Enjoyed this video? Then subscribe to the channel right now, and let's understand and analyze the rest of the income statement: ua-cam.com/video/ToE-oggQiqQ/v-deo.html

my course book together with your channel are being great saviors! Thank you so so much! This question appears in all textbooks: in the past, why was it argued that Apple should spread the recognition of iPhone revenue over a two-year period, rather than recording it upfront? However, for some reason, no teachers seem to explain it! I would like to ask you if you could explain it? I believe is very important, that we students get real life accounting examples (just as you do with Microsoft or other companies throughout your videos) and not with fictitious and simple ones which might help to understand the concept but then make it so hard to expand ones mind to understand real and more complex examples!

Thank you for the kind words! Please let your fellow students know about the channel!!! In answer to your question about Apple under the "old" revenue recognition criteria: Apple's FY2016 annual report, Notes to Consolidated Financial Statements, Note 1 - Summary of Significant Accounting Policies, Revenue Recognition for Arrangements with Multiple Deliverables, states "Revenue allocated to the delivered hardware and the related essential software is recognized at the time of sale provided the other conditions for revenue recognition have been met. Revenue allocated to the embedded unspecified software upgrade rights and the non-software services is deferred and recognized on a straight-line basis over the estimated period the software upgrades and non-software services are expected to be provided." If you look up a document called "Microsoft new accounting standards and FY18 investor metrics", August 3, 2017, by Frank Brod and Chris Suh, they walk you through the "old" versus "new" revenue recognition for Windows 10 OEM revenue, which is a similar story. Hope this helps!

The Finance Storyteller - So can we say that US GAAP also has this new way of Rev Rec called ASC606 and it can work exactly like IFRS and it is not required for both of them to be implemented together?

Hi Shiv! Developing the new revenue recognition standard was a joint project by the FASB and IASB, with synchronized content and timing of adoption. Great move on improving global comparability of financial statements! See also my video on US GAAP vs IFRS ua-cam.com/video/7B96MhOGaqE/v-deo.html

Thank you, Shiv! I am excited too! Look forward to hearing what people think of it. The video is a follow-up to my recent "Income Statement Explained" video: ua-cam.com/video/Hq-44PHgAiU/v-deo.html

If a company sells product & based upon its previous records the company records some percent of sales as "Sales returns and allowances" (for manufacturing defects, warranty expenses & returns). And if we talk about "possible & estimable contingent liabilities" we also book warranty expense for that. So, my question is, what is the difference b/w "sales returns & allowances" & "Contingent liabilities that can be estimated eg. Estimated Warranty expense"? I am confused because in both of these we are making estimates about warranty expenses. So, what is the difference between them? Aren't we booking the same warranty expense twice?

Hello Shiv! The "old" criteria for revenue recognition under US GAAP were: persuasive evidence of an arrangement must exist; delivery must have occurred or services been rendered; the seller's price to the buyer must be fixed or determinable; and collectability should be reasonably assured. The best way to find example of "old way" vs "new way" is to do an internet search on ASC 606 transition or IFRS 15 transition. Listed companies were/are required to disclose the impact of adopting the new standard in their annual report. Part of that is to restate prior years for comparability. To stick with the company in the example, do a search on the term "MSFT New Accounting Standards and FY18 Investor Metrics Conference Call", they take you through how the changeover affected their financials in detail.

The Finance Storyteller - Thanks sir. I will do this for sure but what I was looking for is an example of accounts which will be hit using old method vs new method using same scenario. (Like old one involved Unearned Revenue but new one does not)

Excellent question/suggestion, but I think I missed the "window of opportunity" for making a video on that. That might have been a popular topic around the time ASC 606 / IFRS 15 was first implemented, but by now (2020) everyone should be solidly on the new rules, so I am not going back....

can you do journal entries, FS, cashflows for Air line industry? like collection from agents, cancelled flights, refunds, suppliers, etc? i am currently working for airlines and tasked with getting Finance straight for company. firm follows International accounting standard

Can you develop a case study by merging Micro-soft & Apple (MicroApple) in an unrealistic world? See who gets benefitted and is it possible both can succeed or one has to die for another? Please analyse how bottom line influences stakeholders?

