I want to appreciate all my subscribers from across the globe (Africa, Asia, Europe, the Middle East, The Americas, and The Pacific). Thank you all for your support. I am encouraged by your comments, questions, likes and critiques. They keep me focussed and poised to do better. I will continue to contribute my little quota such that every student and researcher will independently analyse his/her data. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Please do not keep me to yourself (lol) inform your friends, students and academic networks about my Channel. Tell them CrunchEconometrix breaks down the econometric jargons and teaches with simplicity. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

@@danialfahim1733 Awesome!❤️I'll appreciate it if you can share the link to my UA-cam Channel with your friends and academic community in Malaysia 🇲🇾. They will find the content helpful. Thanks 😊

Thanks for your video however i have a question and i didn't get the solution. How can i get the series of volatility of exchange rate by using EGARCH model please reply on my question

Thank you, my sister. I viewed your videos from the superior institute for labor and business sciences in Lisbon, Portugal, and western Europe, where I am pursuing my Ph.D. in Economics.

Thanks Dr. for sharing your knowledge. Quick question though. I am working with the natural log data of the NSE 20 Share Index. I have been able to estimate the GARCH(1,1) GARCH-M(1,1) and TGARCH(1,1) using the data. However, the EGARCH estimation is returning an error message "log of non-positive value". What could be the problem and how can I resolve it? TIA.

Thank you mam for sharing knowledge. I learned the application of Garch family model from your videos only. I have a question from your EGARCH video i.e how you calculated the value 64. 28%. the exponential value of -0.044197 (e^-0.044197=.9567) is 95.67%. my other question is can I calculate the % impact of negative and positive news on volatility. please tell me how I can do it. Thanks & Regards

Oh yes Arafa, I will. But the videos will be available on my CrunchEconometrix-Teachable platform. Here is the link cruncheconometrix.teachable.com/p/practical-econometrics-for-researchers-beginners-and-advanced-level-users-perba/. You can sign up as a USER to watch the free videos and when you pay the one-off fee of $200.00 you will be ENROLLED to watch all the amazing videos posted on the platform. Come on board and get value for money!

Good morning Dr. Do you have a research study or paper that describes the process of egarch in your study? For reference and citation. Appreciate your input. Thanks

I want to aska question about forecasting price... Let we make a xGARCH estimation. How can we use this estimation to forecast t+1 time price and t+1 time confidence interval for the forecasted price? I will be very grateful to you if you answer this question. Or you can make a video for this subject....

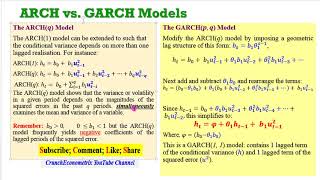

Dear Prof. Many thanks for the explanation. Sorry to take you back. When testing for Heteroskedasticity (ARCH Effect), does the p-values have to be significant at 5% level?. Mine is 0.0987

@ibeh chijioke You need to show understanding of ARCH modelling to estimate a GARCH model. If pvalue is significant is it < 0.05? My advice: watch all my ARCH videos as the precursor to GARCH.

Greeting from India. Madam, while calculating EGARCH, the coefficient of lag return is found to be negative but it is statistically significant. Should I say that my estimation is good?

Hi Qamar, unfortunately I cannot answer to that. You have to form your judgement and interpret your outcomes within the context of your study. Kind regards.

Hello ma'm thank you for your help and videos, my EGARCH alfphas and Betas probabilities are significiant at 5% but my constant's probabiltiy is 0.13. This model is valid or not in this condition ?

@@CrunchEconometrix Thank you for your answer ma'm. I tried to ask you that EGARCH''s constant (C3) significance. For example in your output table in video, if C3's prob. would be 0.13 (13%) , could we accept the model's as significant and use it ?

@@abdulhadialhatem Wow!!! So, nice to hear from my fellow Academics in Iraq 🇮🇶. Please share my videos with your students and the academic community. They will find the content helpful too 😊.

I want to appreciate all my subscribers from across the globe (Africa, Asia, Europe, the Middle East, The Americas, and The Pacific). Thank you all for your support. I am encouraged by your comments, questions, likes and critiques. They keep me focussed and poised to do better. I will continue to contribute my little quota such that every student and researcher will independently analyse his/her data. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Please do not keep me to yourself (lol) inform your friends, students and academic networks about my Channel. Tell them CrunchEconometrix breaks down the econometric jargons and teaches with simplicity. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

THANK YOU SO MUCH!

@@danialfahim1733 U're welcome, Danial😊. Please may I know from where (location) you are reaching me?

@@CrunchEconometrix im from asia! Malaysia. An actuarial science student :)))))

@@danialfahim1733 Awesome!❤️I'll appreciate it if you can share the link to my UA-cam Channel with your friends and academic community in Malaysia 🇲🇾. They will find the content helpful. Thanks 😊

Thanks for your video however i have a question and i didn't get the solution. How can i get the series of volatility of exchange rate by using EGARCH model please reply on my question

Thank you so much for all of these videos! They have completely transformed my econometric understanding and have given me confidence for my exams :)

I could give a million likes for your encouraging feedback, Annabel. May God bless you and give you all "A"s in your papers in Jesus' name, amen!

Thank you, my sister. I viewed your videos from the superior institute for labor and business sciences in Lisbon, Portugal, and western Europe, where I am pursuing my Ph.D. in Economics.

Nice to hear this, Cassidy! ❤️🙏

Thank you so much, Dr. Your videos are helping me to write my dissertation well.

You are so welcome, Japheth 🥰🙏

I am from TURKEY and thank you very much for your informative videos....

You are welcome, Imdat!

thank you very much for this impacting lesson

U're welcome.

thank you so much, you help me a lot! love from Malaysia :)

Happy to hear that, Siti...thanks!

