos on ARIMA to fully understand the process.

Hey so how to decide if you should log transform raw data or not?

Hi Shriya, as detailed in econometric textbooks, articles and online resources there are several reasons for log transformation - to control for heteroscedasticity, outliers etc. Kindly read up, thanks.

hello Madam. MY name is Abu Bakar. thank you so much for this humanitarian gesture. i really appreciate your effort. my question is: I am working on panel data. but couldn't run ARIMA with this panel data in eviews. can you kindly help. Thank you

Hi Abubacarr, I never used ARIMA on panel data. You may need to check other online resources. Thanks.

thanx for the lecture I have one question that to check serial correlation in ARIMA model we need to check correlogram Q statistics or correlogram residual squared

Hi Ramandeep, it's the residuals as explained in the video. May I know from where (location) you are reaching me?

If in ljung box test all the p value is insignificant, but some of the lag spike are outside the band , is it acceptable?

Jeet, this video is detailed and well explained. You may want to watch it again and apply to your results. Thanks.

If my probability of all lags in ljung box test is less than 0.05, what should i do to my data or model?

Hi Chan, there is no direct answer to this. You can combine several measures: increase lags, change the series etc.

Dear mam,

My AR terms are : 96, 192 and my MA terms are 84, 90, 96, 100 and 192

My best fit ARIMA model is (96,1,96) and I deliberately left the combinations with 192. When I ran the correlelogram of Q statistics for (96,1,96), I got significant values in 1, 4 for both ACF and PACF which is not at all there in my original AR and MA terms (AR terms are : 96, 192 and my MA terms are 84, 90, 96, 100 and 192

).

Now what should I do for Diagnostics mam?

I should go for AR(96),MA(96),MA(192)

and AR(96),AR(192),MA(96) ????

or I should proceed with the following combinations:

AR(96),MA(96),MA(1)

AR(96),AR(1),MA(1)

AR(96),MA(96)

, MA(4)

AR(96),AR(4),MA(96)

Please do help me mam.

.

Hi Arrthi, so what are the various outcomes of the different ARIMA models you estimated?

Hello Madam. First off I would like to say thank you so much for making this video as it helps me for my thesis. A question though; my q statistics checks out fine but I'm having some trouble for my residual squared correlogram. All the probability is valued below 5% and lags 1 through 10 isn't flat. Any solutions for this madam?

Hi, lags 1 to 10 are outside their CIs may imply that you did not use the appropriate ARIMA model from onset. Those lags still contain some information left uncaptured.

What if null hypothesis of no autocorrelation in residuals is not rejected???? Plz i need guidance

You re-estimate the model by augmenting the lags.

What should i do mam if autocorrelation values are still less then 5 %

Re-estimate the model at higher-order and/or change the ARIMA structure.

Hi very informative madam can you please tell me how can i run or use AR(1)AR(12)MA(8),we use ARIMA (12,1,8)?how can i write two AR terms together .i use the R software .very greatful.

Hi Neelma, thanks for the positive feedback. Deeply appreciated! But I don't know how to use the R software, unfortunately.

I dont ask how to use in R but my qus is how can we write it ARIMA(.,.,.) i.e u use two ar terms 1 and 12

@@neelma2199 Why not follow my example? It is well explained.

Dear Mrs.

Please add auto-substitute for English video. Thank you so much!

Hi Phurong, I wish I could but that will be too much for me to handle. Please bear with me. May I know from where (location) you are reaching me?

what should we do if there are still probability values more than 5% in auto correlation test ?

Thank you.

Okki, I explained that values above 5% indicate no autocorrelation.

@@CrunchEconometrix Thank you

good evening sir, i am camara from malaysia. i actually have two problem to run the arima model: 1) i transformed my annually data to quaterlly but i still have problem to run it. 2) i used also my annually data for arima modeling but if i want to forecast, the eviews tells me to not put new year. To sum up, i followed all your step in order to run it but there is no way, please help me....

Thank you in advance

Having transformed the data, then quarterly data and not the annual should be used for forecasting.

Sir, what if during check the autocorrelation, there is only one probability not greater than 0.05, other than that are greater than 0.05. Helps me

Hi Shahrin, your query is a bit unclear.

@@CrunchEconometrix how can i snap a pic to show you😭

@@CrunchEconometrix do u have instagram of facebook

I encourage queries posted on UA-cam, thanks.

No need to snap a pix. You can state what the query is and I'll do my best to guide you.

Subtítulos por favor!

Subtitles Please!!! :´)

Ronaldo I did not subtitle my UA-cam videos. My apologies.

why sigmasQ is not showing in my result please help me

Did you follow my procedure?