UA-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, support my Channel with your subscription and sharing my videos with your cohorts.

Thank you for the videos. They are really helpful. May I know the interpretation of the IRF when it starts from 0 and not above or below it . Thank you.

Hi there! I was wondering if it was a requirement for the system to have cointegration to estimate IRF model? as i was wondering if i could further analyse my granger causality results, however my variables do not exhibit long term relationship yielded from cointegration tests. Any advice would be much appreciated! Kind regards :)

Hello Prof. Good job. If you want to analyze the impact of financial crisis on economic performance takin g the case of two countries, one following fixed Exchange rate and another floating. Can you use the VAR model? If one country fixed its exchange rate therefore the interest rate is fixed, can you include the Exchange rate and nominal interest rate as lagged variable of this country. VAR? If the series are not normally distribute what to do.? Can you run the var with differebb

Thanks a lot, for the detailed explanation! Your videos are very helpful! Can you help me on my question, please? What if I get the result: "VAR does not satisfy stability condition". How does this affect my analysis and how could this be interpreted? Thanks a lot in advance!

@@CrunchEconometrix If I may ask, what happens if it does not pass all diagnostics? for example, the normality test? then I cannot do the IRF? Thank you in advance!! Your videos are really helpful! :>

Thanks a lot 🙏. I'v been learning so many things that I thought I could struggle to understand at ease. Please, I want to know how to perform variance decomposition in stata. I'v such videos and I'm not getting 🙏

Hi, thanks for very useful and easy to understand videos. You save me from my last time series exam :) I am planning for my dissertation, please help me to understand PanelVAR model. What makes it different with the VAR model? the only difference that i know so far is only that VAR is based on timeseries data, while panel is based on panel data. Thank you

I'm happy to hear this great news, Gabriella. Congratulations! But at the moment I have not used the panel VAR technique. You may check other online resources. Thanks.

Thanks for the encouraging feedback, Aristide. Deeply appreciated🙏. Please know that due to abuse and unethical conduct on attempts to hack my Google drive, Stata dofiles used in my videos are no longer free but available on my website upon payment. Here's the link cruncheconometrix.com/view/datashop.php. Thanks

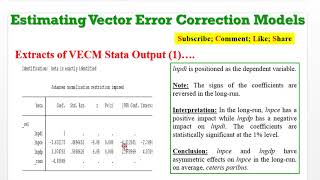

Thank you for this Video and I have one question. In the interpretation, why shock to lnpdi will have asymetric impact on lngdp? What is the meaning of asymetric impact?

Dear Madam, Thank you so much for providing such great content on this topic. I do have a question about the "one SD shock". is it a positive shock or a negative shock are we talking about in the video?

Hello! Your videos are very comprehensive; I was able to understand VAR and IRF! Thank you so much! :> I just have a dumb question: I used many variables so my IRF graphs are too small--I cannot interpret since I cannot view them properly. Is there a way to zoom in the individual graphs? Thank you in advance! :>

Hello, just two questions. First: which is the diference of using the command varbasic and just var? Second: if the coeficients i got with the var model ar not significant for the optimal lag, lets say lag 3 the P value is 0.357 (not significant), can i still interpret the impulse response graphs? Thanks

Hi Erick, try out the 2 codes to observe any difference in coefficients. An insignificant coefficient requires no interpretation, hence it's attendant IRF is meaningless. Estimate the model at different lags and observe the outcomes.

Oh yes Sanduni, I wil. But the videos will be available on my CrunchEconometrix-Teachable platform. Here is the link cruncheconometrix.teachable.com/p/practical-econometrics-for-researchers-beginners-and-advanced-level-users-perba/. You can sign up as a USER to watch the free videos and when you pay the one-off fee of $200.00 you will be ENROLLED to watch all the amazing videos posted on the platform. Come on board and get value for money!

Thank you professor for this useful video. I have vecm results in stata but having hard time deriving IRF from the results? Could you please help. I would also like to know are the IRF from basicvar results different from those after vecm results?

Hi Bosede, Can you please explain why did you use lag(1/2) instead of lag(2)? I use it in stata which yield different output. What is the basic difference between these two? Thank you.

Hi, congratulations by channel. I´d like to ask how Can I convert SD scale to, for instance, dollars, in order do the statament: One US 1,00 increase shock lnpdi increase US 0,35 in lngdp, instead speak as SD?

