after learning calculus I, II,III, differential equations, partial differential equations, probability and stats, would be optimal@@yington a lot of people don't take PDE's, once you learn differential equations you use the notorious text John Hulls intro to quant finance its at undergrad level although used by many grad programs for later chapters. good luck.

@@yingtonkeep in mind what I have told you is only for the very very basics that people cover the first semester of a masters in financial engineering. You really have to sit down and decide what career you want to peruse and then learn what you have to get good at, finance jobs differ dramatically depending upon what you’re doing. Options pricing on sell side vs portfolio optimization on buy side require completely different skills. Be very specific about what you want to do, this is why most people have several years of internships under their belt before even working.

So, instead of assuming a particular distribution which black scholes does, get the implied probability distribution by using closely placed butterflies and binary options?

Thank @@RichardKinch , I understand the Fourier Transform analogy, but not sure if I understand the video. For example, would it be true to say that the cost of a one dollar wide long call spread would be equal to the probability of ITM? Excluding the bid ask spread and transaction costs. In the butterfly case, you would get the change in probabilities, which means that if you sum them up across the entire option chain you would get 1? Is this correct? And thank you NT for the video sir. Edit: I went thru a full example by hand calculating the option chain and what I assumed the video was saying turned out to be indeed the probability of ITM and the density of the PDF of the distribution. This might be well known to everyone - BUT IT BLEW MY MIND.

@@mehdiAbderezai this isnt well known to everyone. this is why a lot of hardcore option traders do wide options targeting a specific price range via the short strikes.

I'm gonna use what delta my broker provides and Black scholes. Too much work to switch systems at my age... If i can was a younger/wealthier man i would research this stuff.

I’ve been self learning to math good enough so that I can understand/follow what he’s teaching. It’s fascinating!

How long does it take to self learn and make sense of any of this…?

after learning calculus I, II,III, differential equations, partial differential equations, probability and stats, would be optimal@@yington a lot of people don't take PDE's, once you learn differential equations you use the notorious text John Hulls intro to quant finance its at undergrad level although used by many grad programs for later chapters. good luck.

@@chymoney1

Thank you !!

@@yingtonkeep in mind what I have told you is only for the very very basics that people cover the first semester of a masters in financial engineering. You really have to sit down and decide what career you want to peruse and then learn what you have to get good at, finance jobs differ dramatically depending upon what you’re doing. Options pricing on sell side vs portfolio optimization on buy side require completely different skills. Be very specific about what you want to do, this is why most people have several years of internships under their belt before even working.

@@chymoney1

Thanks - what would you recommend then for options trading on sell side for instance?

I am doing it, where we use Breeden Litzenberger formula to derive Risk neutral density. Good to understand!

So, instead of assuming a particular distribution which black scholes does, get the implied probability distribution by using closely placed butterflies and binary options?

Yes, rather like a Fourier transform deduces the frequency distribution.

Thank @@RichardKinch , I understand the Fourier Transform analogy, but not sure if I understand the video. For example, would it be true to say that the cost of a one dollar wide long call spread would be equal to the probability of ITM? Excluding the bid ask spread and transaction costs.

In the butterfly case, you would get the change in probabilities, which means that if you sum them up across the entire option chain you would get 1? Is this correct?

And thank you NT for the video sir.

Edit: I went thru a full example by hand calculating the option chain and what I assumed the video was saying turned out to be indeed the probability of ITM and the density of the PDF of the distribution. This might be well known to everyone - BUT IT BLEW MY MIND.

@@mehdiAbderezai this isnt well known to everyone. this is why a lot of hardcore option traders do wide options targeting a specific price range via the short strikes.

@@vtg1632 I didn’t understand the wide option range part.

To catch fast-moving golden fish, even if it costs money, I buy a very wide net and spread it out.

Is my understanding roughly correct?

Thank you!

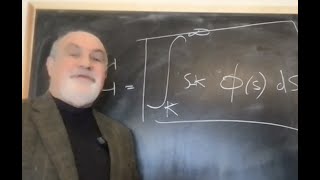

What papers does he referencing to?

Appears that all papers are in the book mentioned in the video

@@tsundokum his "dynamic hedging" book?

@@FirstLast-tx3yj If you are referring to the book that he refers to @8:41, I think it is his book "Statistical Consequences of Fat Tails".

I'm gonna use what delta my broker provides and Black scholes. Too much work to switch systems at my age... If i can was a younger/wealthier man i would research this stuff.

What is all this? I don't understand anything, what's the point of this, someone cares to explain..

ua-cam.com/video/BaU7Sxk6Yk4/v-deo.htmlsi=qTKFQj3QbGWhLnEG

this will be a better start for you