Thanks for the feedback, Rachinder! For the existing videos, you can adjust the speed in Settings - Playback Speed, and/or switch on the subtitles for easier understanding.

The accounting entries are basically still the same: debit accounts receivable credit revenue for the invoice, and debit cost of goods sold credit inventory for shipment of the goods. Applying new revenue recognition rules changes the timing of when those entries are made, not necessarily the nature of them. If you want to learn more about the adjusting entries for accrued revenue and deferred revenue, then watch my video on adjusting entries: ua-cam.com/video/57CST6_RtWk/v-deo.html

@@TheFinanceStoryteller - How do companies make profit during thanks giving when they sell for low cost ? I agree they sell more so more revenue but expense will be more too so how profit ?

@@KumR I think many of the companies are offloading older inventory ("not the latest model") during the sale, and might themselves be putting pressure on the next company in the supply chain (better discounts, better terms), plus cross-/upselling to products and services that are not heavily discounted. I am coming up with these as I go along, you should really check with people that are experts in the field of retail.

Enjoyed this video? Then subscribe to the channel right now, and let's understand and analyze the rest of the income statement: ua-cam.com/video/ToE-oggQiqQ/v-deo.html

my course book together with your channel are being great saviors! Thank you so so much!

This question appears in all textbooks: in the past, why was it argued that Apple should spread the

recognition of iPhone revenue over a two-year period, rather than recording it upfront? However, for some reason, no teachers seem to explain it! I would like to ask you if you could explain it?

I believe is very important, that we students get real life accounting examples (just as you do with Microsoft or other companies throughout your videos) and not with fictitious and simple ones which might help to understand the concept but then make it so hard to expand ones mind to understand real and more complex examples!

Thank you for the kind words! Please let your fellow students know about the channel!!! In answer to your question about Apple under the "old" revenue recognition criteria: Apple's FY2016 annual report, Notes to Consolidated Financial Statements, Note 1 - Summary of Significant Accounting Policies, Revenue Recognition for Arrangements with Multiple Deliverables, states

"Revenue allocated to the delivered hardware and the related essential software is recognized at the time of sale provided the other conditions for revenue recognition have been met. Revenue allocated to the embedded unspecified software upgrade rights and the non-software services is deferred and recognized on a straight-line basis over the estimated period the software upgrades and non-software services are expected to be provided."

If you look up a document called "Microsoft new accounting standards and FY18 investor metrics", August 3, 2017, by Frank Brod and Chris Suh, they walk you through the "old" versus "new" revenue recognition for Windows 10 OEM revenue, which is a similar story.

Hope this helps!

Awesome. The wait ended.

Thank you!!! Enjoy!

The Finance Storyteller - So can we say that US GAAP also has this new way of Rev Rec called ASC606 and it can work exactly like IFRS and it is not required for both of them to be implemented together?

Hi Shiv! Developing the new revenue recognition standard was a joint project by the FASB and IASB, with synchronized content and timing of adoption. Great move on improving global comparability of financial statements! See also my video on US GAAP vs IFRS ua-cam.com/video/7B96MhOGaqE/v-deo.html

I cant wait to see/hear it

Thank you, Shiv! I am excited too! Look forward to hearing what people think of it. The video is a follow-up to my recent "Income Statement Explained" video: ua-cam.com/video/Hq-44PHgAiU/v-deo.html

Excellent video! I love it!!

Thank you very much! Very nice to hear that. :-)

Simply great

Thank you!!!

The video sound is pretty good, beyond my imagination

And what about the content? ;-)

Character In the video It's great, I like it a lot $$

Thank you!

If a company sells product & based upon its previous records the company records some percent of sales as "Sales returns and allowances" (for manufacturing defects, warranty expenses & returns).

And if we talk about "possible & estimable contingent liabilities" we also book warranty expense for that.

So, my question is, what is the difference b/w "sales returns & allowances" & "Contingent liabilities that can be estimated eg. Estimated Warranty expense"?