@@CrunchEconometrix Many thanks for rapid replay. I´m afraid that policy-makers and non-econometrician do not know to understand Standart Deviation. But if I state that US 1.00 dollar increase in lnpdi increases US 0.35 in lngpd at the end of 5 trimester, for instance, they automatically understand that the Multiplier has an impact at 35%. But I don't know how to convert this scale (SD) into currency (dollars).

Hi, you have helped me a lot through your video. thanks a lot. I have a question please, can we convert a variable in log form and left another in raw form? If so what will be the interpretation?

Hi Nayma, you are referring to the functional forms of a model where you have lol-log (elasticity), log-level (semi-elasticity) and level-level. Interpretations differ. For the first, it is "percentage change in X" leads to "percentage change in Y", the second is "a change in X" leads to a "percentage point change in Y" and the third is in "unit change". I will refer you to Wooldridge for detailed interpretation of functional forms. Hope these tips are helpful.

@@CrunchEconometrix I think that they don't show the same outcomes. I'll stick to var tho, because I'll use the command "dfk small" to show F statistics (this is what I saw other studies use). I cannot use this command in "varbasic". I was wondering if you can confirm another doubt that I have: Can I use var if one of the variables is stationary at level and the other variable is only stationary at 1st difference? Thank you very much! PS: I've just subscribed!

@@feliperodriguescruz1794 Good to know this from you...but NO you can't use VAR but ARDL. Thanks for your subscription, please share my videos with your friends and academic community! Gracias 🙏

Hi..I have a question 1.about normality....is that required to VAR model?, because in some discussion many of reseacher assume it is not a problem....thank you for advice

Hi Andres, please forgive my very late response. Yes, I agree too cos I downplay normality this is because there is always the likelihood that some series in the system will not have normally distributed residuals. So, once my VAR model passes other relevant diagnostics, I'm good-to-go...may I know from where (location) you are reaching me?

Thank you for the tutorial. This is very useful. I have one question: how can i get coefficient (negative, central and positive) from impulse response for each variable in each period? Regards.

..but is the shock itself negative or positive? or you mean both positive and negative shocks would give these responses? and moreover, why do you think GPD will respond this way to the shocks. in other words, is there any economic theory underpinning these responses? or are you suppose to come up with why the endo variables have these responses to exogenous shocks?

Emmanuel, whether positive or negative shocks, one mirrors the order. So, for instance if a positive shock to PCEe increases GDP, it implies that a negative shock to PCE will decrease GDP. I simulated my explanation at the end of the video but it is up to the researcher to rationalise the behaviour of the regressand within the context of his/her work. Yes, you must explain to your readership why and how the endo variables respond to exo shocks.

Jones Dahlback It's a matter of choice, Jo. Aside from the fact that it creates an elasticity relationship, it also simplifies interpretation. It is also perfectly okay to use the raw series (ie in level).

Hi Sara, in my opinion shocks are modeled for the short-run, hence the reason for VAR. But you can seek further online resources for shocks related to the VECM.

@@CrunchEconometrix continue the question mam... isn't there a short run and long run equation in vecm, and one more question mam, whether the period in the var analysis can be equated with the data, I mean if the data is 8 periods then 8 quarters, and if monthly data, 8 periods means 8 months

Hi Humaira, due to abuse dofiles are no longer free but available on my website upon payment of a token fee. Here's the link cruncheconometrix.com.ng/shop

Hi Toba, the IRF is closely related to the VAR outcomes. I think I mentioned that. So, if there is a significant VAR relationship, then IRF will be significant too.

hello Ma thank you for your tutorials. they are really powerful. i am running a massive time series research which it needs a proper analysis. i would like to get your consultation. email me please!!

UA-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, support my Channel with your subscription and sharing my videos with your cohorts.

Thank you for the videos. They are really helpful. May I know the interpretation of the IRF when it starts from 0 and not above or below it . Thank you.

I gave interpretations in the video...you can also support interpretations from articles that used the IRF.

Thanks again, your videos so worderful, I much liked it, clear. Keep on be more clear than recent videos 🙏🙏🙏👏👏👏

I'm glad you found it helpful, Ridel☺️

Please Sir, When the ECT(-1) coefficients is for example 49.05 and significant at 1%, how will be the causality direction? Thank you

Ridal, you mean the coefficient of the error correction term is 49.05???