Thanks Dr. for sharing your knowledge. Quick question though. I am working with the natural log data of the NSE 20 Share Index. I have been able to estimate the GARCH(1,1) GARCH-M(1,1) and TGARCH(1,1) using the data. However, the EGARCH estimation is returning an error message "log of non-positive value". What could be the problem and how can I resolve it? TIA.

Hi Robert, it's possible that the EGARCH algorithm is unable to accommodate negative values. You may either drop the technique or change variables.

I changed the mean equation specification to return ar(1) ma(1). Would the equation affect the results or would it result in EGARCH(1,1) estimates?

@@robertndaiga5050 Estimate the model to compare the outcomes.

Support from China! thank you very much!

U're welcome, Leo 😊!

Thank you mam for sharing knowledge. I learned the application of Garch family model from your videos only. I have a question from your EGARCH video i.e how you calculated the value 64. 28%. the exponential value of -0.044197 (e^-0.044197=.9567) is 95.67%. my other question is can I calculate the % impact of negative and positive news on volatility. please tell me how I can do it. Thanks & Regards

Neeru, my video explains how. You may want to watch it again.

Many thanks for the explanation. The results of Lambda C (5) in my paper showed significant but positive. Does this mean there is a leverage effect?

Yes, a leverage effect is implied.

Thank you for the explanation ma'am. But how about Multivariate Garch? Hopefully, you can also make about Multivariate Garch as well. Thank you

Oh yes Arafa, I will. But the videos will be available on my CrunchEconometrix-Teachable platform. Here is the link cruncheconometrix.teachable.com/p/practical-econometrics-for-researchers-beginners-and-advanced-level-users-perba/. You can sign up as a USER to watch the free videos and when you pay the one-off fee of $200.00 you will be ENROLLED to watch all the amazing videos posted on the platform. Come on board and get value for money!

Great videos...Thank you!

Glad you like them, Syed!

Good morning Dr. Do you have a research study or paper that describes the process of egarch in your study? For reference and citation. Appreciate your input. Thanks

Khairul, there are references listed at the end of my ARCH and GARCH videos. Google search/Google Scholar will also give you tons of empirical papers.

Dear Professor. Could you do a multivariate GARCH with a forecast of one of the volatility of the variables?

Thanks for the suggestion, Edilson. I have noted that.

Dear professor please make video on multivariate garch

I want to aska question about forecasting price... Let we make a xGARCH estimation. How can we use this estimation to forecast t+1 time price and t+1 time confidence interval for the forecasted price? I will be very grateful to you if you answer this question. Or you can make a video for this subject....

Hi Imdat, I honestly don't have the answer to this, you may want to check other online resources. Thanks.

Dear Prof. Many thanks for the explanation. Sorry to take you back. When testing for Heteroskedasticity (ARCH Effect), does the p-values have to be significant at 5% level?. Mine is 0.0987

Hi Shelter, you may decide to reject the null hypo at 10%. Just that rejecting the null hypo at 5% gives more confidence about the results.

It helped a lot!! thanks

Thanks for the positive feedback, Laks!

respected professor, did we get the series of leverage effects - kindly respond

Hi Dr. Ghauri, I don't quite understand your query.

Are we to use the return series or the undifferenced in checking for arch effects??

The returns.

I modelled the ar(1) and I checked for arch effects of the residuals..my p value was signifant(higher p value >.1)

If pvalue is significant, I explained what to do.

@@CrunchEconometrix I should go on with OLS..but I am trying to model the data(inflation rate) with selected garch models

@ibeh chijioke You need to show understanding of ARCH modelling to estimate a GARCH model. If pvalue is significant is it < 0.05? My advice: watch all my ARCH videos as the precursor to GARCH.

@@CrunchEconometrix thanks Ma..

Can we run multivariate egarch model in eviews 10

Hi Arup, not sure. But you can check out other online resources for more information.

Greeting from India.

Madam, while calculating EGARCH, the coefficient of lag return is found to be negative but it is statistically significant. Should I say that my estimation is good?

Hi Qamar, unfortunately I cannot answer to that. You have to form your judgement and interpret your outcomes within the context of your study. Kind regards.

Hello ma'm thank you for your help and videos, my EGARCH alfphas and Betas probabilities are significiant at 5% but my constant's probabiltiy is 0.13. This model is valid or not in this condition ?

Kaan, I don't quite understand your query. But I will suggest you watch the clip again to be able to evaluate your model. Thanks.

@@CrunchEconometrix Thank you for your answer ma'm. I tried to ask you that EGARCH''s constant (C3) significance. For example in your output table in video, if C3's prob. would be 0.13 (13%) , could we accept the model's as significant and use it ?

I love you, thanks!

Thanks Guido! I take it as an encouraging feedback. Deeply appreciated! Please may I know from where (location) you are reaching me?

Is it necessary fo variable C to be significant while formulating EGARCH model ? my EGARCH model shows p value higher than 0.05? What shud i do ?

Hi Kailash, if pvalue > 0.05 it implies the coeff is not statistically significant.

Many thanks for the explanation. The results of Lambda C (5) in my paper showed significant but positive. Does this mean there is a leverage effect?

Yes Abdul, that will be the interpretation. Please may I know from where (location) you are reaching me?

CrunchEconometrix I’m one of your fans from Iraq

CrunchEconometrix so, in this case, the good news generate more volition than the bad news in the stock markets.

@@abdulhadialhatem Wow!!! So, nice to hear from my fellow Academics in Iraq 🇮🇶. Please share my videos with your students and the academic community. They will find the content helpful too 😊.

CrunchEconometrix sure. I will do.