I am confused because in both of these we are making estimates about warranty expenses. So, what is the difference between them? Aren't we booking the same warranty expense twice?

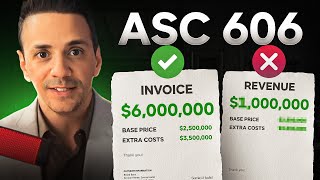

Can I ask for a favor? Can u share a same example which uses old way of rev rec and new way of rev rec?

Hello Shiv! The "old" criteria for revenue recognition under US GAAP were: persuasive evidence of an arrangement must exist; delivery must have occurred or services been rendered; the seller's price to the buyer must be fixed or determinable; and collectability should be reasonably assured. The best way to find example of "old way" vs "new way" is to do an internet search on ASC 606 transition or IFRS 15 transition. Listed companies were/are required to disclose the impact of adopting the new standard in their annual report. Part of that is to restate prior years for comparability. To stick with the company in the example, do a search on the term "MSFT New Accounting Standards and FY18 Investor Metrics Conference Call", they take you through how the changeover affected their financials in detail.

The Finance Storyteller - Thanks sir. I will do this for sure but what I was looking for is an example of accounts which will be hit using old method vs new method using same scenario. (Like old one involved Unearned Revenue but new one does not)

Excellent question/suggestion, but I think I missed the "window of opportunity" for making a video on that. That might have been a popular topic around the time ASC 606 / IFRS 15 was first implemented, but by now (2020) everyone should be solidly on the new rules, so I am not going back....

can you do journal entries, FS, cashflows for Air line industry? like collection from agents, cancelled flights, refunds, suppliers, etc? i am currently working for airlines and tasked with getting Finance straight for company. firm follows International accounting standard

Hi! I have never worked in that industry, so cannot help in that area. I'm sorry!

@@TheFinanceStoryteller ok no problem

Did you find the answers?

Are implementation fees recognized over the life of the contract ?

Hi Aaron! I don't know the answer to that off the top of my head, but browsing through the full text of the accounting standard should get you there.

Can you develop a case study by merging Micro-soft & Apple (MicroApple) in an unrealistic world? See who gets benefitted and is it possible both can succeed or one has to die for another? Please analyse how bottom line influences stakeholders?

Hello Jagadeesh! Nice idea, but I don't do science fiction. ;-) Such a merger would/should never pass antitrust review.

@@TheFinanceStoryteller I am aware of Antitrust. Please don't kill my imagination.

Not trying to kill your imagination, just saying that mine is limited. ;-)

Very nice video, if you dont mind if in next may i ask you to speak a little bit slower! thanks

Thanks for the feedback, Rachinder! For the existing videos, you can adjust the speed in Settings - Playback Speed, and/or switch on the subtitles for easier understanding.

Can u pl give me accounting entries using new rev rec?

The accounting entries are basically still the same: debit accounts receivable credit revenue for the invoice, and debit cost of goods sold credit inventory for shipment of the goods. Applying new revenue recognition rules changes the timing of when those entries are made, not necessarily the nature of them. If you want to learn more about the adjusting entries for accrued revenue and deferred revenue, then watch my video on adjusting entries: ua-cam.com/video/57CST6_RtWk/v-deo.html

@@TheFinanceStoryteller - How do companies make profit during thanks giving when they sell

for low cost ? I agree they sell more so more revenue but expense will be more too so how profit ?

@@KumR Define company..... The retailer (Walmart, Amazon)? The brand (Apple, Nike)? The outsourced manufacturer (Flextronics, Foxconn)?

@@TheFinanceStoryteller - Yep any comp which gives great deals

@@KumR I think many of the companies are offloading older inventory ("not the latest model") during the sale, and might themselves be putting pressure on the next company in the supply chain (better discounts, better terms), plus cross-/upselling to products and services that are not heavily discounted. I am coming up with these as I go along, you should really check with people that are experts in the field of retail.

Character In the video It's great, I like it a lot $$

Thank you very much!