Yes

Yes, it is that. And I don't know how to describe the causality direction.

Thanks for the video. Please do you have one for estimating IRFs from Local Projections on stata?

Angie, no idea what that is.

@@CrunchEconometrix Ok. Thanks.

thank you, great instruction

Glad it was helpful! 🥰

Can you estimate the VAR with differenced series?

Anne, I explained this in the foundational video on VAR. Kindly watch it, thanks.

Hi there! I was wondering if it was a requirement for the system to have cointegration to estimate IRF model? as i was wondering if i could further analyse my granger causality results, however my variables do not exhibit long term relationship yielded from cointegration tests. Any advice would be much appreciated! Kind regards :)

Watch the clips again...well explained on what you need to do.

Hello Prof. Good job. If you want to analyze the impact of financial crisis on economic performance takin g the case of two countries, one following fixed Exchange rate and another floating. Can you use the VAR model? If one country fixed its exchange rate therefore the interest rate is fixed, can you include the Exchange rate and nominal interest rate as lagged variable of this country. VAR? If the series are not normally distribute what to do.? Can you run the var with differebb

Anne, you queries are too confusing to understand.

Thank you so much. It is very helpful and clear

You are welcome, Rupananda!

Very very useful for me, thank you a lots.

tunlin oo Thanks Tunlin and good to hear that my videos are really helpful in some way. Please tell others about my YT Channel...thanks!👍🏽😄

Thanks a lot, for the detailed explanation! Your videos are very helpful! Can you help me on my question, please? What if I get the result: "VAR does not satisfy stability condition". How does this affect my analysis and how could this be interpreted? Thanks a lot in advance!

Eishan, your VAR must pass all diagnostics before you can deploy the IRF and/or FEVD.

@@CrunchEconometrix If I may ask, what happens if it does not pass all diagnostics? for example, the normality test? then I cannot do the IRF? Thank you in advance!! Your videos are really helpful! :>

Diana, heteroscedasticity, autocorrelation, and stability are the most important diagnostics.

Hi, thanks for your tutorial. I wish to know how to compute variance decomposition in Stata. Is there any video discussion on this?

Hi Alice, watch my videos on forecast error variance decomposition. Thanks.

Hello, Thank you for your wonderful Tutorial. can you tell me please how can I take one or two impulse graph from a group of impulse graph?

VAR is a system of equations, hence to my knowledge the IRF graphs are generated together.

Thanks a lot 🙏. I'v been learning so many things that I thought I could struggle to understand at ease. Please, I want to know how to perform variance decomposition in stata. I'v such videos and I'm not getting 🙏

Thanks for the encouraging feedback, Edward. Kindly watch my videos on FEVD...Support that with journal readings. Best regards.

Hi, thanks for very useful and easy to understand videos. You save me from my last time series exam :)

I am planning for my dissertation, please help me to understand PanelVAR model. What makes it different with the VAR model?

the only difference that i know so far is only that VAR is based on timeseries data, while panel is based on panel data.

Thank you

I'm happy to hear this great news, Gabriella. Congratulations! But at the moment I have not used the panel VAR technique. You may check other online resources. Thanks.

Good morning sir, good explications. I want the Dofile please.

Thanks for the encouraging feedback, Aristide. Deeply appreciated🙏. Please know that due to abuse and unethical conduct on attempts to hack my Google drive, Stata dofiles used in my videos are no longer free but available on my website upon payment. Here's the link cruncheconometrix.com/view/datashop.php. Thanks

sr, but IRF result isnt good as u, can u teach me how to improve or repair its better

thanks

The IRF is from your underlying model. To get good IRFs, your model must be good too. So, I suggest you re-work your model.

Thank you for this Video and I have one question. In the interpretation, why shock to lnpdi will have asymetric impact on lngdp? What is the meaning of asymetric impact?

I have responded to you on this via Facebook.

Dear Madam,

Thank you so much for providing such great content on this topic. I do have a question about the "one SD shock". is it a positive shock or a negative shock are we talking about in the video?

Andy, it is plausible to assume "a positive one SD shock" or just a shock as commonly used. I advise that you read articles on IRF for clarity.

