(Stata13): VAR Estimation and Diagnostics

Вставка

- Опубліковано 8 лют 2025

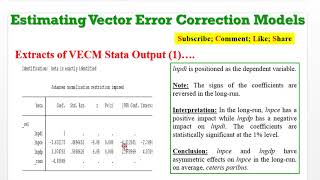

- How can you explain a vector autoregressive (VAR) model? The word “autoregressive” indicates the presence of the lagged values of the dependent variable on the right-hand side of the equation. The word “vector” implies that the system contains a vector of two or more variables. A VAR model is constructed only if the variables are integrated of order one. That is, stationary after first difference. If the variables are cointegrated, construct both short-run (VAR) and long-run (VEC) models. If variables are NOT cointegrated, construct only the short-run (VAR) model. All the variables in a VAR system are endogenous there are no exogenous variables. The stochastic error terms are often called impulses, or innovations or shocks. All variables in the system have equal lags. VAR must be specified in levels, hence VAR in differences is a mis-specification! The VAR model is estimated by ordinary least squares (OLS). Deciding on the maximum lag length, k (an empirical issue). If you use too many lags, you will lose many degrees of freedom, incur statistically insignificant coefficients and multicollinearity. If there are too few lags, there may be specification errors. So, choose optimal lags using the information criterion: AIC, SC, HQIC etc. Also, the interpretation of the short-run coefficients is as in any other linear model they are ceteris-paribus effects and inference can be based on the usual OLS standard errors and test statistics. What are some of the reasons for estimating VAR model? (1) Because there is no cointegration among the variables in the system (2) to establish causal relationships (3) to simulate shocks to the system and trace out the effects of shocks on the endogenous variables (4) for forecasting (decomposing shocks to the VAR system). Kindly check my channel and playlist for all simple and exciting hands-on tutorials using EViews, Stata and Excel applications.

Here is the link to the ex21-1.wf1 dataset (EViews file) used for this tutorial (endeavour to have a Google account for easy accessibility): drive.google.c...

Follow up with soft-notes and updates from CrunchEconometrix:

Website: cruncheconometr...

Blog: cruncheconomet...

Forum: cruncheconometr...

Facebook: / cruncheconometrix

UA-cam Custom URL: / cruncheconometrix

Stata Videos Playlist: • (Stata13):Estimate and...

EViews Videos Playlist: • (EViews10):Interpret V...