Amazing video. I am studying a MSc In Finance and Invesment in England, these videos are being live saving for me. The way James explains is very intuitive, helping to grasp the concept and deepen the understanding of complex concepts. Many thanks.

In the final example, MRR is 0.85% and fixed rate is 2.5% and the periodic settlement value formula is MRR-Sn... so shouldnt it be (0.85%-2.5%)? Why is it the other way around?

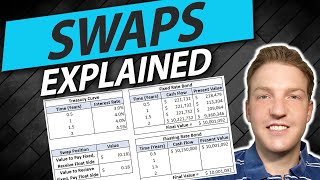

Because the 2.5% fixed swap rate is set so that the present value of fixed and floating payments is equal (over the next four years). If interest rates expectations are unchanged, the present value of the payments to be paid goes above the present value of the fixed payments to be received.

Although I am a year late, I will give it a go. The implied rate is the rate that we calculate using spot rates. If the implies rate is equal to the actual forward rate at time 1,2,3,4 etc then it means the fixed payment receiver must receive less than what he pays since he is in a surplus already. We can illustrate using an analogy. Let's say we have 2 buckets both with100 litres of water and I will lend you water from my bucket and vice versa. During my first expedition I took 30 litres from your bucket while you took 10. Now we know that in the next 3 turns you can take 90 from me while I can only 70 from you . Thus in the next 3 turns I am at a loss cumulative of the next 3 turns

The fixed receiver experiences loss when interest rate expectations are unchanged because the present value of the floating payments becomes greater than the present value of the fixed payments as time progresses. Because the forward curve is upward sloping, these future floating payments are expected to be higher than the earlier payments. As a result, the present value of these future floating payments increases relative to the fixed payments.

Amazing video. I am studying a MSc In Finance and Invesment in England, these videos are being live saving for me. The way James explains is very intuitive, helping to grasp the concept and deepen the understanding of complex concepts. Many thanks.

One of the best videos on this topic. Thank you.

thank you so much for your video!

Great

In the final example, MRR is 0.85% and fixed rate is 2.5% and the periodic settlement value formula is MRR-Sn... so shouldnt it be (0.85%-2.5%)? Why is it the other way around?

Hey are you from zeel education 😂

Mantap

at the 25th minute, in the periodic settlement value, the formula and and the value differs. is it the right calculation?

Can somebody explain why is the fixed receiver getting a loss when the interest rate expectations are unchanged

Because the 2.5% fixed swap rate is set so that the present value of fixed and floating payments is equal (over the next four years). If interest rates expectations are unchanged, the present value of the payments to be paid goes above the present value of the fixed payments to be received.

@@moooooooooooooveyou didnt explain anything??

Although I am a year late, I will give it a go.

The implied rate is the rate that we calculate using spot rates. If the implies rate is equal to the actual forward rate at time 1,2,3,4 etc then it means the fixed payment receiver must receive less than what he pays since he is in a surplus already. We can illustrate using an analogy.

Let's say we have 2 buckets both with100 litres of water and I will lend you water from my bucket and vice versa. During my first expedition I took 30 litres from your bucket while you took 10. Now we know that in the next 3 turns you can take 90 from me while I can only 70 from you . Thus in the next 3 turns I am at a loss cumulative of the next 3 turns

The fixed receiver experiences loss when interest rate expectations are unchanged because the present value of the floating payments becomes greater than the present value of the fixed payments as time progresses. Because the forward curve is upward sloping, these future floating payments are expected to be higher than the earlier payments. As a result, the present value of these future floating payments increases relative to the fixed payments.