Hello! Your videos are very comprehensive; I was able to understand VAR and IRF! Thank you so much! :> I just have a dumb question: I used many variables so my IRF graphs are too small--I cannot interpret since I cannot view them properly. Is there a way to zoom in the individual graphs? Thank you in advance! :>

Hi Diana, try this:

irf graph irf, impulse(y) response( x1 x2)

Modify this to suit your study.

@@CrunchEconometrix It worked! Thank you so much :)) Is there a way though to include the number of lags? Again, thank you in advance!! :>

Diana, not sure how to do that.

You are amazing

Positive feedback is greatly appreciated, thanks!

I would like to know how to formulate GIRF combined graph in STATA application. I tried already but it reports only multiple graphs. Thank you.

Hi Hunny, sorry I have no idea. You may need to check other online resources. Thanks.

@@CrunchEconometrix Thank You Professor.

Hello, just two questions. First: which is the diference of using the command varbasic and just var? Second: if the coeficients i got with the var model ar not significant for the optimal lag, lets say lag 3 the P value is 0.357 (not significant), can i still interpret the impulse response graphs? Thanks

Hi Erick, try out the 2 codes to observe any difference in coefficients. An insignificant coefficient requires no interpretation, hence it's attendant IRF is meaningless. Estimate the model at different lags and observe the outcomes.

Excellent, kindly could prepare a tutorial on panel models?

such pooled, fixed and random effects panel, structural VAR, and Panel VAR

Thanks Rabih, please browse through my list of videos for those on panel data analysis. Kindly tell others too...gracias!

Yeah, thanks Isaw them after commenting, though, could you consider to prepare a tutorial on SVAR and panel VAR?! appreciated

Madam, could you please do tutorial on SVAR analysis in STATA?

Oh yes Sanduni, I wil. But the videos will be available on my CrunchEconometrix-Teachable platform. Here is the link cruncheconometrix.teachable.com/p/practical-econometrics-for-researchers-beginners-and-advanced-level-users-perba/. You can sign up as a USER to watch the free videos and when you pay the one-off fee of $200.00 you will be ENROLLED to watch all the amazing videos posted on the platform. Come on board and get value for money!

@@CrunchEconometrix Thank you mam for your response

Your data is in first differnce, but why you estimate data lngdp not d.lngdp??

Hi Mahjoubi, I explained this in the foundation video on VAR. You may want to watch it.

Thank you professor for this useful video. I have vecm results in stata but having hard time deriving IRF from the results? Could you please help. I would also like to know are the IRF from basicvar results different from those after vecm results?

Hi Nico, you may need to seek further online resources on that because IRF is best obtained from VAR and not VECM. Thanks.

@@CrunchEconometrixThank you very much for your timely response.

Hi Bosede, Can you please explain why did you use lag(1/2) instead of lag(2)? I use it in stata which yield different output. What is the basic difference between these two? Thank you.

Raihan, the 1st estimates the model using lags 1 and 2. The 2nd uses only the 2nd lag. Hence, the difference in the results.

How can I fix this error? Could not open irf.irf file

Hi Osman, not sure how to unravel this. But, I will suggest you post it on Statalist.org for more constructive feedback.

Hi, congratulations by channel. I´d like to ask how Can I convert SD scale to, for instance, dollars, in order do the statament: One US 1,00 increase shock lnpdi increase US 0,35 in lngdp, instead speak as SD?

Edmundo, you can use the standard deviation obtained from the summary statistics, if that will be informative.

@@CrunchEconometrix Many thanks for rapid replay. I´m afraid that policy-makers and non-econometrician do not know to understand Standart Deviation. But if I state that US 1.00 dollar increase in lnpdi increases US 0.35 in lngpd at the end of 5 trimester, for instance, they automatically understand that the Multiplier has an impact at 35%. But I don't know how to convert this scale (SD) into currency (dollars).

Run the summary stats using the raw and not the log form of the variable. That gives you the std dev in real terms not in logs.

Hi, you have helped me a lot through your video. thanks a lot. I have a question please, can we convert a variable in log form and left another in raw form? If so what will be the interpretation?

Hi Nayma, you are referring to the functional forms of a model where you have lol-log (elasticity), log-level (semi-elasticity) and level-level. Interpretations differ. For the first, it is "percentage change in X" leads to "percentage change in Y", the second is "a change in X" leads to a "percentage point change in Y" and the third is in "unit change". I will refer you to Wooldridge for detailed interpretation of functional forms. Hope these tips are helpful.

@@CrunchEconometrix thanks a lot

hello! Can you tell me why you used the command "varbasic" instead of "var"? Do they give us different results?

Try both to see the outcomes...

@@CrunchEconometrix I think that they don't show the same outcomes. I'll stick to var tho, because I'll use the command "dfk small" to show F statistics (this is what I saw other studies use). I cannot use this command in "varbasic".

I was wondering if you can confirm another doubt that I have: Can I use var if one of the variables is stationary at level and the other variable is only stationary at 1st difference?

Thank you very much!

PS: I've just subscribed!

@@feliperodriguescruz1794 Good to know this from you...but NO you can't use VAR but ARDL. Thanks for your subscription, please share my videos with your friends and academic community! Gracias 🙏

Hi..I have a question 1.about normality....is that required to VAR model?, because in some discussion many of reseacher assume it is not a problem....thank you for advice

Hi Andres, please forgive my very late response. Yes, I agree too cos I downplay normality this is because there is always the likelihood that some series in the system will not have normally distributed residuals. So, once my VAR model passes other relevant diagnostics, I'm good-to-go...may I know from where (location) you are reaching me?

Thank you for the tutorial. This is very useful. I have one question: how can i get coefficient (negative, central and positive) from impulse response for each variable in each period? Regards.

The outcome of your IRF is from the underlying VAR model.

..but is the shock itself negative or positive? or you mean both positive and negative shocks would give these responses? and moreover, why do you think GPD will respond this way to the shocks. in other words, is there any economic theory underpinning these responses? or are you suppose to come up with why the endo variables have these responses to exogenous shocks?

Emmanuel, whether positive or negative shocks, one mirrors the order. So, for instance if a positive shock to PCEe increases GDP, it implies that a negative shock to PCE will decrease GDP. I simulated my explanation at the end of the video but it is up to the researcher to rationalise the behaviour of the regressand within the context of his/her work. Yes, you must explain to your readership why and how the endo variables respond to exo shocks.

CrunchEconometrix so in this example the shocks are positive or negative...

@@emmanuelameyaw6806 Positive.

Hi, i have a question please, why using log for these variables

Jones Dahlback It's a matter of choice, Jo. Aside from the fact that it creates an elasticity relationship, it also simplifies interpretation. It is also perfectly okay to use the raw series (ie in level).

Hi! i have a question, how can i simulate a shock when running a VECM model not VAR?

Hi Sara, in my opinion shocks are modeled for the short-run, hence the reason for VAR. But you can seek further online resources for shocks related to the VECM.

@@CrunchEconometrix continue the question mam... isn't there a short run and long run equation in vecm, and one more question mam, whether the period in the var analysis can be equated with the data, I mean if the data is 8 periods then 8 quarters, and if monthly data, 8 periods means 8 months

hello Dr may I have ado file

Hi Humaira, due to abuse dofiles are no longer free but available on my website upon payment of a token fee. Here's the link cruncheconometrix.com.ng/shop

can anyone please tell me how to find the 2nd differential incase the 1st differetial doesn't make the time series stationary

Aleena, use this syntax:

gen d2y = D2.y

@@CrunchEconometrix Thank you so much!

Thank you very much!

U're very welcome, Sebastian...may I know from where (location) you are reaching me?

@@CrunchEconometrix I'm a college student in US

@@sebastiantrent8160 Awesome! 💕 Kindly tell your friends and academic community about my videos and UA-cam Channel. Thanks!

@@CrunchEconometrix Of course.

Sorry prof. Disturbing. How do we know it is significant from the impulse response function.

Regards.

Hi Toba, the IRF is closely related to the VAR outcomes. I think I mentioned that. So, if there is a significant VAR relationship, then IRF will be significant too.

@@CrunchEconometrix thanks prof.

hi, i need VAR model estimate in panel data pleaze: commande: pvar, pvasoc, pvargranger, pvarstable, pvarirf and pvarfevd

Hi Mahjoubi, I have not engaged panel VAR. You may need to check other online resources.

hello Ma thank you for your tutorials. they are really powerful. i am running a massive time series research which it needs a proper analysis. i would like to get your consultation. email me please!!

Edgar Ndani OK, here's it cruncheconometrix@gmail.com but I may not be able to provide you with private tutoring due to my schedule.